FX & Stock market snapshots as of [13/08/2019 0520 GMT]

- In today’s Asian opening session, the China central bank, PBOC has fixed the onshore yuan lower for the 9th straight day at 7.0326 per USD, 115 pips weaker that the previous fix of 7.0211 on Mon. Also, today’s fixing is the weakest since 25 Mar 2008.

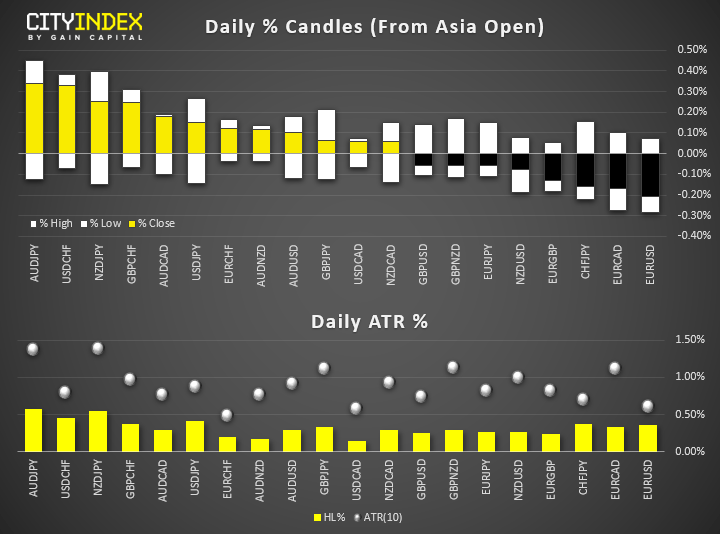

- The offshore USD/CNH has continued to hold steady above yesterday low of 7.0882. The rest of the major pairs and crosses have traded blow their respective 10-day average true ranges so far, a low volatility environment without any key economic data releases in the Asian session.

- The EUR/USD is the weakest pair as it traded down by -0.20% from its 5-day range high of 1.1250 since 06 Aug 2019.

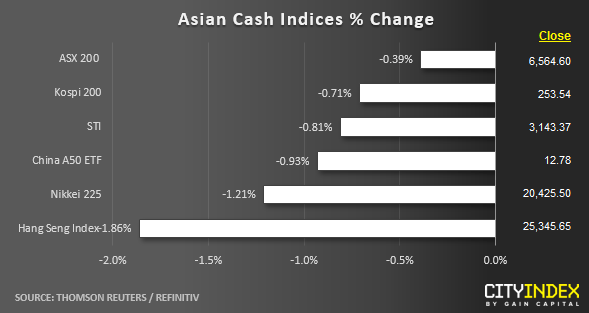

- Ahead of the European opening session, all Asian stock markets have tumbled, taking the cue from a weak performance seen in the key U.S. benchmark indices where the S&P 500 and Nasdaq 100 declined by -1.49% and -1.11% respectively on Mon.

- Negative feedback loop in sentiment is the main catalyst. The on-going Hong Kong protests that have escalated into a higher scale yesterday after a disruption to Hong Kong’s airport operations with a plan to stage another massive protest in the streets this coming Sunday. In addition, contagion from emerging markets is on the rise that saw Argentina’s stocks and currency collapsed to record lows on Mon after disappointing primary election result for the incumbent Argentine President.

- China officials have described the latest unrest in Hong Kong as a sign of terrorism emerging”. Also, media reports have highlighted the sighting of large-scale China’s armed police force personnel and vehicles that have assembled in Shenzhen, city bordering Hong Kong. The risk of military styled intervention from China has increased at this juncture.

- Singapore’s trade ministry has slashed this year GDP growth forecast to 0%-1.0% from previous projections of 1.5%-2.5% due to a challenging external environment.

- The S&P 500 E-mini futures are almost unchanged in today’s Asian session with a tight trading range between 2889 and 2880.

Up Next

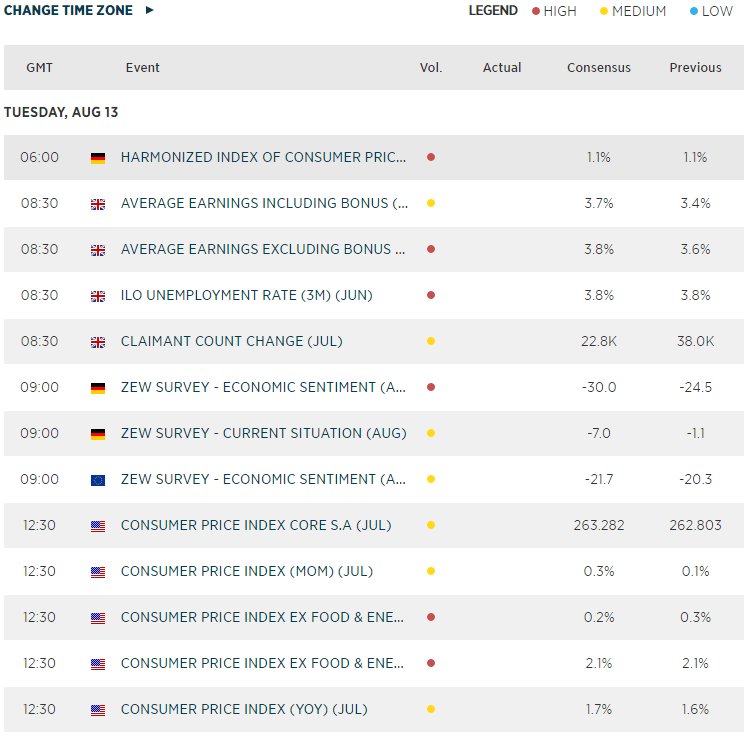

- Germany CPI for Jul at 0600 GMT where consensus is set at 1.1% y/y, unchanged from Jun

- Germany ZEW economic sentiment survey for Jul at 0900 GMT where consensus is at -30.00 down from -24.5 in Jun.

- U.K. Unemployment Rate for Jul at 0830 GMT where consensus is expected 3.8%, unchanged from Jun.

Macroeconomic Calendar

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Forex articles

Today 04:00 PM

Yesterday 11:30 AM