Market Brief: Risk Assets Rally as Cooler Heads Prevail

View our guide on how to interpret the FX Dashboard.

- Following peak “WW3” fears in overnight trade, cooler heads prevailed as news spread that there were no US causalities from the Iranian missile strikes and no immediate plans for further strikes. In a speech this morning, President Trump emphasized economic sanctions, rather than further military actions, in response to the attacks.

- That said, late headlines of explosions in Baghdad’s “Green Zone” may keep traders on edge again heading into Asian session trade.

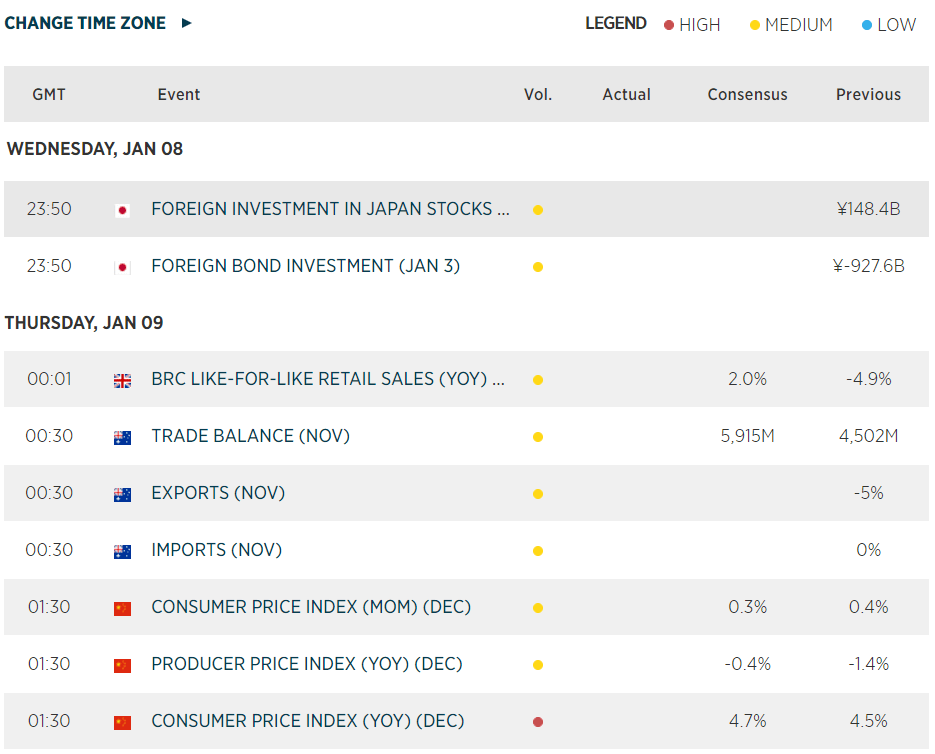

- US data: The ADP Employment report (Dec) came in at 202k vs. 160k expected. Combined with upward revisions to previous reports, traders are more optimistic heading into Friday’s NFP report.

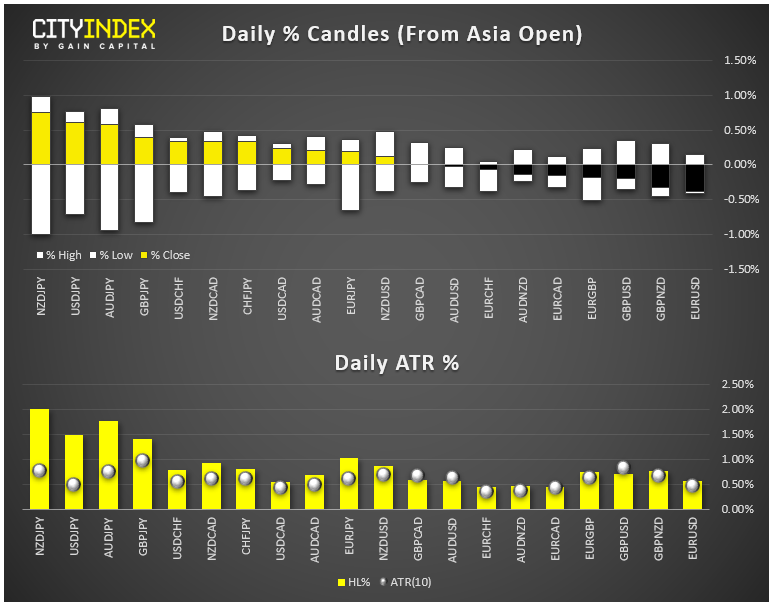

- FX: The New Zealand dollar was the strongest major currency on the day, while the safe haven Japanese yen was the weakest as geopolitical fears receded.

- Commodities: In a truly massive move, oil prices (WTI, -4%) traded as high as 65.60 before reversing to trade down to a low near $59 intraday, driven by receding fears of military action in the Middle East and a surprising buildup in inventories. The prices of gold (-1%) and bitcoin (-2%) followed similar, if less dramatic, intraday paths.

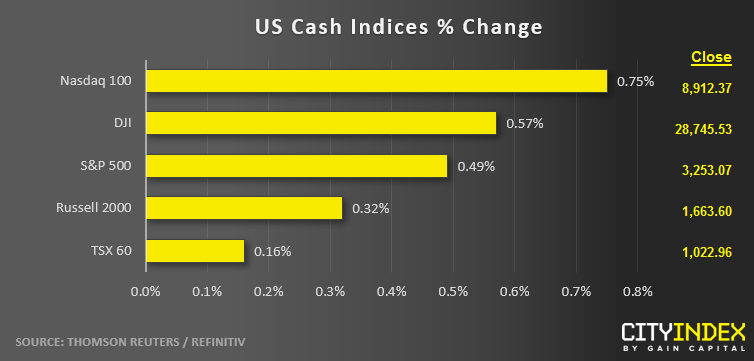

- US indices closed higher as prices recovered from their overnight swoon. European indices also closed in the green, led by a 0.7% gain in Germany’s DAX.

- Technology (XLK) was the strongest major sector on the day. Energy (XLE) was the weakest, and the only sector to fall, dragged down by falling oil prices.

- Stocks on the move:

- Boeing (BA) ticked -2% lower after one of its planes experienced a crash near Tehran, killing all 167 passengers and 9 crew members on board.

- Pharmacy Walgreen’s Boost Alliance (WBA) slid -6% after missing analyst earnings and revenue estimates.

- Retailer Macy’s (M) tacked on 2% after reporting solid holiday sales.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM