View our guide on how to interpret the FX Dashboard

FX Brief:·

- CPI data for Australia came mostly in as expected. This makes it less likely the RBA will cut in November, although expectations were only around 20% anyway. Trimmed mean (RBA’s preferred gauge) remain steady at 1.6% YoY and 0.4% QoQ, although weighed mean CPI was revised lower to 1.2% YoY (1.3% prior) and 0.3% QoQ (0.4% prior). Still – it’s possible RBA could make it to the new year without further easing, unless employment completely turns in the meantime.

- Retail sales in Japan soared by 9.1% YoY in September – although this new-found appetite for ‘stuff’ was in fact the rush to beat October’s sales tax hike. If history is to be repeated, expect retail sales to tank in the coming months.

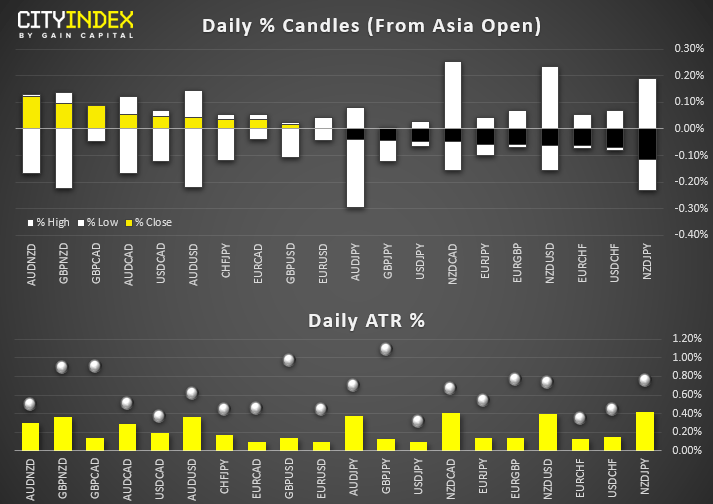

- We’ve seen a few whipsaws across AUD and NZD pairs but, with volatility remaining low overall, not too much can be deciphered from it. Other than it was a news release (AU CPI) and we’re trading back near open prices. And, of course, traders are waiting for today’s highly anticipated FOMC meeting and Powell’s press conference.

Equity Brief:

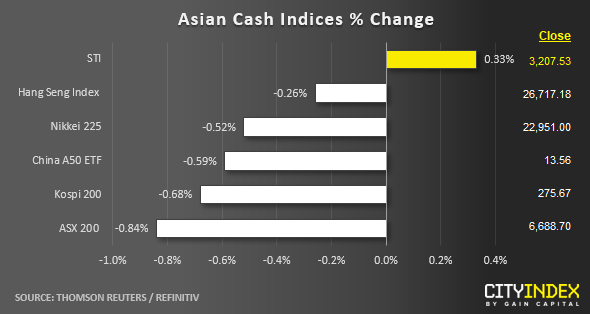

- Almost all Asian stock markets are in profit-taking mode after 3 to 5-days of consecutive gains as traders wait for the Fed FOMC meeting outcome and forward guidance on U.S. monetary policy out later at the 2nd half of the U.S. session today. Later after the close of the U.S. session, technology bellwether Apple will report its Q4 fiscal earnings and it will include 10 days of its new iPhone 11 sales.

- Also, the usual “hot and cold” cycle of U.S-China trade related news flow is making its way back to market again. Reuters had reported that a U.S. administration official said an interim agreement between U.S. and China may not be completed in time for signing in Nov but the official had added that it did not mean the deal was falling apart. This remark ran counter with the earlier optimism expressed by U.S. President Trump where he was expecting to sign “Phase 1 of the trade deal” with China’s Xi during the upcoming APEC Summit in 16-17 Nov.

- The worst performer today is Australia's ASX 200 which has declined close to -0.80% led by mining and natural resources related stocks. BHP, Rio Tinto and Fortescue Metals have shed as much as -1.3%, -1.2% and -1.6% respectively on the backdrop of a weaker iron ore futures price.

- Bucking the profit taking trend is the Singapore’s Straits Times Index (STI) which has recorded a modest gain of 0.33% led by the three banks; DBS, UOB and OCBC that have rallied by 1.30%, 0.64% and 0.93% respectively. UOB will report its Q3 earnings this coming Fri, 01 Nov before the market open.

- The S&P 500 E-Mini futures has traded almost unchanged as at today's Asia mid-session with a tight range of 5 points after a slide of 0.08% from its new all-time high level of 3046 printed yesterday in the cash S&P 500 index.

Up Next

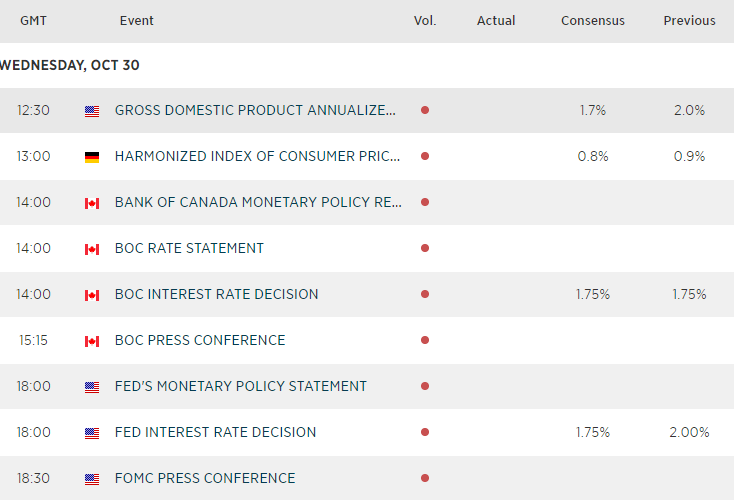

- US GDP data is the firt main event, with expectations for it to soften to 1.6% from 2% YoY prior. Fed Atlanta’s GDPnow however expects it fall to 1.7%, which may leave room for a small positive surprise head of the main event.

- The Fed and BOC hold their policy meetings, which will more than likely take precedence over the 2nd tier economic data available in the European. Check out the previews for a run down of how things could play out.

The U.S. dollar, Frogger & the FOMC

The BOC and The Canadian Dollar

FOMC Preview: Rate Cut Priced In, But Powell May Move Markets Regardless

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM