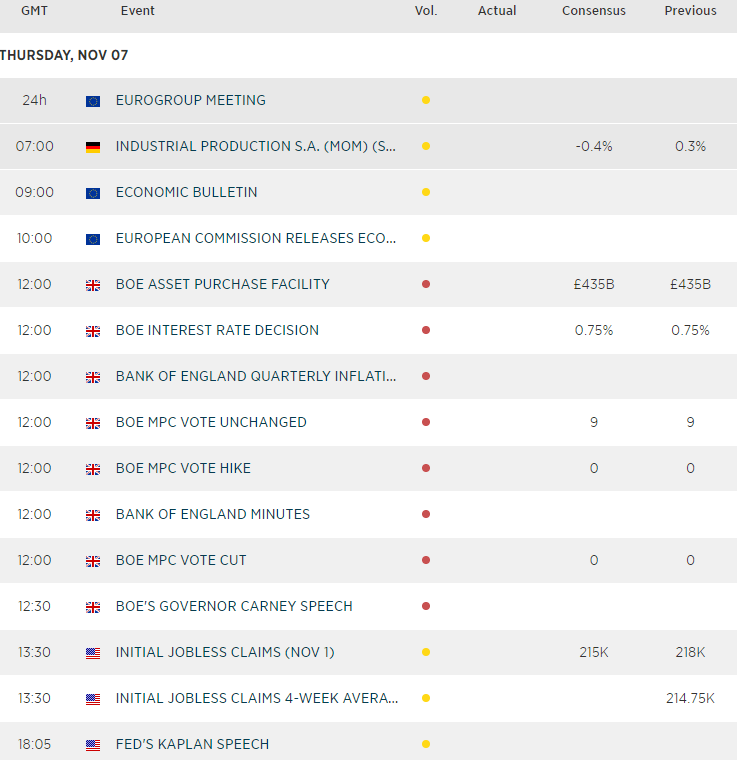

View our guide on how to interpret the FX Dashboard

FX Brief:

- Quiet ranges across the FX space, although most of the action was seen prior to the Asia open following weak employment data from NZ. With employment becoming a mandate for RBNZ, rising unemployment saw traders increase the odds of a rate cut to around 60% and weigh on NZD crosses.

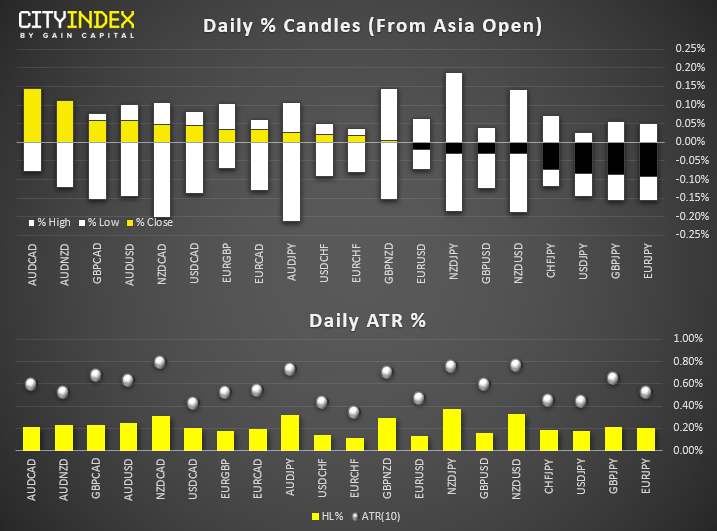

Notice that AUD is the strongest major following poor NZ employment data, as expectations for RBA to cut next month remains below 10% (hence why AUD/NZDF is sniffing around a key breakout level). - FX pairs remained in tight ranges overall, with pairs averaging around 38% for their ATR’s. Hopefully this leaves a few pips on the table for moves throughout the European and US sessions.

- USD/CNH remains below 0.7000 (just), EUR/USD sits on key support, EUR/GBP is considering a break lower. USD/JPY its just below 109.31 resistance as it considers a breakout. Let’s just hope these trade talks don’t reverse again otherwise markets will simply do the same.

- BOJ Sept Meeting Minutes: Members to pay closer attention to the chance momentum has been lost towards CPI target (basically, watch data closely as further easing is now on a meeting-by-meeting basis).

Equity Brief:

- Key Asian stock markets have started to see profit-taking activities as traders wait for more positive catalysts on the impending U.S-China “Phase One” trade deal agreement to be signed off by Trump and Xi.

- One of the sticking points is that China has requested U.S. to roll back some of the imposed tariffs in Sep as well as eliminate any new tariffs before any agreement can take place. So far, there is no clear take on this request from key U.S. officials.

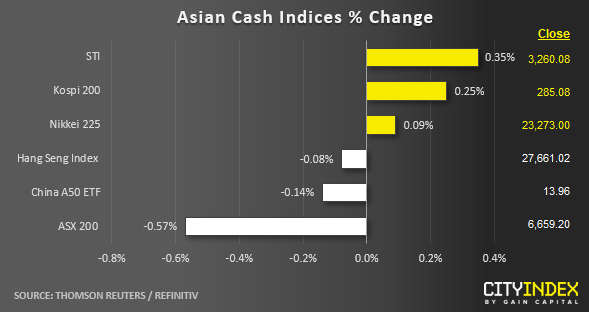

- The worst performer as at today’s Asian mid-session is Australia’s ASX 200 where it has dropped by -0.57%. Almost all sectors are trading in the red except for Basic Materials. The worst performer are industrials related stocks; the Industrial sector has tumbled by -1.8% follow by the Technology sector downed by -1.5%.

- Singapore’s Straits Times Index (STI) has managed to inch out a modest gain of 0.35%, on track for a third consecutive session of gains led by Hongkong Land and Jardine Matheson Holdings that have rallied by 3.13% and 2.40% respectively.

- Meanwhile, Japan’s services sector has shrunk for the first time in three years in Oct. The finalised Jibun Bank Japan Services PMI dropped to 49.7 in Oct from 52.8 in Sep due to the negative effectives caused by the recent powerful typhoon and a sales tax hike.

- The S&P 500 E-Mini futures is almost unchanged in today’s Asian session after a drop of -0.12% seen in the S&P 500 cash index at the close of yesterday, U.S. session.

Matt Simpson and Kelvin Wong contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM