Stock market snapshot as of [10/1/2020 1:12 PM]

- Global stock markets are on pace for a fourth consecutive day of gains. The insouciant attitude is even more remarkable as it comes ahead of Friday’s monthly payrolls, data which frequently stoke hypersensitive trepidation. The risk of volatility linked to U.S. employment surprise exists. However, as our Head of Research Matt Weller points out here, “even an outlier NFP reading for a single month is unlikely to meaningfully impact Fed policy, and by extension, market pricing.”

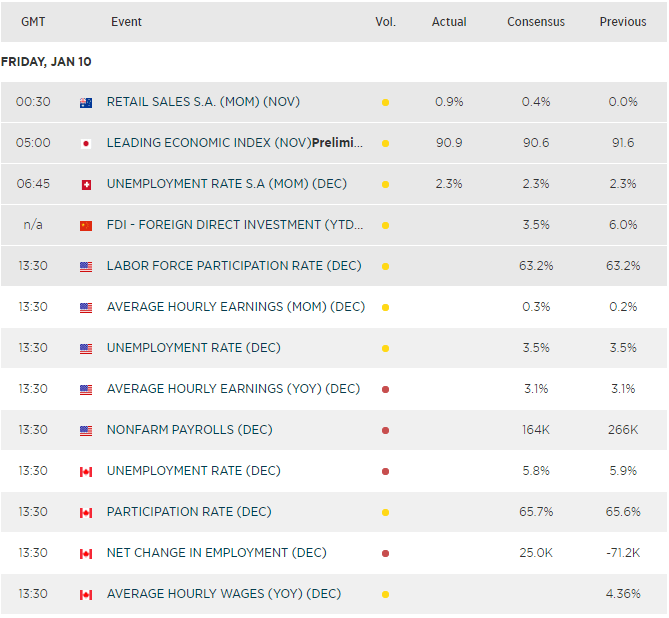

- Consensus forecasts point to payrolls easing from the extraordinary bump up to 266,000 in November to 162,000 in December. That would still be a print consistent with a solid labour market. Yet it would not cause a ripple on the surface of policymaking considerations. Likewise, expectations for 0.3% month-to-month wage growth, as per long-term run rate, would also be neutral. This probable heads-we-win, tails-we-win scenario helps explain the return to what looks like complacent sentiment on risky assets

- Having stepped back from the brink, Tehran and Washington appear to be staying back. Iran dismissed the notion that the Boeing 737 that crashed in a fire ball soon after the Islamic Republic began striking U.S. airbases in Iraq could have been shot down. Canada, the U.K. and Australia say the claim is backed by intelligence. Such an event was “not possible”, Tehran said, calling the allegations “psychological warfare”. The U.S. and Canada are among countries Iran has invited to aid investigations though. And Canada’s PM Justin Trudeau noted the aeroplane’s downing “may well have been unintentional.” This signal and the generally co-operative attitude amongst countries involved tends to neutralise, for now, yet another incendiary aspect of an extraordinary week

- Meanwhile, Federal Reserve Vice Chairman Richard Clarida characterised the U.S. economy as in a “good place”. Hours earlier, Beijing confirmed that Vice Premier Liu He will lead a delegation to Washington to sign the phase one trade deal between 13th-15th January

Stocks/sectors on the move

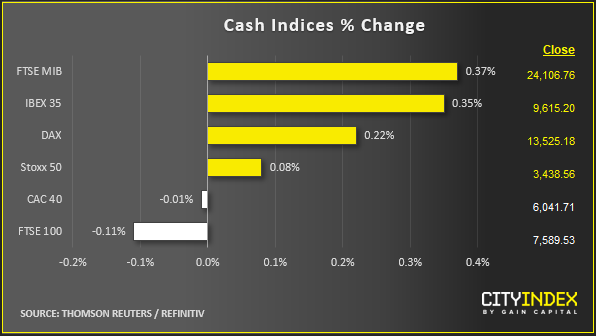

- It’s never the best sign when European utilities – supposedly a ‘bond-proxy’ sector top the STOXX sectors. Still, the main driver on Friday was comments from the CEO of Italy’s power group Enel. The stock traded 1.8% a while ago. “In most of the countries in which we operate, there is no longer any need for subsidies,” Antonio Cammisecra said, noting Enel can increasingly fund renewable projects by wholesale electricity deals

- Energy stocks as the second-best performing industry segment was more in keeping with the prevailing mood. A bullish JPMorgan note on European Energy shares played a part

- Boeing stock’s uplift in the prior session amid grim exoneration over the downed 737 faces some pullback. It disclosed staff comments to regulators investigating the plan maker’s beleaguered 737 Max model. The plane was “designed by clowns” who in turn were “supervised by monkeys”, according to one Boeing pilot. The stock was 0.5% lower in pre-market deals

FX snapshot as of [10/1/2020 1:12 PM]

View our guide on how to interpret the FX Dashboard

FX markets

- A firm dollar backs the relaxed view around data, with EUR/USD having touched its 50-day average of 1.019, which provided some support

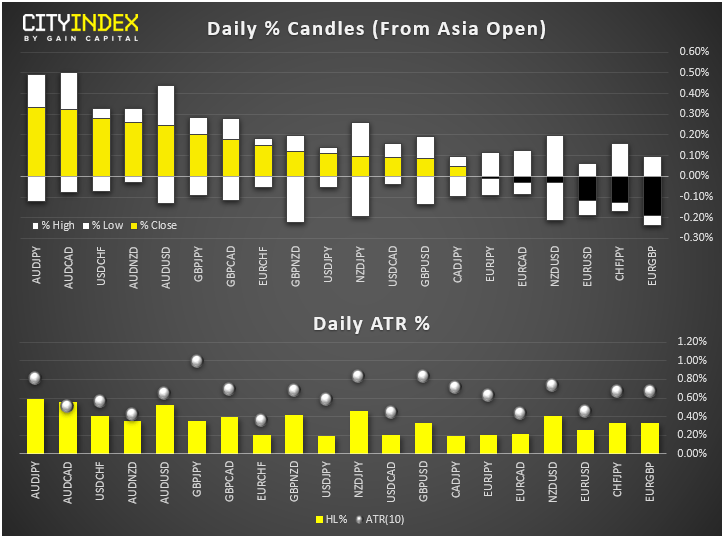

- All G10 majors eased vs. the greenback, though the yen’s massive vault earlier in the week meant that it continued to repay the heaviest toll, albeit lightly on Friday. USD/JPY is set to gain at least 1.4% this week

- Aussie keeps climbing and is one of the few to keep the dollar at bay as it retraces some of the late-2019 collapse. Australian retail data was the latest stimulus

Upcoming economic highlights

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM