Market Brief: Oil Surges 14% on Saudi Oil Strike, FX Impact Limited

- The weekend’s drone strikes on oil refineries in Saudi Arabia dominated markets, with oil prices ultimately finishing the day around 13% higher, its fourth-largest one day rise on record. Tensions in the region remain elevated with US authorities blaming the attack on Iran.

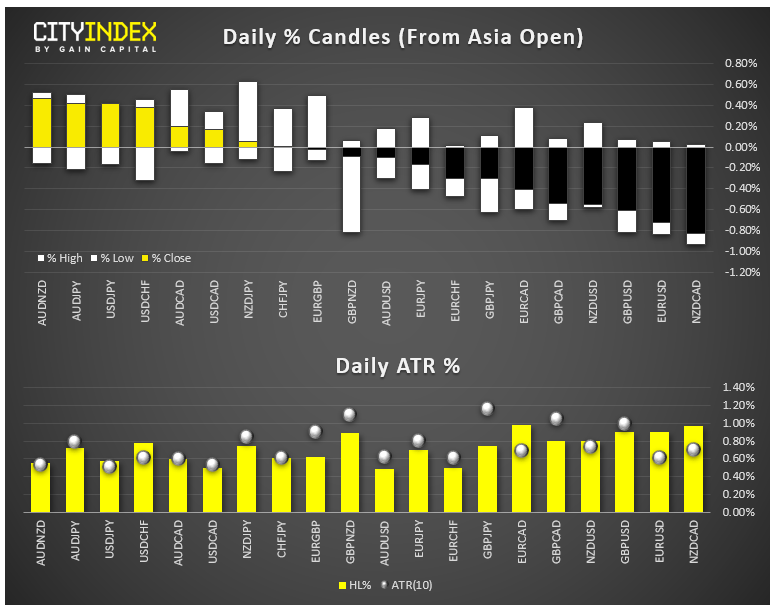

- FX: The oil-sensitive loonie was predictably the strongest major currency today, though it only rose about 0.3% against the greenback. European currencies brought up the rear, with both the euro and pound falling against their rivals.

- Commodities: Gold tacked on about 0.5% in general risk-off trade.

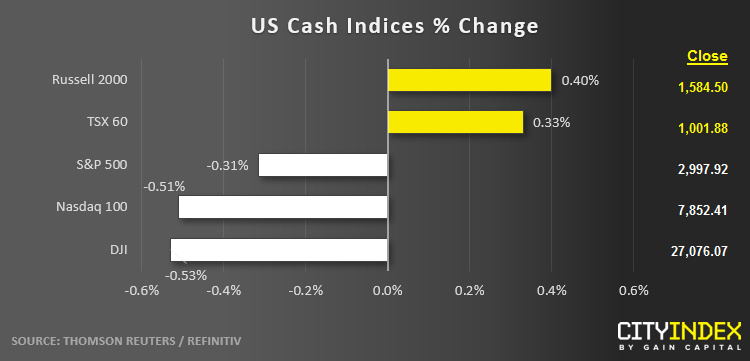

- US indices finished roughly 0.5% lower today, as oil prices represent a key cost for most firms (not to mention the potential impact on consumer spending).

- Energy (XLE) was by far the strongest sector, gaining roughly 4% in its biggest one-day rise this year. Material stocks (XLB) were the weakest sector on the day.

- Stocks on the move:

- Oil companies were big beneficiaries of the surge in oil prices, with megacaps Exxon Mobile (XOM, +1%) and Chevron (CVX, +2%) both bucking the bearish trend in broader markets.

- General Motors (GM) dropped -4% after 50k UAW workers began a potentially long strike.

- Overstock.com (OSTK) fell another -21% to unwind about half of the short squeeze that was driving the troubled retailer in the first half of the month.

Latest market news

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM