Market Brief: Oil and Poloz Push USD/CAD Back Below 1.33

View our guide on how to interpret the FX Dashboard.

- Trade headlines dominated markets today:

- The WSJ reported China has invited the US to another round of talks around a “phase one” trade deal, while the US is reportedly considering delaying the scheduled December 15th tariffs regardless of whether there’s a deal or not.

- Meanwhile, Beijing is closely watching the status of the US bill supporting Hong Kong protestors.

- Separately, the USMCA trade deal is nearing completion, with some lawmakers still expressing optimism that it could be signed later this year.

- Finally, Politico reported that the White House is considering a trade investigation into EU automobiles.

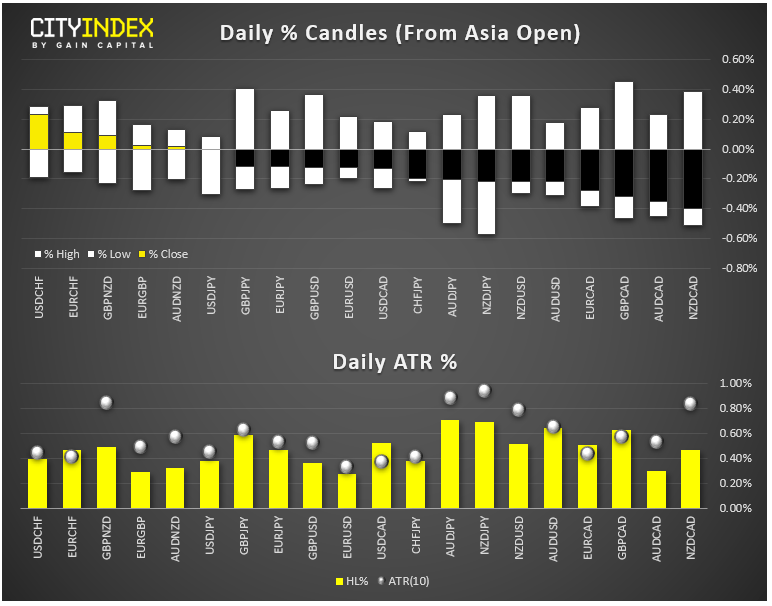

- FX: The Canadian dollar was the day’s strongest major currency, bolstered by less dovish comments from BOC Governor Poloz and rising oil prices. The New Zealand dollar was the day’s weakest currency.

- Commodities: Oil tacked on another 2% to trade at a nearly 2-month high today, while gold slipped less than -1%.

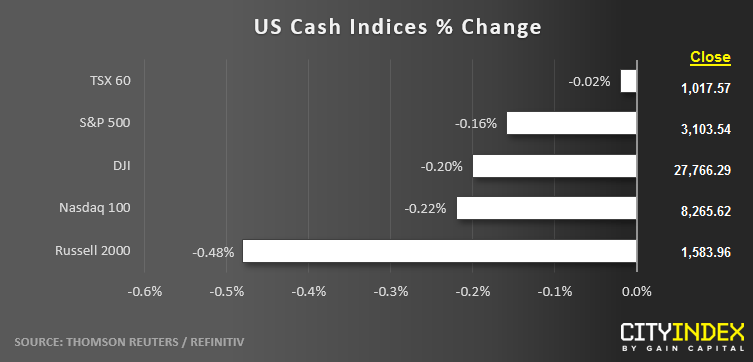

- US indices closed moderately lower on the day following a late fade.

- Energy (XLE) was the strongest major sector for the second straight day. REITs (XLRE) brought up the rear.

- Stocks on the move:

- Broker Charles Schwab (SCHW, +7%) is reportedly looking to buy TD Ameritrade (AMTD, +17%).

- Macy’s (M) shed -2% after the department store missed analysts’ sales estimates and lower full-year guidance.

- General Motors (GM) ticked -2% lower on an announcement that the company would have to recall over 600k trucks.

Latest market news

Yesterday 08:33 AM

Latest Forex articles

April 17, 2024 02:40 PM

April 17, 2024 04:47 AM

April 16, 2024 12:00 PM

April 16, 2024 04:24 AM