View our guide on how to interpret the FX Dashboard

- Earlier in the session, the NZ government announced further infrastructure spending alongside a boost in fiscal spending in 2020. However, SEEK job advertisements since September’s spike has been lacklustre, which brings doubt to the strength of the employment market as we head into 2020. That said, market reaction may be a little overdone considering the positive news flows seen from NZ of late.

- Markets remain in a holding pattern whilst Trump decides whether to adds tariffs to $160 billion of Chinese goods over the weekend. Whilst there have been mixed reports over a potential delay, advisors are to meet with Trump over the coming days to hopefully finalise the decision (or leave the markets risk to weekend gaps if no decision has been announced before Sunday’s deadline).

- House Democrats formerly announced impeachment charges against President Trump, a move which is likely to result in a Republican-led Senate trial early next year.

Price Action:

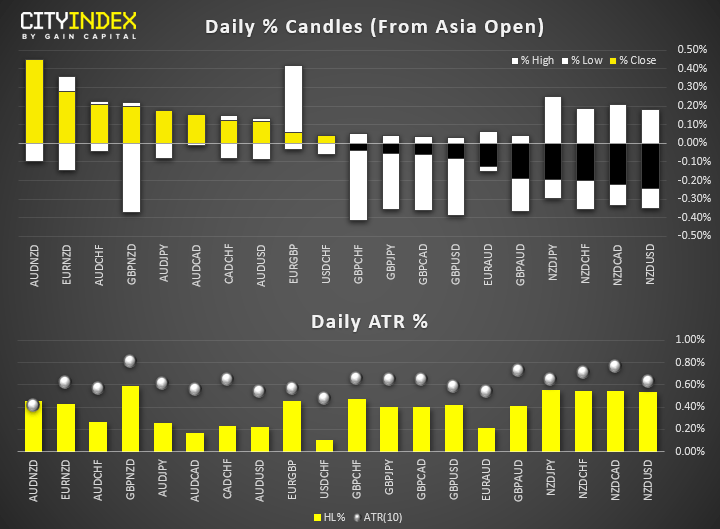

- NZD is the weakest major and the most volatile (as it quiet elsewhere ahead of today’s FOMC meeting and CPI data).

- AUD/NZD is the largest gainer and enjoying its largest daily gain in a month. Having failed to break below a bullish trendline and the 1.40 handle, it likely marks the beginning of a much-needed correction. However, it’s moved 108% of is typical ATR so prone to mean reversion if looking to enter on a lower timeframe.

- NZD/USD and NZD/CAD are the weakest pairs although daily range is yet to meet its ATR. Outside of NZD pairs, volatility remains low, with an average range to ATR around 50%.

Equity Brief:

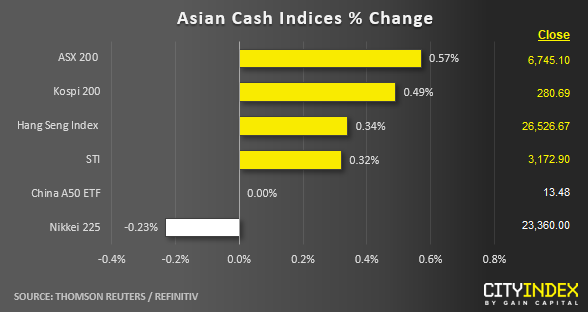

- Key Asian stock markets are again trading in a cautiously optimistic mode where modest gains between 0.25% to 0.50% have been recorded in Singapore, Hong Kong, South Korea and Australia markets while no change in China A50 and Japan’s Nikkei 225 has now traded into the red with a minor loss of -0.23%.

- Yesterday’s we had the usual dose of optimistic U.S-China trade related news headline quoted by media from “unnamed” sources after the initial slide in equities prices seen at the start of the European session. The media stated that U.S. and China officials have planned for a delay on the additional tariffs impose on China’s products that are set to kick in on 15 Dec as talks progress for the finalisation of the Phase One trade deal.

- On the other hand, U.S. White House Trade Adviser, Navarro said that he was not aware of any indication of the 15 Dec tariff delay.

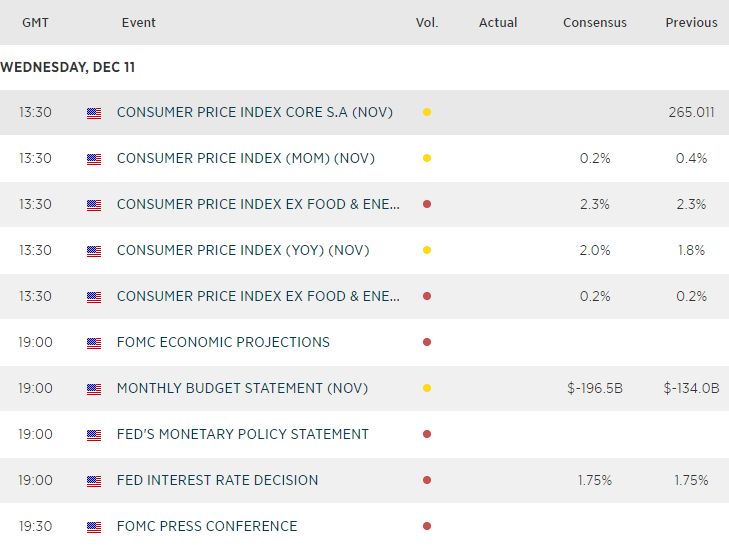

- For the rest of day, do expect more churning and sideways movement as we head into Fed FOCM monetary policy outcome out later at 1900 GMT. Also, do take note of Fed’s Chair Powell press conference at 1930 GMT where he is likely to be “probed” by the media on the state of the short-term funding repo market especially a research report published by Credit Suisse yesterday on the risk of a liquidity squeeze in the repo market and its potential negative ramifications as we head into the upcoming year-end turn.

- Japan 225: Yesterday’s slide has managed to hold at 23250 predefined minor range support (printed a low of 23263 in 10 Dec, European session). No change, still expect sideways movement between 23650 (medium-term range resistance in place since 07 No 2019) and 23250. Only a break below 23250 sees a deeper slide towards the medium-term range support area of 23150/23050 (also the minor ascending trendline in place since 21 Nov 2019 low & 61.8% retracement of the recent push up from 03 Dec low to 09 Dec 2019 high).

- Hong Kong 50: Staged the minor expected slide to retest yesterday, 10 Dec Asian session low of 26264 during the European session (printed a low of 26238). It has now bounced back towards its minor range resistance at 26600. Expect churning within 26238 and 26600. A break below 26238 sees a further slide towards 25920 swing low of 03 Dec 2019.

- Australia 200: Yesterday’s losses have met reversed via a minor V-shaped recovery after it printed an intraday low of 6671 in the European session. Hourly RSI oscillator remains above the 50-level. Expect sideways movement between 6780 (03 Dec minor swing high & 61.8% retracement of the previous slide from 29 Nov high to 03 Dec 2019 low) and 6670.

- Germany 30: Slide down towards 12900 (03 Dec 2019 swing low area) as expected a staged a bounce off from it thereafter. The bounce has stalled below a minor descending trendline from 02 Dec 2019 high now acting as a resistance at 13120. Expect a potential slide back to retest 12960/12900 within a medium-term range resistance in place since 19 Nov 2019.

- US SP 500: Slide/retracement target/support hit at 3120 as expected (printed an intraday low of 3115 in yesterday’s European session). Expect churning within 3147 (minor descending trendline from 02 Dec 2019) and 3115. A break below 3115 sees a further potential slide towards 3106 next (05 Dec 2019 minor swing low & Fibonacci retracement/expansion cluster).

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Dollar articles

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM