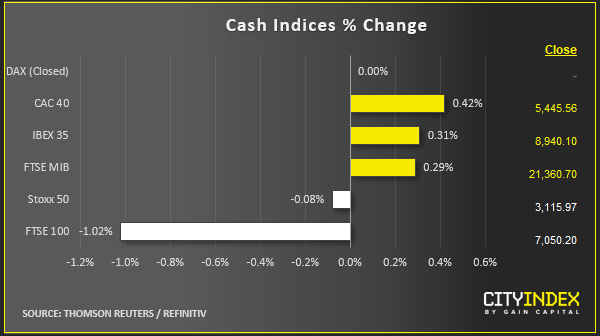

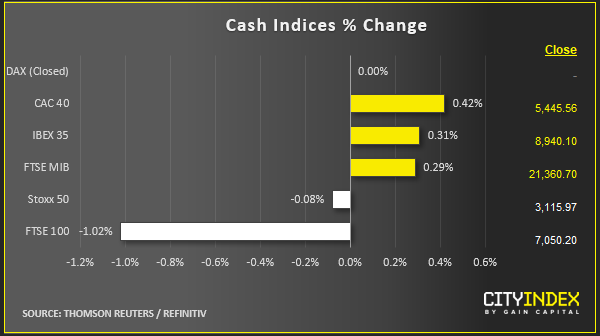

Stock market snapshot as of [3/10/2019 1:51 PM]

- A day after stocks and other risk-laden assets were sold the hardest since August it’s been a fairly positive morning in Europe, though admittedly, one of the most pivotal stock markets, Germany’s DAX was closed for a public holiday

- The tentative rebound is all the more remarkable as it comes after Washington, somewhat unexpectedly, announced tariffs on $7.5bn worth of European goods. In some ways, the move finally drops the axe on European trade and markets that has been feared since the White House embarked on an aggressive and provocative trade policy path around two years ago. The key difference in this latest twist is that it stems from action that pre-dates the current administration. U.S. President Donald Trump effectively got the go-ahead to levy new 10%-25% duties following a case the U.S. brought against the EU 15 years ago. In the largest award ordered in the international trade arbiter’s history, the WTO authorized an annual retaliatory charge of up to $7.5bn after ruling that pan-European plane maker, Airbus, received illegal government subsidies

- The muted market reaction is probably linked to the relatively contained size of the U.S. move: note that Airbus shares have led France’s CAC-40 index higher with a rise of 3.5%, suggesting that investors may have feared a more punitive sanction was possible. Furthermore, whilst some non-industrial products are also implicated by the new tariffs, e.g. certain food like pork, cheese, olives food stuffs, wines and whiskies, leather goods were dropped from an initial list, enabling shares of European luxury groups to buttress the region’s equity rally

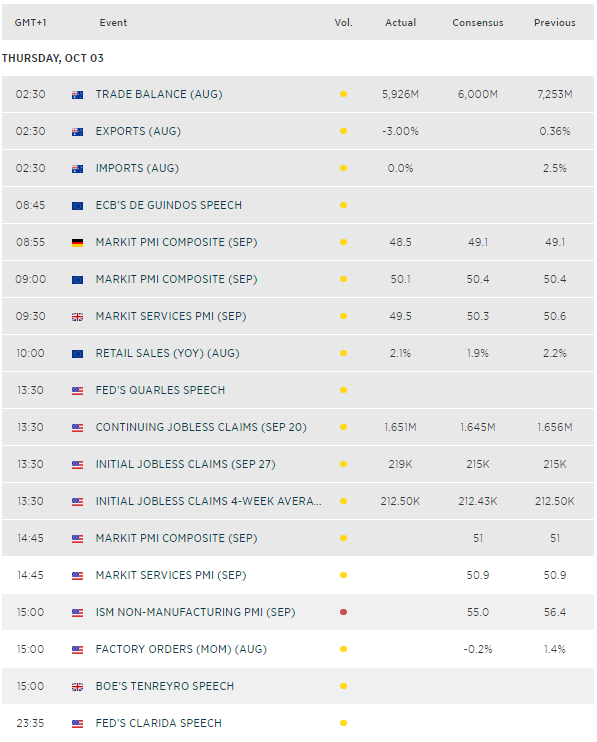

- Nevertheless, it’s ‘early days’ to declare the sharp downdraft against risk assets seen this week over, largely because the most pivotal of the raft of critical data releases of the week remain ahead. On Thursday, the U.S. Institute for Supply Management (ISM) will release the second tranche of its highly influential monthly business surveys, this time for the ‘non-manufacturing’ sector. A day after the ISM’s key manufacturing gauge printed sharply lower than expected, if measures of the much larger U.S. services sector also disappoint, Wednesday’s selling might look like a walk in the park by comparison

Stocks/sectors on the move

- Despite a more measured retreat on Thursday, Europe’s 600-share STOXX had slipped into the red a short while ago, weighed down by its Energy component. This is the fifth consecutive session of losses for Brent crude oil futures, partly with an eye to a quicker than expected resumption of near-full production at Saudi Arabia’s key processing facilities following a missile attack

- Falls by Financials and Materials also over-shoot those by other super sectors, drawing limits around any relief from relatively limited Washington tariffs on the EU, so far. Automobiles & Parts – the industry most clearly in the firing line for further possible U.S. tariffs—collectively fell 0.4%. Luxury group shares, LVMH, Christian Dior, Kering, Hermes, mostly rose after new Washington tariffs spared leather goods. (Though not Britain’s Burberry, which slipped 0.6%)

- U.S. stocks to watch include Tesla, which posted another set of record deliveries in the just-ended quarter, though still fell short of claims by CEO Elon Musk. The stock points 5% lower. Constellation Brands, a rival of European booze makers that have been hit with new tariffs, was losing 3% ahead of Wall Street’s start, even after its Q2 EPS topped forecasts and it raised guidance. Bed Bath & Beyond is similarly out of luck, eyeing a 6% loss despite Q2 adjusted EPS exceeding forecasts. GoPro missed again. Shares may tank 16%. Pepsi beat; shares are inching up 2%

FX snapshot as of [3/10/2019 1:51 PM]

FX markets

- Sterling/Brexit check-in: Boris Johnson has just outlined his new Brexit plan to Parliament, though sterling’s reaction was fairly muted as it didn’t deviate from previously leaked extracts much, nor are the chances of a favourable reception from the EU much higher than initially suspected. Ireland’s foreign minister Simon Coveney said there is “no point having proposals that one side can veto”. However, he conceded that he saw “progression” in the UK’s position

- A little optimism goes a long way. Sterling charges higher against the euro, franc, loonie, but not so much against the yen or Aussie

- Generally, the dollar continues to ease off its highest levels since May 2017 as Treasury yields resume their long slide on global growth concerns. The still lower-yielding euro sees among the least benefits as it pirouettes around $1.096

Upcoming economic highlights

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Brent articles

February 21, 2024 03:30 PM

November 28, 2023 09:05 PM

November 20, 2023 08:26 PM

November 8, 2023 06:11 PM