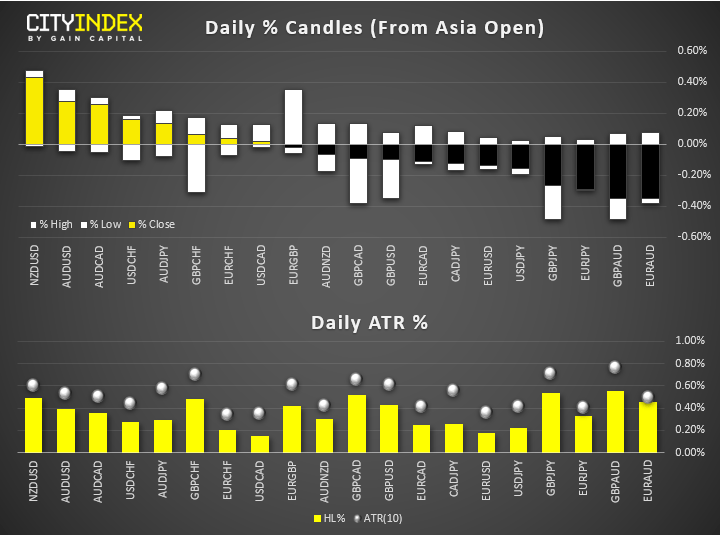

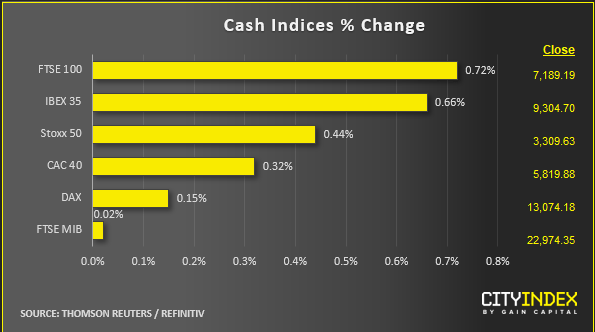

- Market update at 13:00 GMT: Commodity dollars were leading in FX with euro and pound being the laggards. Stocks were higher, gold and oil flat.

View our guide on how to interpret the FX Dashboard

- Investors are awaiting key employment data from North America, with the US non-farm payrolls and Canadian employment reports both due at 13:30 GMT. NFP expected to print 181K on the headline front while average hourly earnings are seen rising 0.3% month-on-month in November compared with 0.2% the previous month. Canadian employment is seen rebounding by 10K after an unexpected drop in the previous month. Given the BOC’s hawkish rate hold in mid-week, a strong Canadian jobs report could see the commodity dollar outshine its southern neighbour - and especially if oil prices were to spike higher in the aftermath of the OPEC+ decision.

- The so-called OPEC+ group are meeting to discuss production cuts in an effort to head off global oversupply in 2020 and sustain prices. According to Reuters, citing sources, Saudi Arabia and Russia have won the backing for deeper output cuts from OPEC and allied oil producers. Collectively, they have apparently agreed to an extra 500,000 barrels per day (bpd) in cuts for the first quarter of 2020. Oil prices were little-changed following a sizeable rebound over the past few days.

- Jeremy Corbyn, the Labour Party leader, says he has a confidential government report that reveals "cold, hard evidence" that there will be "customs declarations and security checks" between Northern Ireland and Great Britain, under Boris Johnson's Brexit deal. PM Johnson and Corbyn will go head-to-head in a live TV election debate at 20:30 GMT on BBC One tonight.

- Meanwhile in France, President Emmanuel Macron faced the biggest protest since he took office more than two years ago, as hundreds of thousands took to the streets in protest of the controversial pension reform bill. Labour unions have extended their protests until Monday.

- There is no end in sight for the recession in Germany’s manufacturing industry. Fresh data this morning revealed an unexpected 1.7% monthly drop in industrial output. The falls were concentrated in production of capital goods, including tools, buildings, vehicles, machinery and equipment. This comes on the back of woeful figures published on Thursday that showed manufacturing orders fell by 0.4% in October. The German economy narrowly avoided a technical recession in the last quarter, but with manufacturing activity continuing to deteriorate, this could spill over to services and hurt employment, resulting in another quarter of negative economic growth.

- Another major country trying to avoid a recession is the world’s third largest economy, Japan. Prime Minister Shinzo Abe has launched the nation’s first fiscal stimulus since 2016. After months of underwhelming data, Mr Abe revealed a larger-than-expected ¥13.2tn ($121bn) package. The large fiscal stimulus package is introduced to help repair typhoon damage, upgrade infrastructure and invest in new technologies. This comes as Japanese exports are continuing to shrink while the recent sales tax hike continues to bite the consumer - the latest data showing household spending plummeted 11.5% last month or 5.1% on a YoY basis.

- Stocks remain supported for the time being. Trump remains upbeat on US-China trade talks, saying they’re “moving along very well”. But he’s been saying this for a year now, so make of that what you will – words of my Asian colleague Matt Simpson.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM