View our guide on how to interpret the FX Dashboard

FX Brief:

- There was a small burst of risk-on following reports that US and China had agreed to continue with phase one talks. Given this doesn’t actually cover any new ground at all (as we’ve been here already…) then its hard to envisage a spill-over effect in the European and US sessions. S&P500 E-minis touched a new high and safe-haven currencies (CHF and JPY) saw minor outflows yet moves were later reversed.

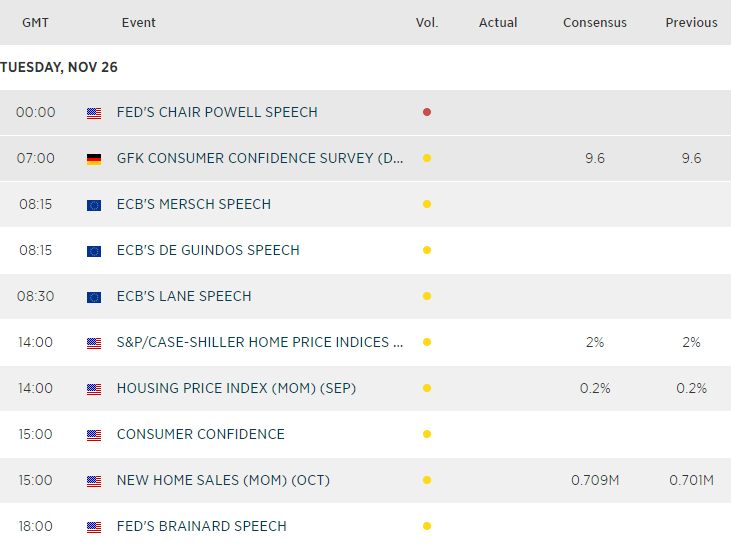

- RBA’s Assistant Governor Guy Debelle warned that higher wage growth is needed to hit their 2-3% inflation target it will take a sustained fall I unemployment to lift the economy. And that was before a read of Australian consumer sentiment plunged to a 4-year low, with future financial conditions also falling by 4.4%. (take note that RBA’s Governor Philip Lowe is due to speak at 09:00 GMT).

- New Zealand retail sales rose in the third quarter by 1.6%, beating expectations of 1.5% and up from 0.2% prior.

Price Action:

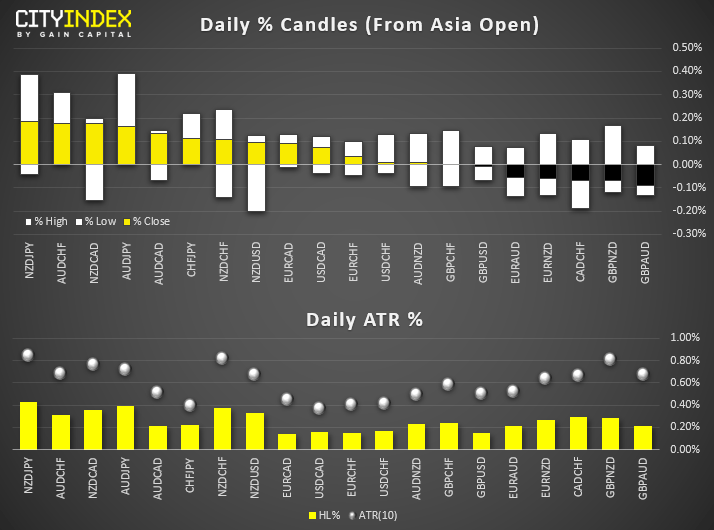

- DXY trades in a tight range within yesterdays Doji candle, which suggests the potential for mean reversion whilst below 98.45 resistance.

- USD/JPY briefly touched a 2-week high, although key resistance around 109.50 is likely to cap any breakout without confirmation of a trade deal. At time of writing, there’s potential for a bearish hammer on the daily chart to close beneath resistance.

- USD/CHF has parity within its sites, yet yesterday’s bearish pinbar beneath it brings the potential for a dip lower from key resistance.

- AUD/USD is teasing support at 0.6770 but runs the risk of a mild rebound, with DXY below resistance.

- CAD/JPY tested the upper bounds of the bullish wedge it remains confined within. We’re still monitoring it to see whether it will rise in line with the wedge and bullish channel or invalidate both patterns with a bearish breakdown.

Equity Brief:

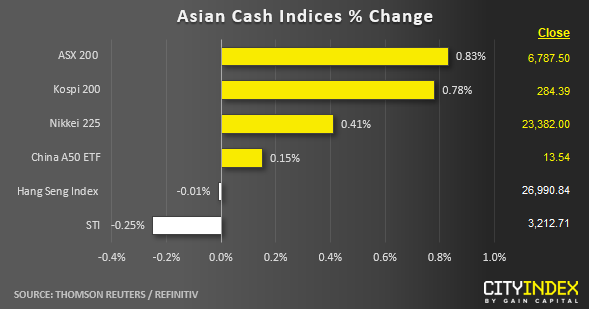

- Asian stock markets have opened higher at the start of the today’s Asian session taking the cue from the positive performances seen overnight in the U.S. stock markets where the S&P 500 and Nasdaq 100 have recorded fresh all-time highs.

- China state related media, Xinhua has reported China Vice Premier Liu He, the top trade official has held a telephone call today with U.S. Trade Representative Lighthizer and Treasury Secretary Mnuchin where both sides have reached a consensus on properly resolving related issues and agreed to maintain communication on remaining issues in consultation on the “Phase One” trade deal.

- Several key Asian stock markets; Japan’s Nikkei 225, China A50 and Hong Kong’s Hang Seng Index (HSI) have seen their initial gains fizzled out from their respective intraday highs together with the worst performer, Singapore’s Straits Times Index (STI) that is downed by -0.25% so far.

- Hong Kong’s chief executive Carrie Lam, first official press conference after the landmark victory by the pro-democracy camp in the local district council election has offered no new concessions to protestors that may spark fresh round of demonstrations again over the past six months of social unrest.

- Alibaba’s secondary listing in Hong Kong is off to a roaring start where it has rallied by 6.9% to HK$188.20 in the mid-session from its listing price of HK$176.00. Alibaba’s HK is now trading at a small premium of 0.96% over its U.S. listed ADS share of US$190.45 on NYSE based on yesterday’s closing price where eight Alibaba’ HK shares is worth the equivalent of one NYSE listed ADR.

- The S&P 500 E-Mini futures is trading almost unchanged as at Asian mid-session from yesterday, 25 Nov U.S. session close of 3131 after an initial push up to print a current intraday high of 3145.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM