Market Brief: Much Ado About Brexit…But No Deal Yet

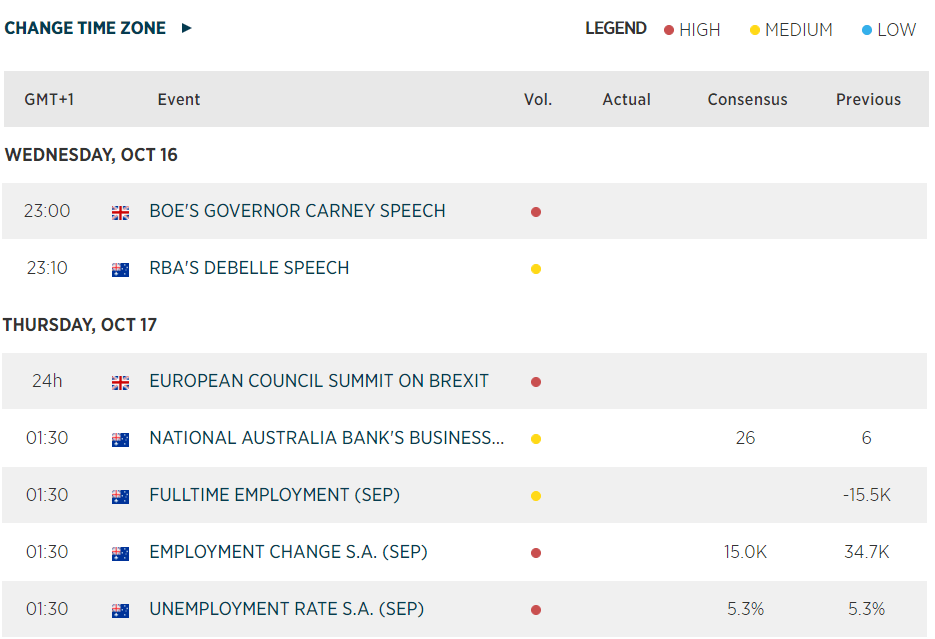

- A cacophony of Brexit headlines whipsawed markets back and forth today, with the UK’s previous recalcitrant DUP party reportedly moving closer to accepting the most recent proposals. As of writing (and as far as your humble author can tell), it appears that the Prime Minister and EU have agreed on all the previously contentious issues except for VAT, and ironing out a full agreement will be tomorrow’s order of business. Parliamentary approval could still prove to be a major stumbling block.

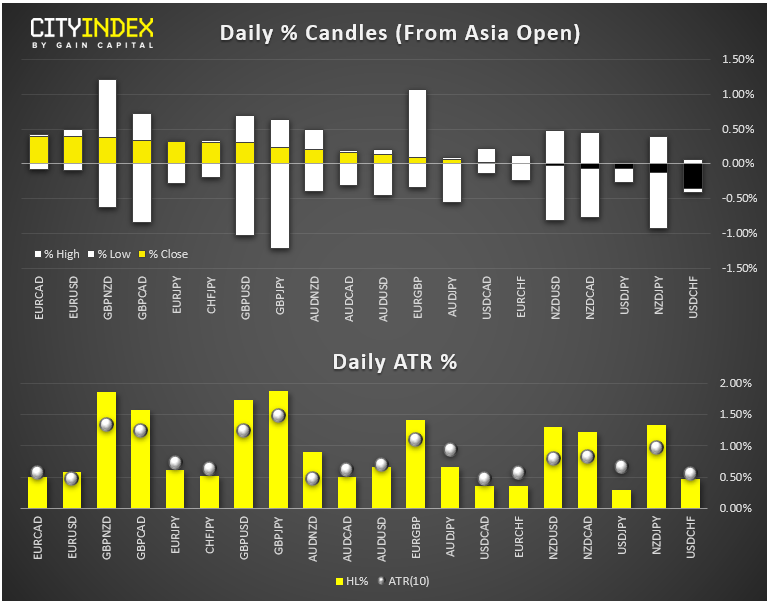

- FX: The euro and Swiss franc were the day’s strongest major currencies, while the New Zealand dollar brought up the rear.

- US data: Retail Sales (September) declined -0.3% m/m, well below the +0.3% reading expected – this marked the first decline in seven months. Core Retail Sales decline -0.1% vs. +0.2% eyed. Last month’s retail sales report was revised higher, taking some of the sting out of the shocking headline reading.

- Commodities: Both oil and gold edged higher today, gaining slightly less than 1%.

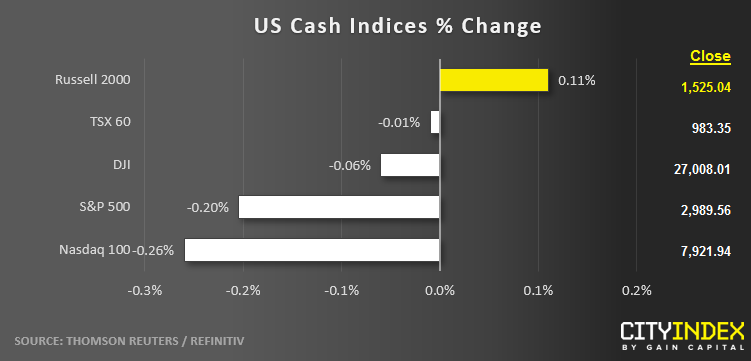

- US indices closed modestly lower at the end of a choppy day.

- Consumer Discretionary stocks (XLY) were the strongest major sector, while Energy (XLE) was the weakest despite the rise in oil prices.

- Stocks on the move:

- General Motors (GM) gained another 1% after reaching a tentative agreement with the UAW union to end the month-long strike. The UAW votes on the deal tomorrow.

- Bank of America (BAC) tacked on 2% after reporting stronger-than-expected earnings.

- Amidst growing competition from the likes of Disney and Apple, Netflix (NFLX) reported better-than-expected earnings, but weaker revenues, guidance, and subscriber growth. The stock is trading up 4% in volatile after-hours trade, though tomorrow’s open will provide a better indication of traders’ outlook for the firm.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM