View our guide on how to interpret the FX Dashboard

FX Brief:

- It was gaps galore at market open as tensions in the Middle East escalated over the weekend. The $36 move in gold, re-test of $64 resistance on WTI and gap lower on the S&P futures underscored the negative tone form geopolitics as we kick off the new year.

- French President Macron spoke with Trump and said Iran should avoid “destabilising” actions. Japan’s PM Abe has called for all parties to avoid escalating tensions in the Middle East.

- Australian manufacturing PMI contracted for a second consecutive month at 48.3, although slightly above the prior read of 48.1. Japan’s manufacturing read contracted for an eleventh straight month and remains at multi-year lows “with little hope of a turnaround” according to HIS Markit, who compile the survey.

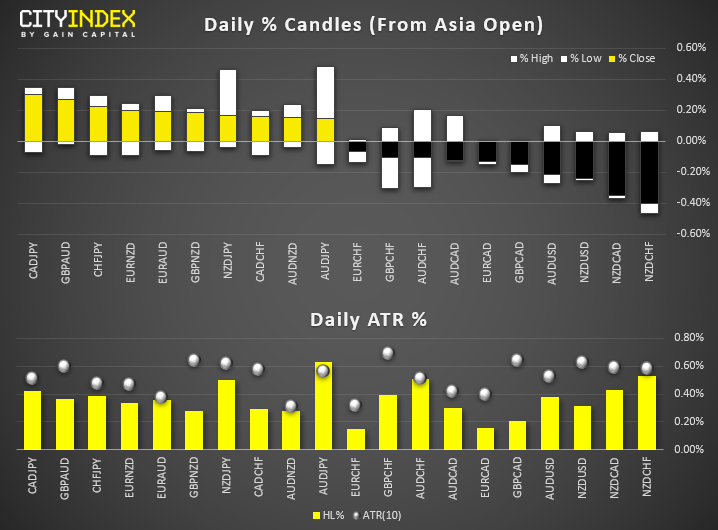

- NZD and AUD are the weakest majors, CAD and CHF are the strongest. Still, volatility is lower than Friday’s explosive move, although 11 of the 28 pairs we track have met or exceeded their 10-day ATR.

Price Action:

- AUD/USD and NZD/USD are teasing key support levels near Friday’s low. Whilst this leaves potential for a minor bounce, the bearishness of the declines over Thursday and Friday do suggest we may see another low in due course after a corrective bounce (assuming one is even seen).

- USD/CAD continues to consolidate between 1.2950 and 1.3015 (the 2019 low). Keep an eye for a breakout either side of the congestion zone as it could pave the way for its next directional move.

- USD/CHF produced a spinning top doji on Friday. If prices remain beneath Friday’s high (0.9744) then we could assume the correction has ended and for it to revisit the lows. A break above 0.9944 brings 0.9440 into focus and assumes a deeper correction against the dominant, bearish trend.

- USD/JPY made a minor low today but ultimately remains above 107.88 support. Given it didn’t follow Friday’s move (like gold and WTI did) then it suggests we could be in for a corrective bounce, unless Middle East tensions escalate further.

Equities Brief:

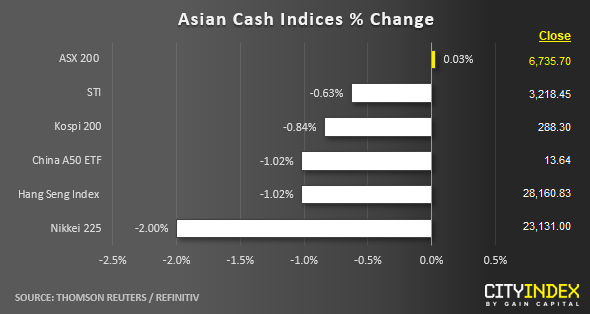

- A sea of red for major Asian stock markets as we kick start the first full week of trading for 2020. Rising geopolitical risk in the Middle East that has been triggered by the assassination of an Iran top military leader by U.S overshadowed the “feel good” factor from the upcoming U.S-China Phase One trade deal official signed off schedule on 15 Jan in the U.S. White House.

- U.S. President Trump has “doubled down” his hawkish stance on Iran where he has threatened to target Iranian cultural sites if Tehran retaliates. In addition, Trump has threatened to impose sanctions on Iraq as Iraq’s parliament has voted to expel remaining U.S. troops in Iraq. Meanwhile, Iran government has abandoned limitations on enriching uranium, stoking fears of using nuclear weapons as a form of retaliation against U.S.

- China Caixin Services PMI for Dec has fallen to 52.5 in Dec from a 7-month high of 53.5 printed in Nov which indicates a slow-down in growth in the services sector. A positive factor to note is the New Orders component where rose the most since Sep on the back of new product offerings.

- Japan’s manufacturing sector has continued to contract for 8 consecutive months since May 2019. The finalised Jibun Bank Japan Manufacturing PMI for Dec was revised down to 48.4 from an earlier flash estimate of 48.8 and was also lower from Nov finalised data of 48.9.

- Aside from geopolitical and marco news flows, a mysterious viral pneumonia outbreak has spread in Wuhan, a central Chinese city with a population over 11 million that has led to speculation of a resurgence of the highly contagious Sars virus in 2003 that also triggered a massive sell-off in Asian stocks. Medical experts in China has so far downplayed the fears and stated the viral pneumonia outbreak is not Sars, Mers or bird flu.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 08:15 AM

Latest Dollar articles

Yesterday 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM