Equity Brief:

- Key Asian stock markets have almost given up the gains accumulated since the start of the week; taking the cue from the sell-off seen in U.S. stocks overnight. Right now, the U.S. administration has upped its hawkish stance towards China where visa bans have been imposed on Chinese officials linked to violation of human rights over Muslims in the Xinjiang region on top of the recent blacklist of eight Chinese technology firms over similar human rights violation.

- The mood has turn sombre for a positive break through on the upcoming two days of high-level U.S-China trade negotiation talks in Washington that will kickstart on Thurs, 10 Oct. Also, SCMP have reported that the highest ranking official from the Chinese delegation, Vice Premier Lui He will not carry the title of “special envoy” for the upcoming trade talks, an early indication that Lui He has received no particular instructions from China President Xi and a source has told SCMP that the Chinese delegation may cut short its stay in Washington.

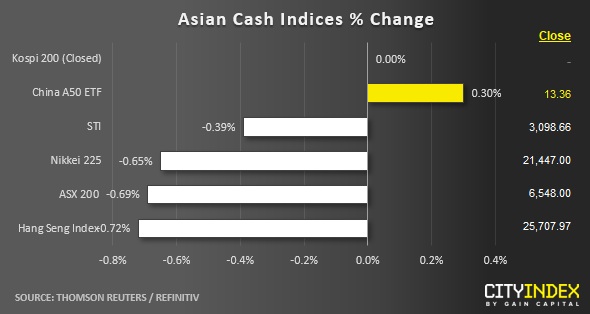

- Hong Kong’s Hang Seng Index has continued to slide where it recorded a slide of -0.71% as at today’s Asia mid-session towards its 10-day low of 25600. Financials, properties and technology related stocks are the worst performers where Hang Seng Bank, AAC Technologies and CK Asset Holdings have declined by -3.39%, 3.26% and -2.20 % respectively.

- South Korea’s Kospi 200 is closed today for a public holiday. The S&P 500 E-mini futures has managed to shape a bounce of 0.20% to print a current intraday high of 2903 in today’s Asian session after a decline of -1.56% seen in the U.S. session. However, the current bounce does not look like a potential bullish reversal from a technical analysis perspective.

FX Brief:

- After a sell-off in the GBP seen yesterday (the weakest currency in the overnight U.S. session) reinforced by the dim prospect of getting EU approval on U.K PM Boris Johnson’s latest Brexit proposal, the GBPUSD has traded in a tight range of 13 pips in today’s Asian session.

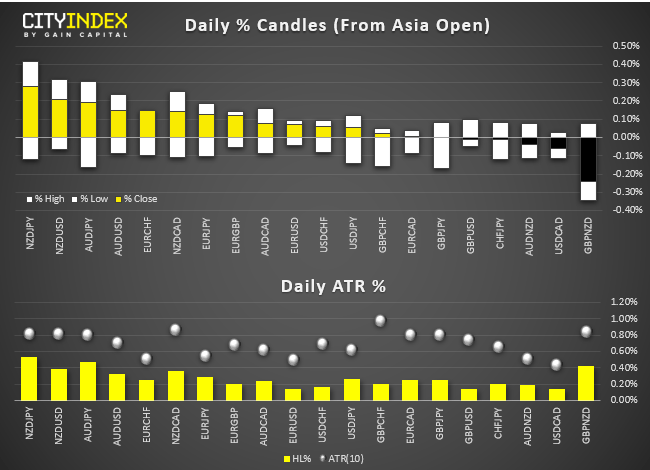

- The antipodean currencies are the best performers so far where the NZD/JPY AUD/JPY, NZD/USD and AUD/USD have recorded modest gains between 0.15% to 0.28% but these gains are questionable in the backdrop of an escalation in political tension between U.S and China where it may derail any positive outcome on the upcoming high-level U.S-China trade talk.

Up Next

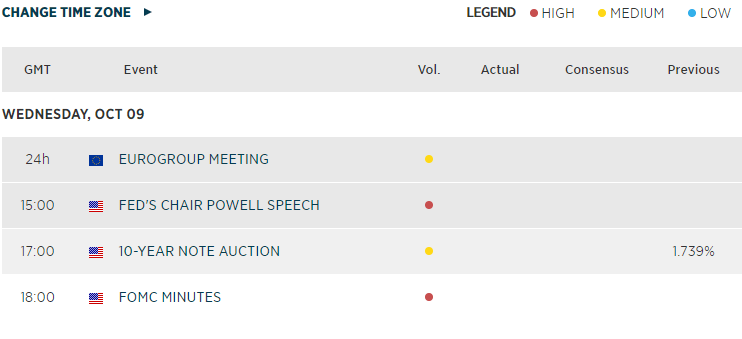

- Fed Chair’s Powell speech (the third & last for this week) and FOMC minutes on the Sep meeting. In yesterday’s speech at the National Association for Business Economics Annual Meeting, Fed Chair Powell has indicated that Fed will start to grow its balance sheet soon to counter the recent turmoil seen in the repo market and open the door for another interest rate cut in the upcoming Oct FOMC meeting.

Economic Calendar

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Today 08:15 AM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM