View our guide on how to interpret the FX Dashboard

FX Brief:

- Trade optimism made a return at the end of the week in Asia, after White House economic advisor Larry Kudlow said that US and China were close to a trade deal. (Getting that familiar feeling of déjà vu yet again…). Well, believe it or not, equities liked it and we saw carry trades come back into fashion.

- BOC’s Poloz said that wage inflation is now above 4% in most measures. Meanwhile RBNZ’s governor Orr reiterated their stance that rates need to remain low for a long time, adding that future policy guidance is important. Assistant governor Hawkesby says that their next meeting in February is ‘live’.

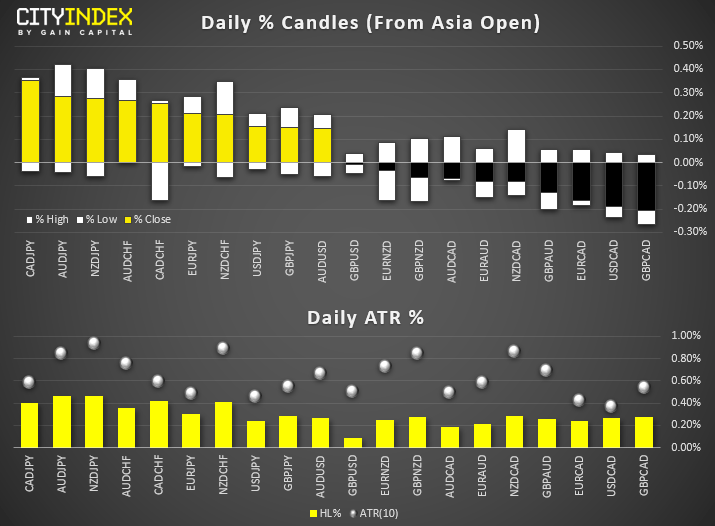

- Commodity currencies (CAD, AUD and NZD) are the strongest majors of the session, JPY and CHF are the weakest. This places carry trades at the top of the leader board for the session, with CAD/JPY, AUD/JPY and NZD/JPY leading the pack. At the other end, GBP/CAD and USD/CAD are the weakest pairs.

- No pairs have met or exceeded their ATR’s today, which leaves potential for moves in the European or US sessions without imminent concerns of over extension.

Equity Brief:

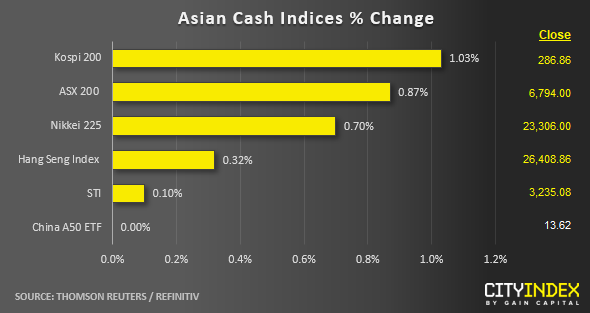

- Key Asian stock markets have started to trade higher as at today’s Asian mid-session with hopes (again) that the U.S-China “Phase One trade deal” sign-off will gain traction soon. White House economic adviser Larry Kudlow has told media after an event at the Council on Foreign Relations that the Phase One deal is downed to the “short strokes”.

- Th best performers so far, South Korea’s Kospi 200, Australia’s ASX 200 and Japan’s Nikkei 225 which have rallied by close to 0.70% to 1.00%.

- The ASX 200 is now eying a 2nd consecutive session of gains led by gold mining related stocks; Dacian Gold and Saracen Mineral which have rallied by 5.1% and 2.7% respectively.

- Cautious trading in Hong Kong stock market as the Hang Send Index has only posted a modest gain of 0.30% where participants are more concerned on the economic fallout from the escalation of the on-going anti-government demonstrations over the coming weekend.

- Singapore’s Strait Times Index (STI) has not jumped onto the trade deal (hope) bandwagon as it is almost trading almost unchanged; dragged down by Singtel which has recorded a decline of -3.30% after it posted a S$668 million loss on provision due to its Indian associate, Bharti Airtel’s claims from the Indian government where the Supreme Court in India has ordered telecom operators to pay the state billions in past dues.

- The S&P 500 E-Mini futures has rallied in Asia session with a gain of 0.34% to print a current intraday high of 3110 (fresh all-time high) after Kudlow’s positive comments on the U.S.-China Phase One trade deal.

Up Next

- US retail sales contracted by -0.3% in September, its first negative print since February. Another negative print today could point towards concerns that weakness from the manufacturing sector is spreading to the wider economy. Keep an eye on USD to see if it retraces further, in line with what price action currently suggests.

Matt Simpson and Kelvin Wong both contributed to this article Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Today 10:37 AM

Today 08:25 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM