View our guide on how to interpret the FX Dashboard

FX Brief:

- China’s manufacturing PMI’s provided a positive start to the week for risk appetite, with IHM Markit read expanding at its fastest rate in nearly 3 years. This follows on from NBS (government related) read on Saturday which expanded for the first time in 7 months.

- Earlier it was reported that China wants tariffs rolled back as part of a phase one trade deal.

- Over the weekend, PBOC’s Governor Yi warned that policy is to remain cautious and that the ‘downturn will stay for a long time’.

- New Zealand’s government announced it plans to increase infrastructure spending on Saturday, a move which should help boost growth into 2020.

- It was a mixed set of data from Australia. ANZ job advertisements fell -1.7% in November, showing less demand from employers and the potential for weaker employment number further out. Building approvals also declined -15.6% YoY, its fastest decline since March 2009. Manufacturing PMI expanded at 51.6 versus 48.1 prior to show the sector back into expansion.

Price Action:

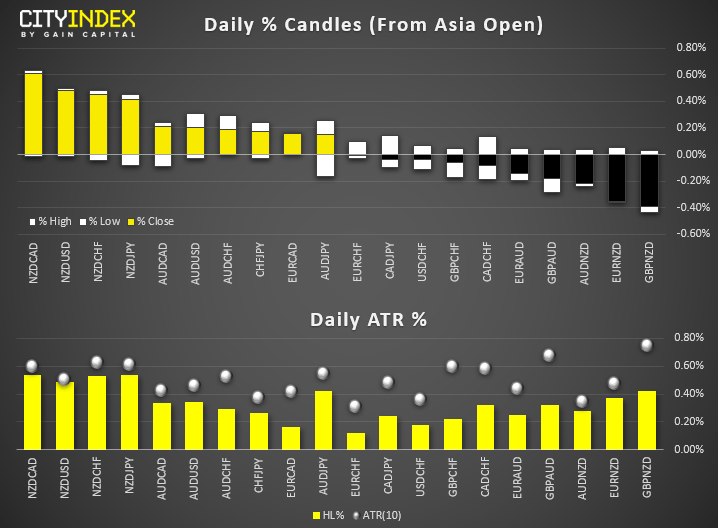

- NZD and AUD are the strongest majors on the back of firmer PMI data from China. JPY is the weakest in a mild risk-on session. Daily ranges for NZD crosses hit 80-95% of their ATR’s whilst pairs outside of NZD are just 35-50% of their ATR’s (so an increased chance of them breaking out of consolidation in the next session/s.)

- DXY printed a bearish key reversal on Friday (bearish outside bar and hammer) to suggest a top is being carved out.

- EUR/USD is back above 1.10 having printed a bullish hammer on Friday. A break above 1.1028 confirms the reversal candle.

- NZD/CAD continues to hold above 0.8500 support and could be heading towards a break to new highs.

Equity Brief:

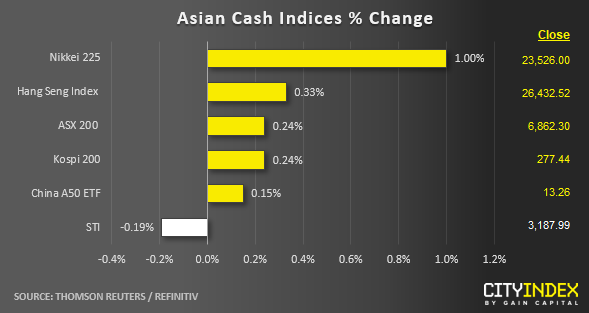

- Key Asian stock indices are showing cautious modest gains so far on the backdrop of a better than expected manufacturing activities in China that has reinforced that the global economy has started to recover. Official NBS China Manufacturing PMI for Nov has came in at 50.2 over the weekend, the first expansionary reading above the 50 level since Apr 2019 coupled with the non-official Caixin Manufacturing PMI that comprises of more small medium enterprises that has also beat consensus forecast to rise to a near 3-year high of 51.8 in Nov; the 3rd consecutive month of steady increases above the 50 level since Aug 2019.

- On U.S-China trade deal related matters, there was a report out from China’s Global Times on Sunday that had cited from unnamed sources that in order for the much touted “Phase One trade deal” to be signed off, China’s stance was a removal of existing tariffs on Chinese goods but U.S. officials had been resisting such demand because the tariffs were their only weapon in the trade war. Time is now running short for a Phase One deal to be agreed between U.S and China before another tranche of U.S tariffs are set to be implemented on Chinese products on 15 Dec.

- After a calm weekend in the previous week, Hong Kong’s anti-government mass demonstrations were back in the street over the weekend where the police clashed with protesters with tear gases fired. There are no signs of demonstrations abating as anti-government protestors have planned a series of lunchtime rallies for the whole of this week.

- Hong Kong Financial Secretary Paul China has warned that Hong Kong is expected to record its first budget deficit since 2004 with the economy sustaining damage to 2% of GDP growth the due to the on-going 6-months of social unrest.

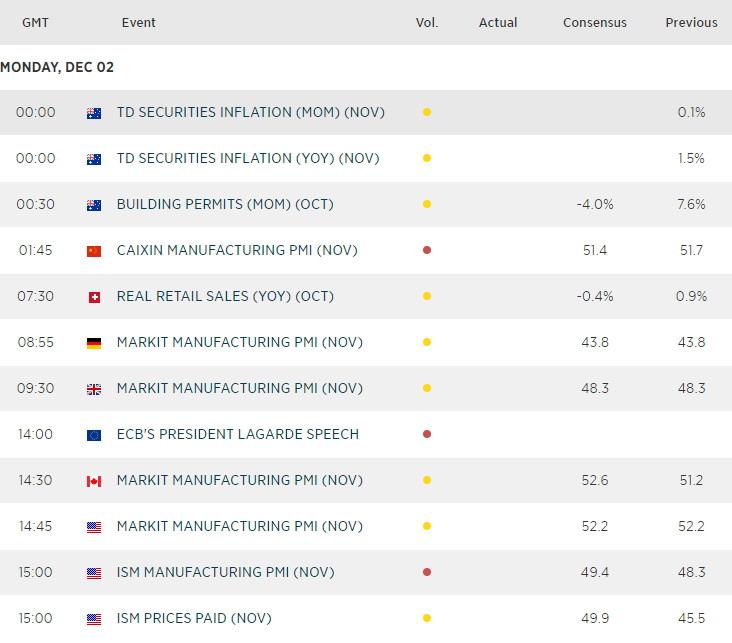

- Hong Kong’s Retail Sales for Oct out later at 0830 GMT where its has recorded a decline of -18.3% y/y in Sep.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM