View our guide on how to interpret the FX Dashboard

FX Brief:

- Hong Kong strongly opposes the passage of the Hong Kong bill by the US house, saying it will not help ease the social unrest.

- The ebb and flow of FX moves were mostly dictated by the HK bill and contrasting reports over how this phase one deal was looking.

- Earlier in the session, Trump said he felt China weren’t stepping up the level he wants for trade talks, seeing JPY broadly strengthen across the board with several pairs testing key levels. Yet concerns were later soothed with Vice Premier Lui saying he was “confident” a deal can be made, with JPY paring earlier gains. The Yuan briefly touched a 3-week low.

- There’s room for further cuts, according to a former PBOC governor. Separately, Premier Li Keqiang vows to keep macro policies stable and use all possible means to lower interest rates. (Basically, more stimulus than you can shake a stick at…)

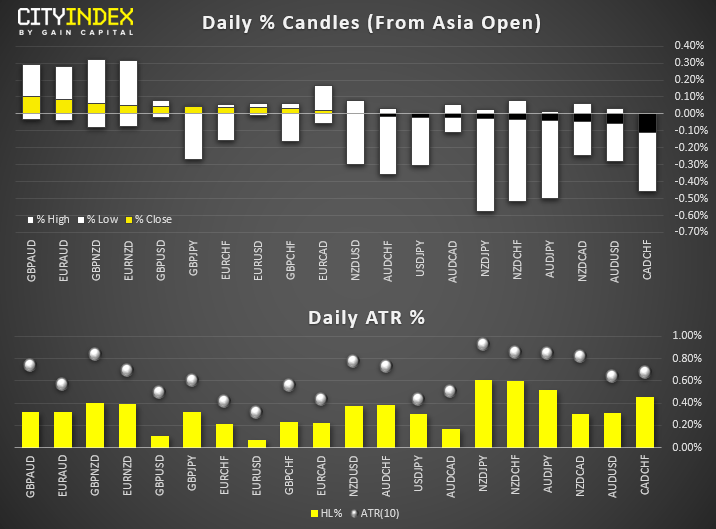

- As for price action, the most notable feature is indecision, with all pairs having formed doji’s or hammers with small bodies. Average range to ATR is around 50%, so this leaves the potential for moves in later sessions without concern of overextension. Although it would be nice if some markets could decide which way they want to go!

Equity Brief:

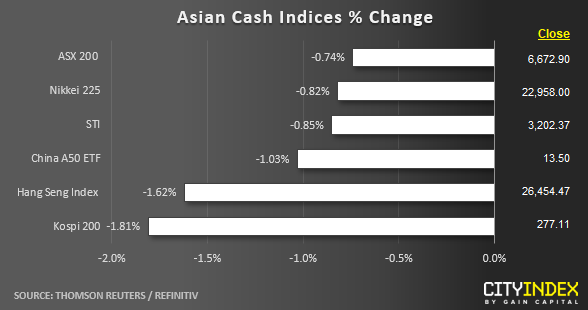

- Key Asian stock markets have continued to drop into a sea of red for the 2nd consecutive session; elements of uncertainty have started to surface in the past few days on the signing off of the much “hyped up” U.S-China Phase One trade deal before 15 Dec. Complications arise through the passing of the Hong Kong Democracy Bill to support anti-government protestors in HK by Congress and U.S President Trump has indicated to sign the bill into legislation as soon as today according to sources. China has indicted displeasure and vowed to “retaliate”.

- After a rally of 2.4% seen on Hong Kong’s Hang Seng Index (HSI) in the earlier part of this week, “reality check “has finally set in where the HSI has recorded a drop of -1.61% as at today’s Asian mid-session that has wiped out all its earlier gains.

- Alibaba has raised about HK$88 billion on its secondary listing in Hong Kong and confirmed its pricing at HK$176 per share for the 500 million new shares, making it the biggest HK listing since 2010. Alibaba’s Hong Kong share is expected to start trading on 26 Nov.

- Singapore’s finalised Q3 GDP rose at a faster pace than its earlier estimation; 0.5% y/y versus a previous projection of 0.1% y/y. The Ministry of Trade & Industry has also indicated an optimistic economic outlook for Singapore next year where 2020 full-year GDP estimate is projected at 0.5%-2.5%, up from 0.5%-1% this year. However, the Singapore’s Straits Times Index (STI) is not “buying” into such optimism at this juncture where it shed -0.8% dragged down by the heavy weightage banking stocks; DBS and OCBC where both dropped by -1.91% and -1.26% respectively.

- Shares of Westpac Banking has continued to face downside pressure; down by -1.95% in light of its breach of anti-money laundering practises and Australian PM Morrison has called on the bank’s board to review Westpac’s CEO position.

- The S&P 500 E-Mini futures has continued to drift lower in today’s Asian session, down by -0.20% to print a 3-day low of 3091.

Up Next:

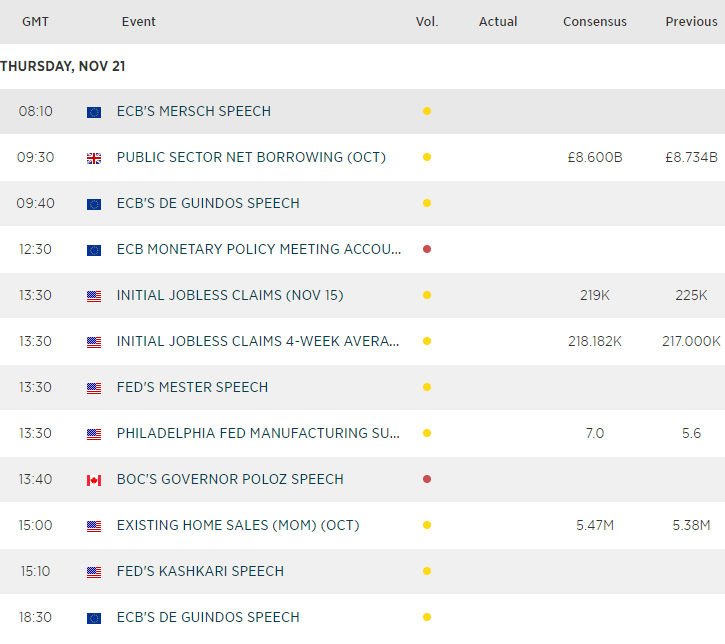

- BOC’s Poloz is to hit the wires, two days after Deputy Governor Wilkins strongly hinted that lower rates and / or QE could be used in the future. If Poloz is to stick with this narrative, we could have a broadly weaker CAD on hour hands, so keep CAD pairs on your radar.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Dollar articles

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM