View our guide on how to interpret the FX Dashboard

FX Brief:

- Markets erupted after news came to light the US had orchestrated a targeted missile attack on Pro-Israeli leaders at an Iraq airport. The attack has been confirmed by the Pentagon, and US Navy Seals also detained several leaders.

- Separately, North Korea’s official newspaper warned of an immediate, powerful strike against threats. This follows on from comments from NK leader Kim Jong-Un in late December that the world will soon witness a “new strategic weapon”.

- Oil and gold spiked higher and remain supported, and the yen is the strongest currency on safe-haven inflows. AUD/JPY and NZD/JPY are the biggest movers to the downside in today’s risk-off environment.

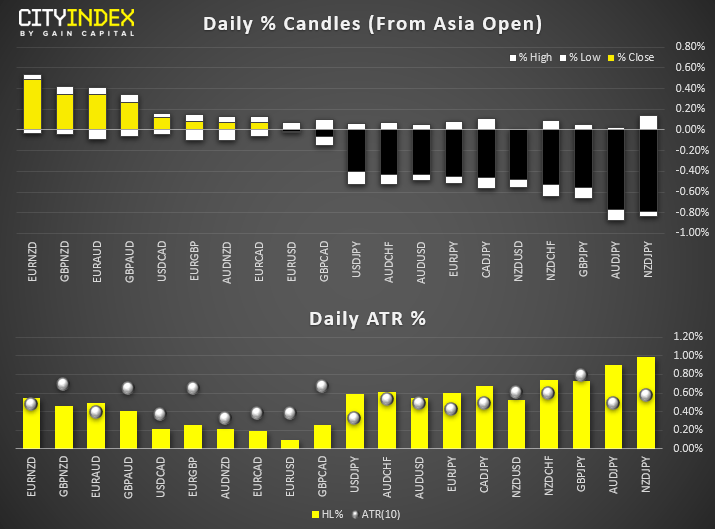

Price Action:

- AUD/NZD and NZD/JPY broke out of compression as outlined yesterday, but clearly not in line with its trend. At 11 and 10-day lows respectively, bears remain in control although both have moved over 150% of their typical daily ranges so be mindful of over-extension.

- USD/JPY fell to a 9-day low and has also reached 180% of its typical daily range. Given today’s low is just above 107.88 support, then there is potential for this level to hold (or even retrace higher) if tensions in the Middle Eastern don’t escalate further.

- AUD/USD has continued to retrace from its highs but has found support near the 38.2% Fibonacci level highlighted yesterday. Ultimately, we’re looking for evidence for support to build above the breakout level around 0.6940, but we’re waiting for volatility to subside before turning bullish on the daily chart.

- USD/CAD continues to coil at the lows but is risk of over-extension to the downside. That said, whilst it remains beneath the 2019 lows (1.3015), we have to consider another leg lower. Whereas a break back above this milestone level warns of a larger rebound. Keep in mind BOC’s Wilkins and FOMC minutes are on tap. And this governor previously gave a dovish speech, before a slew of weak data came out through December – this leaves USD/CAD vulnerable to a rebound if she repeats her dovish remarks.

Equities Brief:

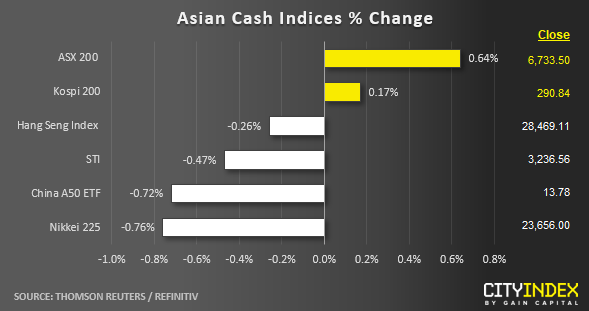

- Most Asian stock markets have started to see a partial reversal of the recent Christmas rallies due to the risk of rising geopolitical tensions in the Middle East.

- Meanwhile, a Reuters news report has indicated that China has planned to keep its inflation target around 3% in 2020, unchanged from last year despite elevated pork prices according to unnamed policy sources. The 2020 inflation target is expected to be unveiled at the annual parliamentary session in Mar and was endorsed by top Chinese leaders at a economic planning conference in Dec 2019.

- Also based on the policy sources, Reuters has reported that China consumer inflation is expected to ease in the second half of 2020 with central bank, PBOC easing polices on track.

Price Acton (derived from CFD indices):

- US SP 500: The Index has wiped out all its earlier Asian session gains after it printed a current intraday fresh all-time high of 3262 which is closed to our key medium-term resistance/target of 3280 as per highlighted in our previous weekly outlook report. Right now, the daily RSI oscillator has formed a bearish divergence signal at its overbought region. At risk of a shaping a multi-week corrective decline towards 3155 support in the first step.

- Japan 225: Bearish break below medium-term ascending channel support from 26 Aug 2019 low. At risk of shaping a further decline to retest 22700 (former range resistance from 08 Nov 2018) with key short-term resistance at 23785.

- Hong Kong 50: Recent Christmas rally has stalled right below a medium-term resistance of 29000 (76.4% Fibonacci retracement of the decline from 04 Jul 2019 high to 15 Aug 2019 low). It printed a current intraday high of 28863 and formed an impending daily “Dark Cloud Cover” bearish candlestick pattern. A break below 28400 may see a further decline towards 28000 next (former 07 Nov 2019 swing high & former major descending resistance from 29 Jan 2018 all-time high).

- Australia 200: After its 3rd failed attempt to break above the major resistance zone of 6880/90 on 16 Dec 2019, the Index has staged a bearish breakdown below its ascending support in place since 23 Dec 2018 low. Today, it has retreated right at its 6790 pull-back resistance of the aforementioned ascending support. Further potential downside to retest the 6600 minor support in the first step.

- Germany 30: Current slide in price action is still holding above the 13100 support (medium-term ascending channel support from 15 Aug 2019 low & former swing high areas of 22 May/14 Jun 2018) but upside momentum has started to wane as seen from the impending bearish divergence in the daily RSI oscillator since 07 Nov 2019. Low conviction now for a further push up to target 13600/750 and a break below 13090 opens up scope for a potential corrective decline towards the 12600/500 support (former swing high area of 03/25 Jul 2019).

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM