- It’s been reported that the Dutch government have been in talks with 325 UK-based companies who are considering relocating to the Netherlands post-Brexit.

- China’s Vice Premier Liu He says China are willing to resolve its trade dispute with the US via “calm” negotiations. This is after Trump announced fresh retaliatory tariffs on China late Friday and “hearby ordered” US companies to leave China.

- FX markets saw a few U-turns, initially kicking off the week in risk-off mode but fears subsided after comments from Liu He.

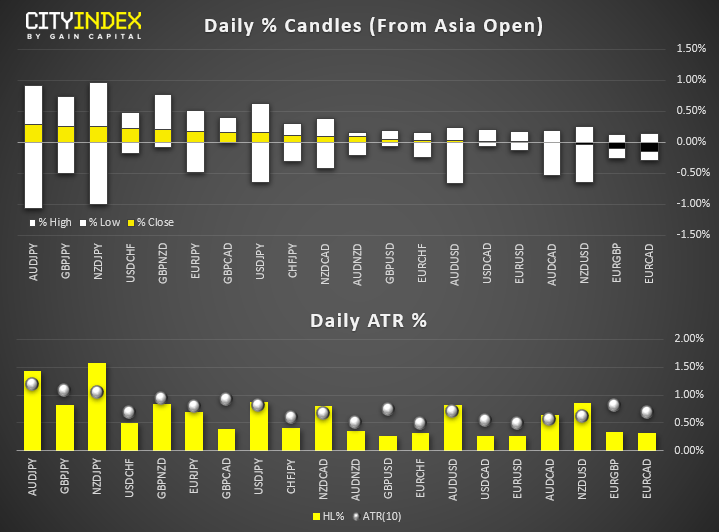

- USD/JPY it its lowest level since October 2017 but has since closed its gap. AUD/USD fell to a 13-session low but has since recovered losses and trades marginally higher for the day. NZD/USD also came under pressure before its U-turn, with today’s intraday low hitting its lowest level since October 2015.

- USD/CNH gapped to a fresh 11-year high as it plays catch-up with the onshore CNY, in response to the escalating tensions with the trade war.

- US10Y yielded its lowest rate over 3-years, currently trading at 1.46%.

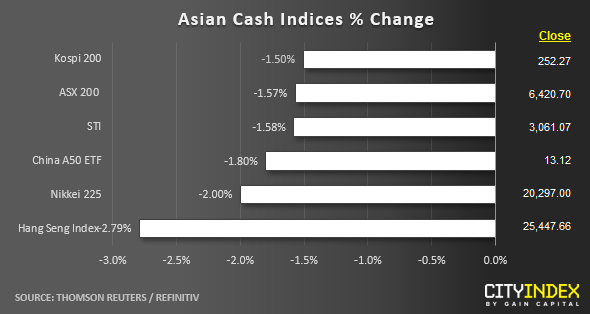

- Ahead of the European session open, Asian stock markets have plunged into the red in line with last Fri’s 23 Aug weak performances seen in the key benchmark U.S. stock indices; S&P 500 – 2.59%, Nasdaq 100 – 3.15% reinforced by U.S. President Trump latest’s tariffs increase on China’s products after China has proposed to retaliate on additional tariffs on US$75 billion of U.S. goods, including soybeans, automobiles and oil.

- The worst performer as today’s Asia mid-session is the Hong Kong’s Hang Seng Index (down -2.79%) where localised factor added to the woes. Yesterday’s anti-government protest rally has seen an escalation of violence between police and protesters after the prior week’s peaceful rallies. The on-going three months of protests have dampened consumer and business sentiment where Hong Kong now faces the risk of the technical recession in Q3.

- Earlier comments today from China Vice Premier Liu He, a key negotiator in U.S/China trade talks have managed to “smooth’ some selling pressure as he said the China is willing to resolve the trade dispute through dialogues with a calm attitude.

- However, caution shall be warranted on the bounces seen so far in Asian stocks as the USD/CNH (offshore yuan) has broken above the previous medium-term high of 7.1400 and managed to hold firm above 7.1400 so far.

- The S&P 500 E-min futures has staged a gapped down in at the Asian open session where it has declined by -1.45% to print a current intraday low of 2810. As at today’s Asian mid-session, it has managed to retrace slightly from its intraday low with a loss of -0.86% at this juncture.

Up Next:

- The G7 talks will be concluded and its been reported that Trump will accompany Macron to meet the press today.

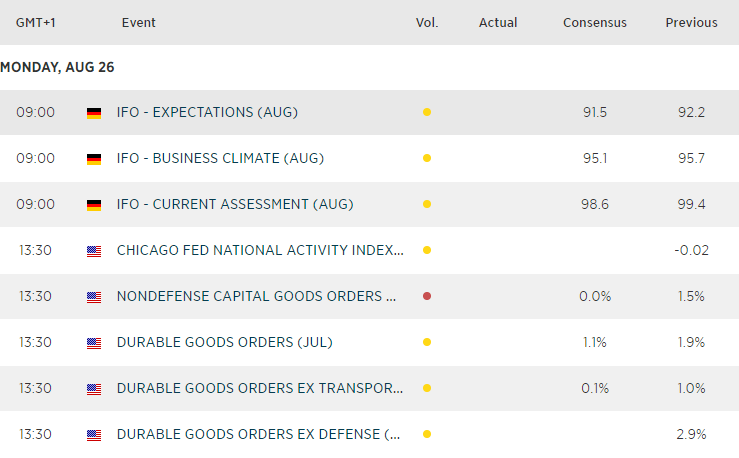

- German IFO is of interest as they continue to point towards a recession, which places Euro crosses and the Dax into focus for traders. You can take a closer look at the bearish charts from the week ahead post, but expectations are for the reads to deteriorate further which leaves potential for a bounce on the Euro if they surprise to the upside.

Latest market news

Yesterday 08:33 AM

Latest Dollar articles

Yesterday 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM