Stock market snapshot as of [27/9/2019 10:19 AM]

- European markets have found sufficient reasons to put aside U.S. political tremors, trade and Brexit uncertainty in favour of moderate gains at the end of a shaky week. It’s a flicker of optimism about global industrial demand, including from key resource consumer China, even after a week in which peripheral trade war-linked developments cast uncertainty about the scope of U.S.-China talks that are set to continue next month

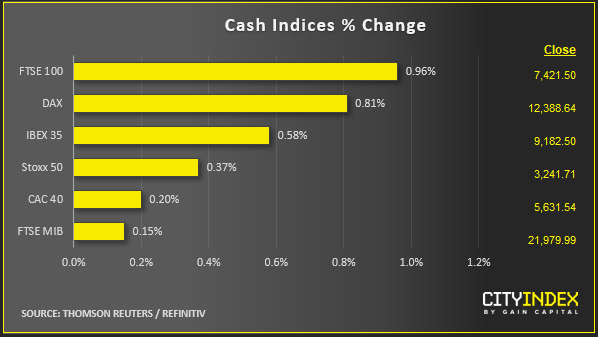

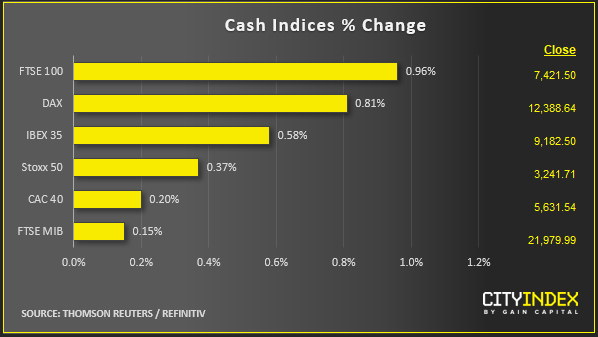

- The upswing has particularly favoured the FTSE 100, home to some of the largest miners in the world, amid signs that one of Europe’s biggest laggard markets this year could soon catch up and even break to a new cycle

- U.S. stock index futures got in to the same spirit half-way through Europe’s session, shrugging off, for now, the increasing probability of Washington disruption. President Donald Trump has come out swinging against damaging allegations from a whistle-blower, who Trump accused of being close to a spy. White House moves to lock down call logs after apparent leaks only heightened the growing sense of crisis. With the S&P 500 closing lower in four out of the last five sessions it’s tough to dismiss the notion that investors are rattled. Just how rattled markets are should become more evident in coming weeks as the impeachment process gathers pace

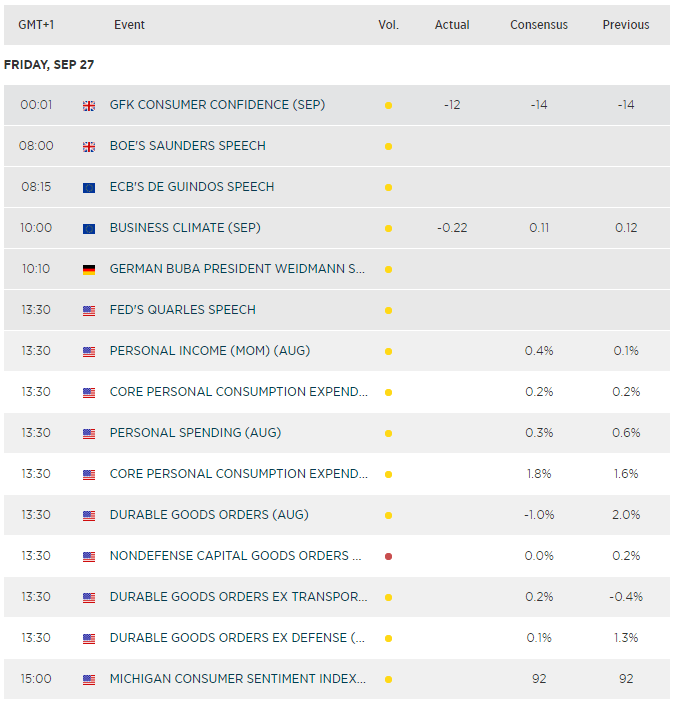

- Stock investors are also side-lining the latest pessimistic assessments about Europe’s economy, in the shape of a European Commission survey on Economic Confidence. Industry and consumer components extended declines in September, whilst Services barely rose. The commission said industry managers had become “markedly more pessimistic”. The euro bore the brunt, getting pinned near post-ECB rate cut lows. The EC prints combine with worse than forecast inflation, also out earlier, to bake in accommodative monetary policy, probably well into 2020

- Underlying U.S. inflation data, codified as Personal Consumption Expenditure gauges were largely in-line with forecasts, rounding out a snapshot of developed-economy price growth that was lacklustre, including CPI releases out earlier from Japan

Stocks/sectors on the move

- ArcelorMittal and ThyssenKrupp are among the mining, metal and chemical groups out in front, followed by general retailers that lift consumer discretionary segments, with heavyweight help from Europe’s car industry, as Daimler, VW and BMW lead all large Continental auto shares higher. Rises by virtually every high-profile European bank stock, led by HSBC confirms the mood is enjoying a spell of risk taking

- Reports that Saudi Arabia may have agreed a partial ceasefire in its proxy Yemen conflict are even being shrugged off by oil prices and hence a boon to integrated petroleum producers’ shares, including Shell, BP and Repsol

- Heavyweight stocks to watch when Wall Street opens include Micron, which looks set to slide 5% looking pre-opening dealing after the group’s gross margin missed estimates and its profit outlook also disappointed. Likewise, the U.S. semiconductor sector could be pressured for a consecutive session

- Peloton shares should also be in focus, partly out of interest in the numerous further techy ‘unicorns’ waiting in the wings with IPOs. The exercise bike and fitness services group spun sharply lower in its debut session on Thursday

FX snapshot as of [27/9/2019 1:17 PM]

FX markets

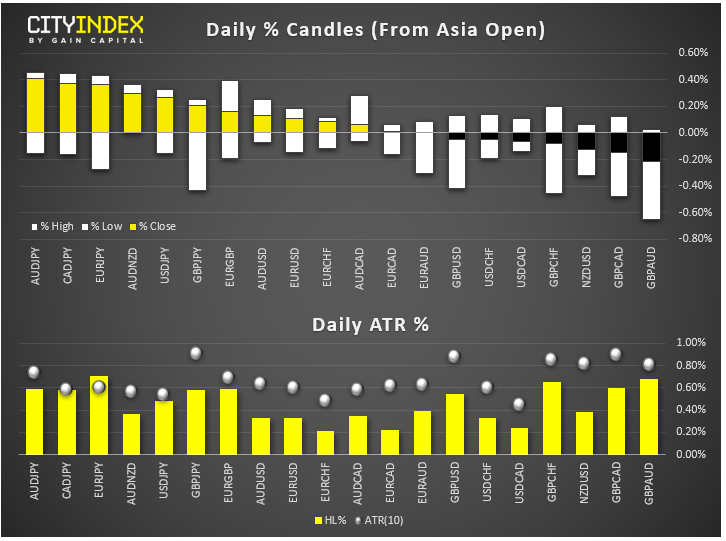

- Despite horrible European growth indications, the pound is out-slumping the euro after the Bank of England’s chief economist moved to remove any remaining doubt that deal or no deal, Brexit (or even just the threat of Brexit) an interest rate cut may still be required. Michael Saunders said uncertainty shouldn’t be a “recipe for policy inertia,” and officials would need to be nimble. The pound is under pressure vs. higher-yielding Aussie and Canadian dollar, and against negative-yielding franc

- A Belfast court decision in favour of Prime Minister Boris Johnson in a case over the impact of a no-deal Brexit on the Good Friday peace accord for Northern Ireland, looks less material for the pound. This week’s Supreme Court ruling against Johnson’s Parliament suspension will supersede most remaining Brexit litigation against the government fairly moot

- Euro weakness remains significant despite the EUR/USD rate’s uptick from its lowest since 12th May. City Index and FOREX.com Senior Technical Analyst Fawad Razaqzada notes the pair is again testing a key low seen in the wake of the ECB’s decision to cut rates earlier this month, around $1.0925. Failure to pull sharply higher here would increase the euro’s negative bias with added resistance

Upcoming economic highlights

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Euro articles

April 2, 2024 03:02 PM

February 15, 2024 07:29 PM

January 4, 2024 07:14 PM

December 20, 2023 07:17 PM