FX Brief:

- China’s GDP hit a fresh multi-decade low, expanding ‘just’ 6% YoY and below expectations of 6.1% (down form 6.2% prior). Taking the edge off-of weak growth, industrial output expanded at 5.8%, above 5% consensus whilst retail sales also beat at 7.8% YoY versus 7.5% forecast. So, whilst growth was a disappointment, the rest average it out, hence the muted market reaction from the likes of AUD and NZD.

- RBA’s Governor Philip Lowe thinks that negative rates are “extraordinarily unlikely” and that low rates along are not likely to stimulate investment. “In my view we’re clearly in the world of diminishing returns to monetary easing…" which could be taken to mean RBA will favour QE of negative rates.

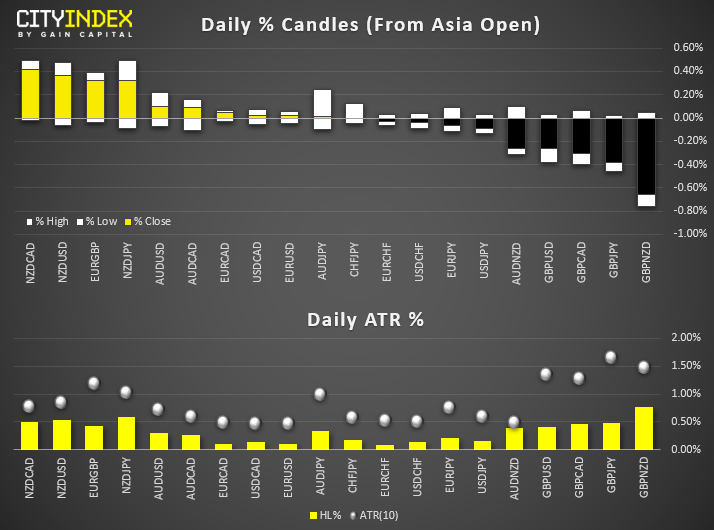

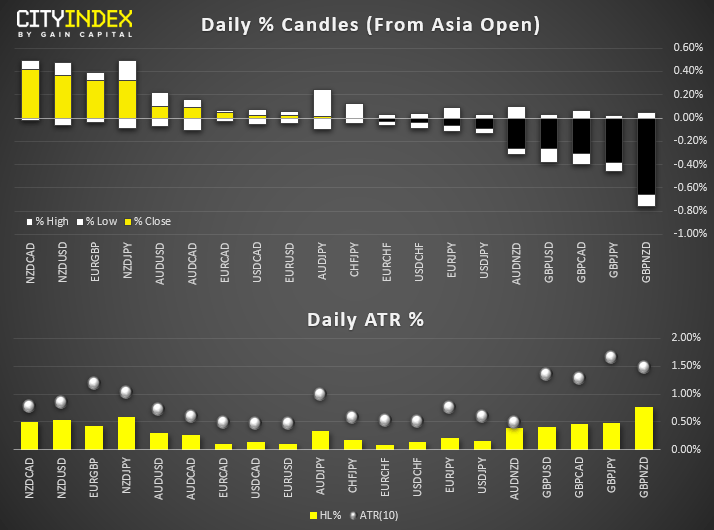

- Razor-thin ranges for the majors. USD/JPY is consolidating in a small range above the pivotal level if 108.50. EUR/USD is brimming at its highs after closing above 1.1100 yesterday. GBP/USD is treading water around 1.2850. NZD I the strongest major (as seen with it dominating strength on the FX dashboard). GBP/NZD has fallen -0.8% but, given high levels of volatility it has pushed the ATR up, hence it ‘only’ covering 50% of its ATR.

- AUD/NZD is the only pair to be near its ATR and, with little news flow expected to directly impact the cross, the move could be done for the day and could be prone to mean reversion.

Equity Brief:

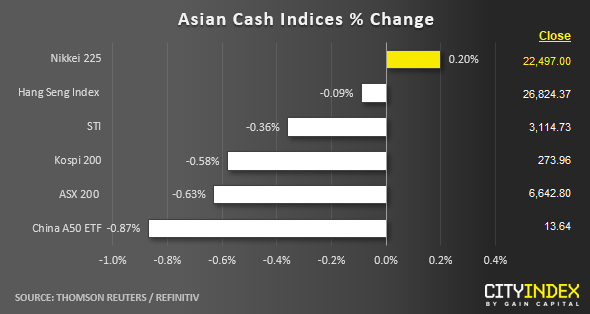

- Some profit-taking activities can be seen in several Asian stock markets in today’s Asian session on the backdrop of mixed economic data from China. China Q3 GDP growth has slowed to 6.0% y/y (below consensus of 6.1% y/y), its lowest growth rate since Q1 1992 while Industrial Production has managed to beat expectations with a growth rate at 5.8% y/y in Sep (5.0% y/y consensus).

- Despite EU and U.K has agreed to a Brexit deal and the ball now is back in U.K for a parliamentary vote schedule this Sat. Thus, some unwinding of “risk on “positions can be justified as we head into the weekend with the possibility that U.K PM Boris Johnson may not be able gather enough votes in the parliament as the Northern Ireland DUP, which the government relies on for support in key votes has reiterated no support on the latest deal.

- The ASX 200 has continued to decline for the 2nd consecutive day where it has shed -0.63% led by major healthcare related stocks that have offshore operations where revenue can be dented due to a weaker USD seen in the past week. Share prices of CSL and Cochlear have declined by -1.1% and -0.8% respectively.

- Japan’s Nikkei 225 has managed to inch out a modest gain of 0.20% led by several major technology stocks reinforced by upbeat earnings from Taiwan’s TSMC, the world’s largest contract chipmaker. Murata Manufacturing, Fanuc and Keyence have recorded gains between 1.3% to 2.4%.

Up Next

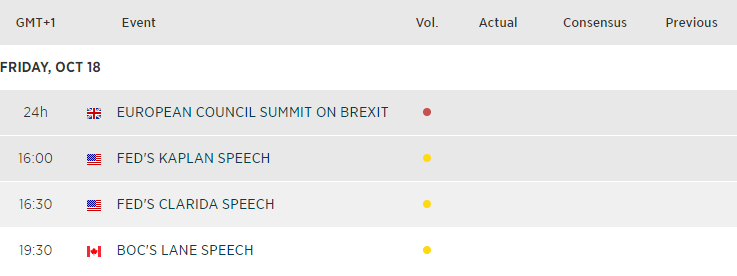

- No major economic data points today, so it’s all about Brexit as we head towards the weekend.

Related Analysis:

Volatility Assessment Ahead Of Brexit Deal Vote | GBP/USD, GBP/JPY, EUR/GBP

Market Brief: BoJo’s Brexit Breaks Through the EU

GBP/JPY on watch as focus turns to parliament Brexit vote

Markets rejoice! Brexit deal now faces the fire

Matt Simpson and Kelvin Wong both contributed to this article

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Yesterday 08:33 AM

Latest Dollar articles

Yesterday 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM