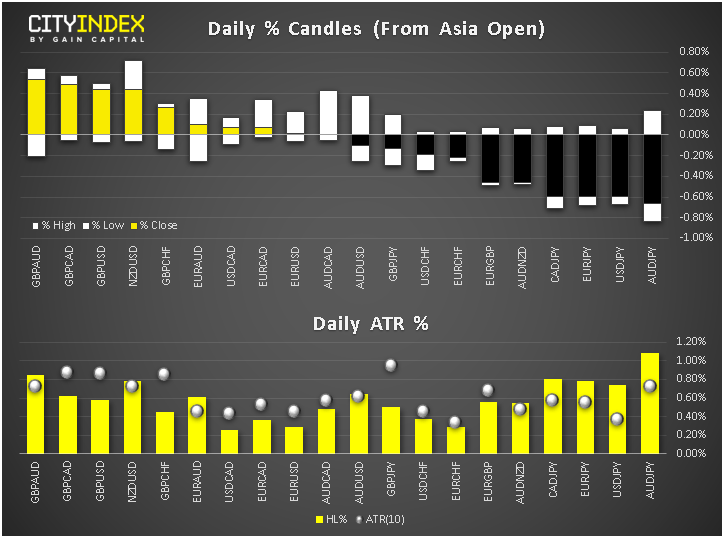

- At midday in London, the GBP and JPY were among the strongest while the AUD and USD were among the weakest.

View our guide on how to interpret the FX Dashboard

- The US dollar continued to sell-off following the Fed’s rate cut last night. Although the central bank signalled a pause in the cutting cycle, Chairman Jay Powell suggested the Fed is nowhere near hiking: “We've just touched 2% core inflation to pick one measure, and then we've fallen back. So I think we would need to see a really significant move up in inflation that's persistent before we would even consider raising rates to address inflation concerns."

- Bank of Japan decided to keep monetary policy unchanged and the yen strengthened as some had expected it to ease policy. But Governor Kuroda said Japan had more room than Europe to lower the already negative interest rates if it needed to.

- China’s manufacturing sector shrank for the sixth successive month in October, according to the latest PMI figures. Activity slowed down on weaker output and new orders, suggesting lingering challenges as growth in the world’s second-largest economy slowed to a 30-year low in the third quarter. The PMI dropped to 49.3 from 49.8 below 49.8 expected. What’s more, the Non-manufacturing PMI also tumbled sharply to 52.8 from 53.6 previously.

- Hong Kong’s economy plunged into a recession after months of violent protests took its toll on growth.

- Eurozone data was mixed: third quarter GDP came in at +0.2% vs. +0.1% q/q expected, but on a year-over-year basis GDP was in line at 1.1%, down from 1.2% previously. Eurozone CPI printed +0.7% in October as expected, down from +0.9% previously, but core CPI was a touch higher at +1.1% vs. 1.0% expected and last. German Retail Sales rose just 0.1% m/m vs. 0.3% expected.

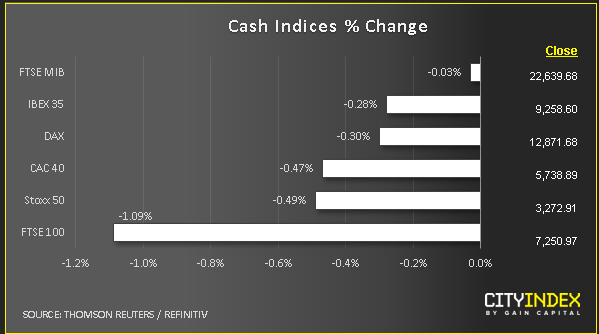

- Stocks fell sharply in Europe this morning despite the S&P 500 rallying to a new record yesterday. Sentiment was hurt here by generally weaker European earnings, news of a recession in Hong Kong, soft Chinese data and as fresh doubts emerged over a long-term US-China trade, according to a Bloomberg report. However, the major indices were at or near key support levels. Could they rebound?

- Among commodities, Gold rallied as it was supported by the weakness in stocks and the US dollar, while crude oil continued to slide amid ongoing concerns over weaker demand.

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Forex articles

Today 04:00 PM

Yesterday 11:30 AM