View our guide on how to interpret the FX Dashboard

FX Brief:

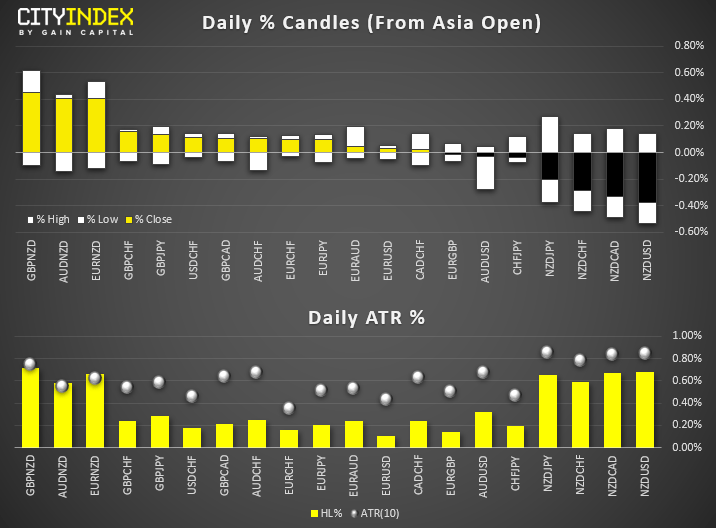

- New Zealand’s 2-year inflation expectations fell to 1.8%, its lowest level since Q4 2016 whilst the 1-year is now just 1.6%. Coming just one day ahead of tomorrow’s RBNZ meeting, expectations for a cut have risen from 72% this morning to around 85%, weighing broadly on NZD.

- Kiwi crosses accounted for the baulk of today’s volatility, with EUR/NZD and AUD/NZD daily ranges exceeding their 10-day ATR’s. Outside of NZD pairs, the average daily range relative to ATR is just 40%. NZD/JPY and NZD/USD are just above key support levels ahead of tomorrow’s RBNZ meeting.

- Business confidence in Australia rose from its lows today according to a survey from NZB. Whilst it’s still at relatively low level, it could suggest the slump in confidence has troughed.

- French PM Emmanuel Macon says he had “an excellent conversation” on the phone with President Trump.

- Reports have surfaced that Trump plans to delay auto tariffs on the EU for 6 months.

Equity Brief:

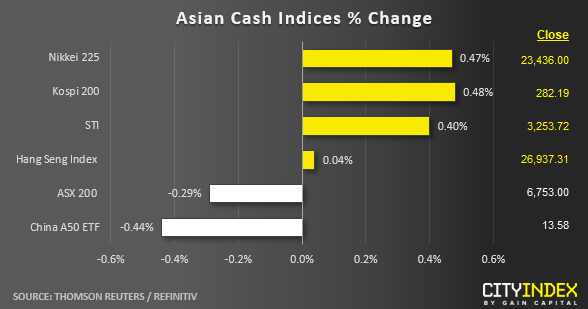

- Key Asian stock markets are trading in a mix fashion as traders continue to monitor the political situation in Hong Kong and U.S. President Trump’s speech later at The Economic Club of New York for any hints that offers clarity on the outstanding issues regarding U.S-China trade talks.

- Today’s worst performers are Australia’s ASX 200 and the China A50 ETF where both shed about -0.4%. The ASX 200 has given up almost half of its gains recorded yesterday.

- Singapore’s Straits Times Index (STI), South Korea’s Kospi 200 and Japan’s Nikkei 225 are leading the pack with gains at around 0.40%. Today’s gain seen in the STI came after it has posted an accumulated loss of -1.4% in the past two sessions. Golden Agri-Resources, Singapore Technologies Engineering and Mapletree Commercial Trust are the top component stocks gainers so far; upped 6.52%, 2.75% and 2.27% respectively.

- The situation in Hong Kong remains tense with on-going stand offs between anti-government protesters and the police that have led to territory-wide disruptions this morning. Media has reported that protesters have urged people to gather in the Central business district, Hong Kong financial hub and Tsim Sha Tsui, a popular tourism and shopping area at noon today that can cause more disruptions towards economic activities.

Up Next:

- Germany’s ZEW economic index is expected to be less pessimistic at -13 versus -23 prior.

- U.S. President Trump speech at The Economic Club of New York where a White House spokesman has indicated Trump will focus his speech on how U.S. tax and trade policies have supported a strong economy. Any impromptu remarks on the progress of U.S.-China trade talks may trigger a significant movement in the financial markets.

- Several Fed members (Clarida, Harker and Kashkari) are also due to speak, so keep an eye on USD pairs and gold for any policy clues.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Latest Dollar articles

Yesterday 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM