FX & Stock market snapshots as of [16/08/2019 0600 GMT]

- In today’s Asian session, the risk sensitive AUD/USD has continued to firm up within a sideways trading range in place since 08 Aug 2019. 0.6820 remains the range resistance to keep an eye on.

- The AUD/USD is being bided up in anticipation of fresh stimulus injection from China. The National Development and Reform Commission has made an announcement today that it will roll out a plan (no details yet) to boast China’s disposable income later in 2019 and 2020.

- The EUR/USD remains under pressure as it inches down lower towards the 01 Aug 2019 swing low of 1.1027. Current weakness is being supported by a dovish media interview yesterday from ECB official, Rehn that has mentioned a “significant and impactful” stimulus package is required in the upcoming ECB meeting in Sep.

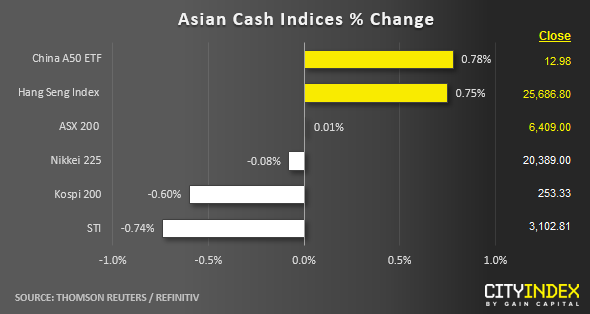

- Mix bag is the theme today for Asian stock markets. The Singapore’s STI and South Korea’s Kospi 200 have remained in the red as at today’s Asian mid-session.

- Rising tension between North and South Korea has reinforced the underperformance seen in the Kospi 200. North Korea has launched two projectiles into the Sea of Japan after Pyongyang described South Korea’s president as “imprudent” and vowed to terminate inter-Korean talks.

- China and Hong Kong stock markets shine in anticipation of fresh stimulus plans announced by China’s state planning agency to boost domestic spending.

- However, economic uncertain remains intact in Hong Kong hampered by domestic unrest. The City braces herself for more protests over this weekend after the police has rejected a protest march to be held this Sunday organised by a major NGO, The Civil Human Rights Front.

- The S&P 500 E-mini futures has inched up higher by 0.45% as seen in today’s Asian session to print a current intraday high of 2864. Interestingly, it is now hovering below a minor range resistance of 2872.

Up Next

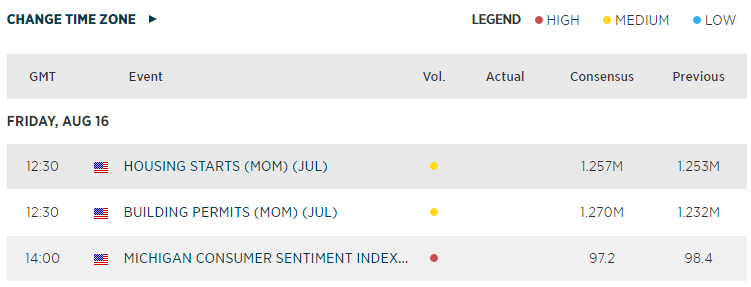

- U.S. Housing Starts for Jul out at 1230 GMT (1.270M consensus versus 1.232M in Jun)

- U.S. Michigan Consumer Sentiment Index (97.2 consensus versus 98.4 previous).

Macroeconomic Calendar

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Latest Forex articles

Yesterday 11:09 PM

Yesterday 04:00 PM

Yesterday 04:19 AM

April 22, 2024 04:33 PM