- The US officially blamed Iran for this weekend’s attack on the world’s largest oil facility in Saudi Arabia. Trump tweeted that the US was “locked and loaded”, hinting at a potential response over the attack. Oil prices are back below $60 after gapping higher over 12% today.

- China data came in weaker than expected, with urban investments slowing to 5.5% YoY (weakest in 12 months), industrial output falling to 4.4% (weakest since 2002) and retail sales felling to 7.5% versus 7.9% expected. This is all despite further stimulus earlier this year, which will no doubt spur further calls for yet more stimulus.

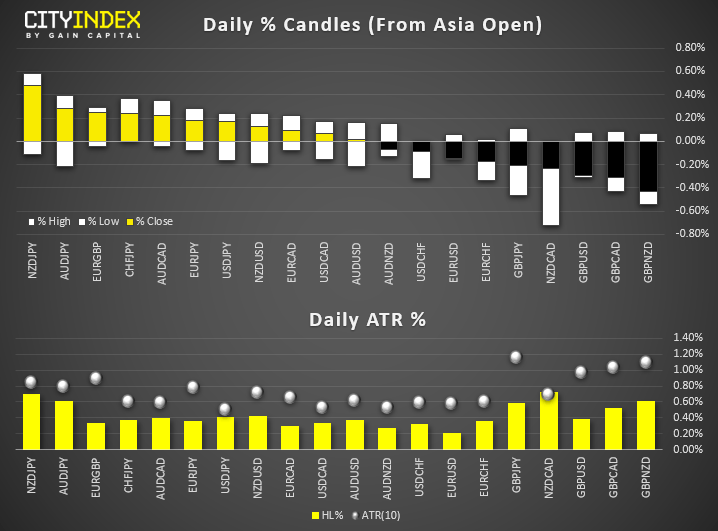

- CAD is the strongest major, supported by higher oil prices. JPY is the second strongest major from safe-haven flows, seeing USD/JPY gap to a 2-day low and trade back beneath April’s bearish trendline. GBP is today’s weakest major, although remains near Friday’s highs.

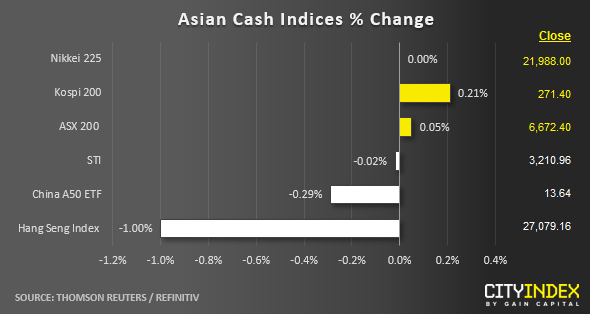

- Despite the weekend drones’ attack on Saud Arabia’s oil production that has sent the WTI crude oil futures to spike close to 10% in today’s Asian session, the overall performance seen so far on Asian stock markets have appeared to be quite muted despite an increase in Middle East’s geopolitical risk. U.S. has put the blame on Iran for the attacks and President Trump tweeted with a “lock and loaded” response that hinted a potential retaliation towards Iran.

- Also, industrial production from China for Aug came in below expectation at 4.4% y/y versus consensus of 5.2% y/y. It has continued to decline from Jul data of 4.8% y/y that has led to a 3rd consecutive month of slower growth from the negative effects of the on-going U.S-China trade tension.

- The worst performer so far as at today’s Asia mid-session is Hong Kong’s Hang Seng Index where it has dropped by -1.00%. The weaker sentiment seen in the Hang Seng Index versus its Asian peers is likely due to localised factors. Firstly, the negative spill-over effect from another bout of violent weekend clashes between police and anti-government protestors where mass protests have entered the 15th week. Secondly, London Stock Exchange (LSE) has rejected Hong Kong Stock Exchange (HKSE) US$39 billion takeover bid. Despite HKSE’s refusal to give up on its bid for LSE, shares of HKSE has dropped by -2.7% to hit a 4-week low of 234.40 as seen today.

- S&P 500 E-mini has gapped down in today’s Asian open session and traded lower to print a current intraday low of 2983; a drop of -0.86%. Right now, as at today’s Asian mid-session, it has recouped some of its earlier losses to trade at 2990; a current intraday drop of -0.61%.

Up Next:

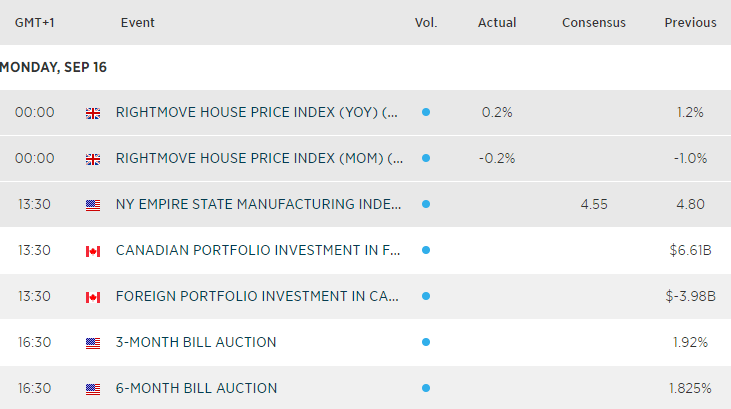

- Data is light for the US session (and non-existent for the European). And with trade tensions taking a back seat, it’s any update or knock-on effect from the weekends oil plant attack which could be a key driver for markets. Markets to watch: WTI, Brent, CAD, NOK, RUB

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Dollar articles

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM