- China vowed to retaliate after the US House voted to pass a human rights bills, which effectively provides support to pro-democracy protesters in Hong Kong. Risk came off a little with E-mini futures dropping slightly and JPY gaining inflows, making it today’s strongest major. Although we’ll need to see if the senate passes the bill for it to have any meaningful impact.

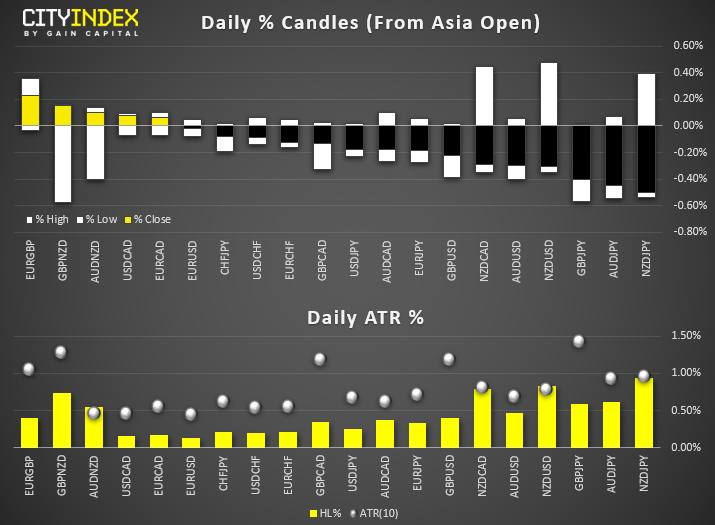

New Zealand CPI slowed to 1.5% YoY from 1.7% prior, yet shortly after RBNZ said their own measure of CPI remained at 1.7%. Still, RBNZ suggested further cuts may be needed and that they continue to undertake prep work on ‘less conventional’ (QE) tools should they be required. NZD and AUD are currently the weakest majors on the session, which are also being weighed down by the pro-democratic bill voted by the US House of Representatives. - The British pound wavered as doubts again grew whether a Brexit deal could be reached, seeing GBP retrace a tad after its best 4-day rally since 2016. With yen taking inflows, GBP/JPY was the third biggest mover, whilst NZD/JPY was the only pair to reach its typical daily range and is today’s biggest mover (so perhaps the move is overdone?)

Equity Brief:

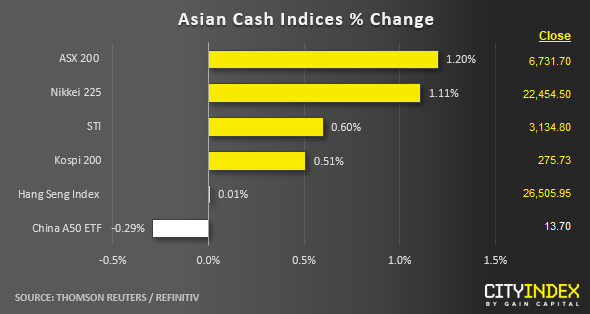

- Most Asian stock markets have continued to solidify their gains since the start of the week taking the cue from the U.S. stock market where both the S&P 500 and Nasdaq 100 have rallied by 1.00% and 1.28% respectively on the backdrop of Q3 earnings optimism.

- China and Hong Kong’s stock markets do not manage to sail along the “bullish wave”. The political situation in Hong Kong has become the latest flash point between U.S. and China on top of an on-going trade war. The U.S. House of Representatives has just passed a bill that offer support to pro-democracy protestors in Hong Kong. A similar bill is now in front of the Senate (the upper house of the U.S. Congress) for voting. China has threatened to retaliate if U.S. Congress passes the bill that can complicate the on-going negotiation talks to put “Phase 1 of the U.S.-China trade deal” in writing.

- The Japan stock market has continued to shine where the Nikkei 225 is upped by 1.19% for a second consecutive session. It also rallied to a 10-month high at 22615 led by semiconductor related stocks reinforced by the positive sentiment seen in the U.S. Philadelphia Semiconductor Index that has surged to a fresh all-time high in terms of closing level yesterday. Tokyo Electron and Advantest have outpaced the Nikkei 225 with gains of 1.8% and 3.7% respectively.

- The S&P 500 E-Mini futures have continued to pull-back in today’s Asian session after a test on the 3000 psychological level in yesterday U.S. session. It has dropped by -0.30% to print a current intraday low of 2986.

Up Next

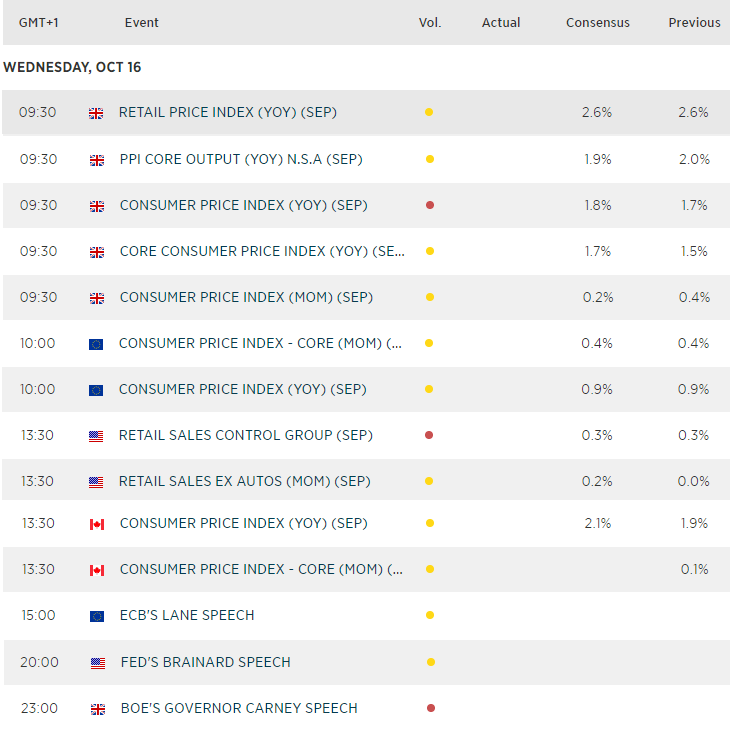

- UK inflation, producer and retail prices make up the baulk of UK data, with prices mostly being expected to soften. Still, it’s more likely Brexit headlines which could make a material impact on GBP crosses over the next couple of days.

- US retail sales provides a feel for consumer spending, which is expected to rise 0.2% from 0% prior.

Matt Simpson and Kelvin Wong both contributed to this article

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM