View our guide on how to interpret the FX Dashboard

FX Brief:

- Risk appetite took a bump early on when President Trump signed the Hong Kong Bill. Whilst they vowed to retaliate, that their Foreign Minister said they’ll take firm counter measure IF the US continues in this way suggests the signed bill may not be detrimental to trade negotiations after all.

- Weaker than expected Australian capex data weighed on the Aussie, seeing it print a 30-session low. With expenditures lower, it’s another headwind for growth and undermines hopes of its recent recovery seen in previous quarters.

- Japanese retail sales slumped at their fastest pace in 4.5 years, in response to the new sales tax hike. It comes as no major surprise given retailers rushed out these past two months to beat the hike and repeat a pattern seen in 2014 when they last hiked sales tax.

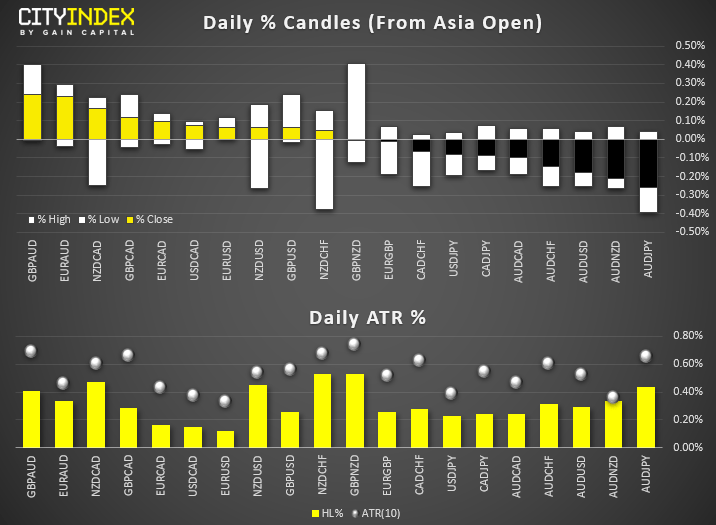

Price Action:

- DXY: continues to respect 98.45 resistance and printed a bearish pinbar on the daily chart at this key level yesterday. Due to thanksgiving today and quiet calendar tomorrow, there’s potential for more consolidation before it either rolls over or beaks higher.

- USD/JPY closed to a 6-month high yesterday and invalidated the bearish wedge pattern we’d been monitoring. Given how well it held up when Trump signed the HK bill, further upside appears favourable from here.

- NZD/JPY is one to watch for a break above 70.30. We think NZD remain oversold relative to RBNZ’s expectations and data overall continues to be positive for the Kiwi. Any signs of positive trade talk could help bolster this view.

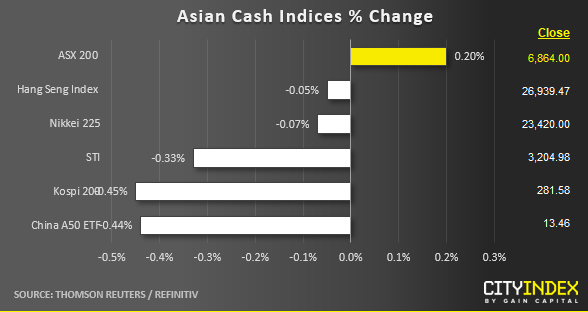

Equity Brief:

- Key U.S. stock benchmark stock indices; S&P 500, Nasdaq 100 and Dow Jones Industrials have surged to another fresh record highs for the 3rd consecutive session overnight ahead of the Thanksgiving holiday today in the U.S.

- However, Asian stock markets are not in a jubilant mood today after U.S. President Trump has signed the controversial Hong Kong Human Rights and Democracy Act Bill today (early Asian hours) that may put the U.S-China Phase One trade deal in jeopardy. Time is ticking for both sides to conclude the deal before the next tranche of U.S. tariff is scheduled for 15 Dec.

- China’s foreign ministry has reiterated her displeasure and commented that U.S. backing the anti-government protestors in Hong Kong was a serious interference in Chinese affairs and U.S. efforts were doomed to fail. Also, China has warned of “firm counter measures” without stating any details.

- Most of the key Asian stock indices are showing modest losses of between -0.40% to -0.05% except for Australia’s ASX 200 that has gained by 0.17%. Therefore, movement for next 48 hours is likely to be highly reactive towards potential “tic for tac” related headlines over trade deal and Hong Kong.

- Japan’s retail sales for Oct has tumbled by the fastest pace in more than 4 years to -7.1% versus consensus forecast of -4.4% y/y due to the recent impose national sales tax hike to 10% from 8% on 01 Oct.

- The S&P 500 E-Min futures has shed by -0.28% to print a current intraday low of 3142 in today’s Asian session that has almost wiped out yesterday’s U.S. session intraday gain.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Today 08:15 AM

Latest Dollar articles

Yesterday 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM