Market Brief: Another Round of Records as Focus Shifts to NFP

View our guide on how to interpret the FX Dashboard.

- Investors shrugged off reports of rockets strikes near an Iraqi Air Force base to bid up risk assets for the second straight day.

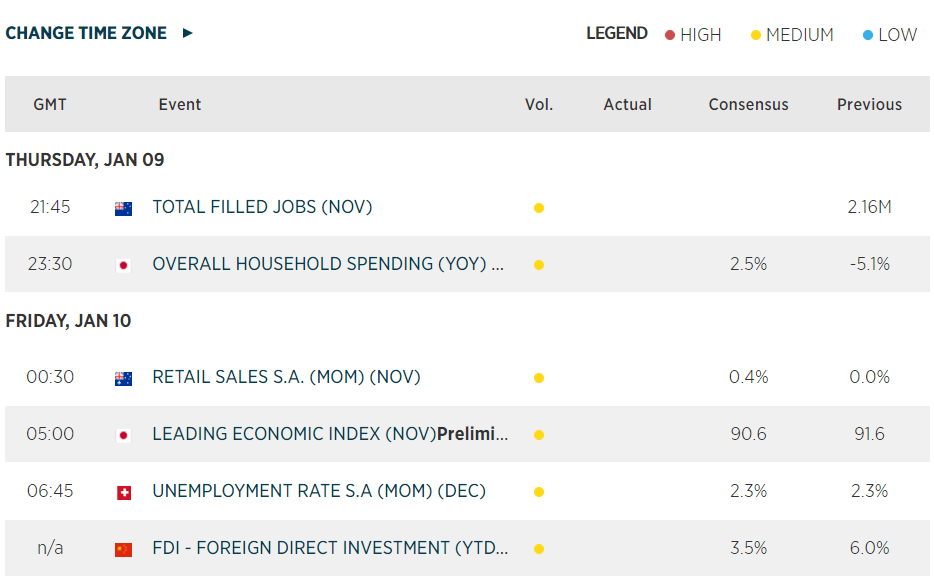

- Traders are shifting their eyes toward tomorrow’s always important Non-Farm Payrolls report, with expectations centered around a reading of about 160k jobs and a 0.3% m/m rise in wages – see our full report here.

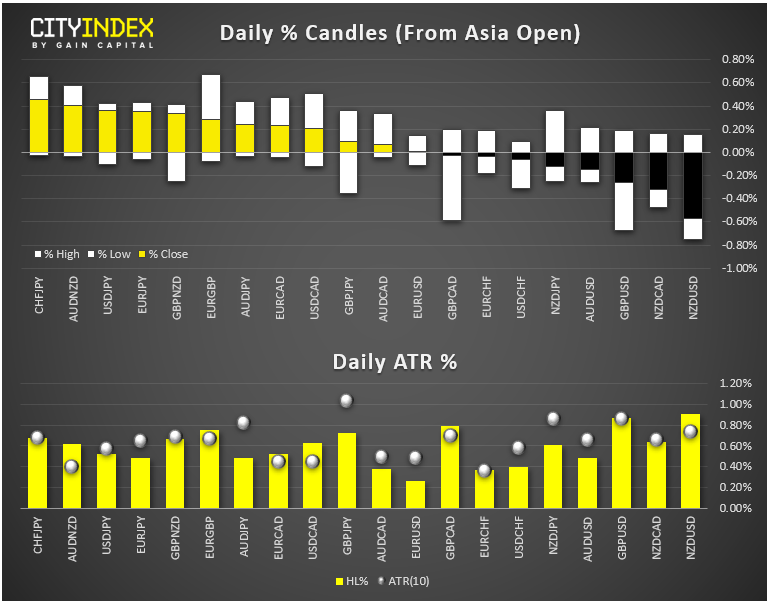

- FX: The strongest major currency on the day was essentially a tie between the Swiss franc, euro and US dollar. The weakest currency was the New Zealand dollar. The loonie also ticked lower after a round of disappointing Canadian data.

- Commodities: Oil was essentially flat after yesterday’s dramatic bearish reversal while gold ticked about 0.5% lower on the day.

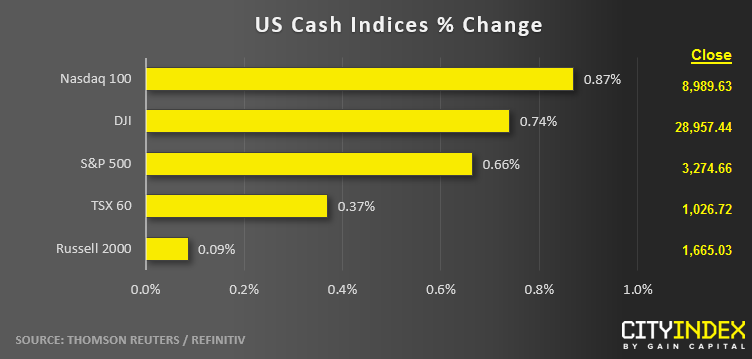

- US indices closed solidly higher to set fresh record highs again today, with most of the move occurring at the open while afternoon trading was quiet. European indices finished higher, highlighted by Germany’s DAX rallying 1.3% to close at a fresh 2-year high.

- Technology (XLK) was once again the strongest major sector on the day. REITs (XLRE) brought up the rear, though all sectors finished higher on the day.

- Stocks on the move:

- Boeing (BA) bounced back 1.5% today as the most recent news suggests a missile may have taken down a flight in Iran earlier this week, rather than a mechanical issue with Boeing’s plane itself.

- Retailers Kohl’s (KSS, -7%) and Bed Bath and Beyond (BBBY, -19%) each dropped sharply after reporting weak sales over the critical holiday shopping period.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Forex articles

Yesterday 06:01 AM

April 17, 2024 02:40 PM

April 17, 2024 04:47 AM