Stock market snapshot as of [30/8/2019 6:58 PM]

- Stock markets are bedding down to a lacklustre end to an indecisive week and a torrid month. The incongruousness of earlier stock index gains looks to have caught up with investors. An advance at Friday’s open was based on less than plausible hopes that China and the U.S. would soon re-engage in increasingly urgent trade talks. Beijing has signalled it won’t immediately retaliate to the latest round of Washington tariffs set to kick in on Sunday, but neither the U.S. nor China have been prepared to confirm that high-level talks mooted for September will actually go ahead

- The real-time trigger for Wall Street’s the retreat might have been mixed U.S. consumer data combined with the Fed’s favoured Personal Consumption Expenditures gauge of inflation that remained well below the Fed’s 2% target in July. Overall, there’s a sense that the economy, whilst strong relative to global growth, is stuck on a low gear

- Pictures of Hurricane Dorian progressing towards a strike on Florida’s eastern coast on Labor Day weekend may also be chilling sentiment. Whilst the storm isn’t forecast to hit regions with major oil production, thus offering little help to fuel prices, orange juice futures have spiked. 60% of the Florida’s main orange-growing region could be affected

Stocks/sectors on the move

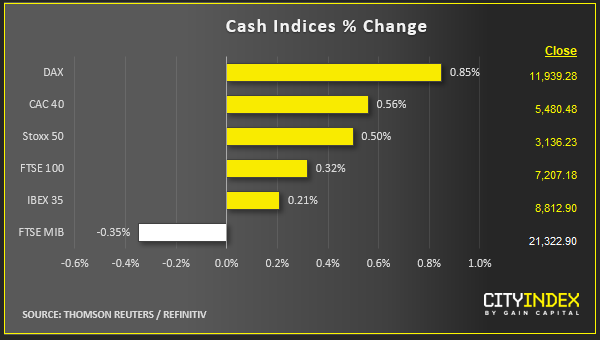

- European markets contrasted with U.S. indices by posting a second-consecutive day of solid gains. Sectors rose across the board, though property, mining & metal shares and industrial segments outperformed

- S&P 500’s Materials sectors kept up that strength in the U.S. session, though drilling down into the broad grouping showed participation was low. Chemical groups Dow and LyondellBasell were among a narrow selection of gainers, whilst the broader commodity names stayed weak. Chemicals makers rose after Brazil agreed to increase duty-free import quotas to comply with a request from U.S. President Donald Trump

- Ulta Beauty led the worst-performing U.S. industrial segment, Consumer Discretionary, with an ugly 28% slump. The retailer joins forecast-downgrade trend after posting a rare quarterly earnings miss, pointing to weakness continuing into 2020

FX snapshot as of [30/8/2019 6:58 PM]

FX markets

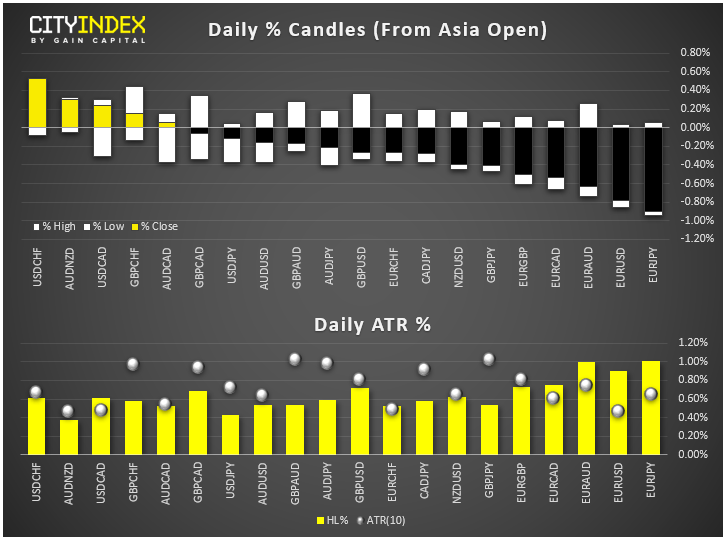

- The euro stands out on the downside with a fresh two-year low as it crosses below $1.10 for the first time since May 2017. A combination of surreptitiously retreating Fed rate cut odds (given a shove by in-line PCE inflation data) and an incoming ECB chief saying there’s room to cut rates even more in the Eurozone is behind the single currency’s latest down leg. There is also no let-up in data that reads ‘economic malaise’

- Boris Johnson’s plan to suspend Britain’s Parliament has survived the first of a raft of legal challenges after a top Scottish judge dismissed a bid to block the move. The Prime Minister’s gambit is interpreted as a means of thwarting MPs who would like to prevent a no-deal Brexit, something Johnson has vowed to trigger if a fresh deal with the EU hasn’t been sealed by 31st October. Sterling reacted by slumping for its third straight session, the first such run of losses since the beginning of the month. There are several more legal challenges in the pipeline

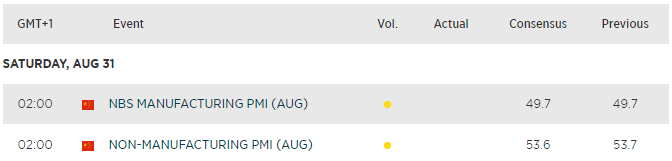

Upcoming economic highlights

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM