Including those of Donald Trump…

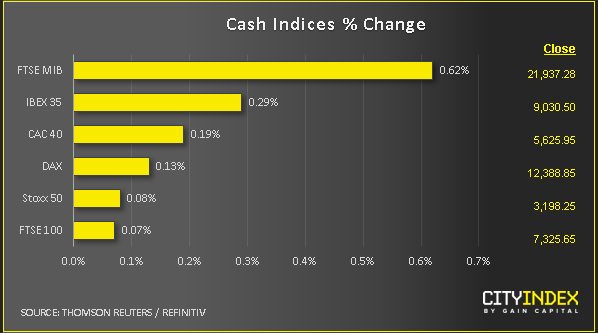

- This is an update as at midday in London. In FX, USD was the top riser while the likes of CHF and NZD were among the weakest major currencies. GBP and EUR also weakened. Among commodities, gold fell on USD strength and crude oil remained on the back foot after yesterday’s reversal. The major EU indices were all in the positive territory.

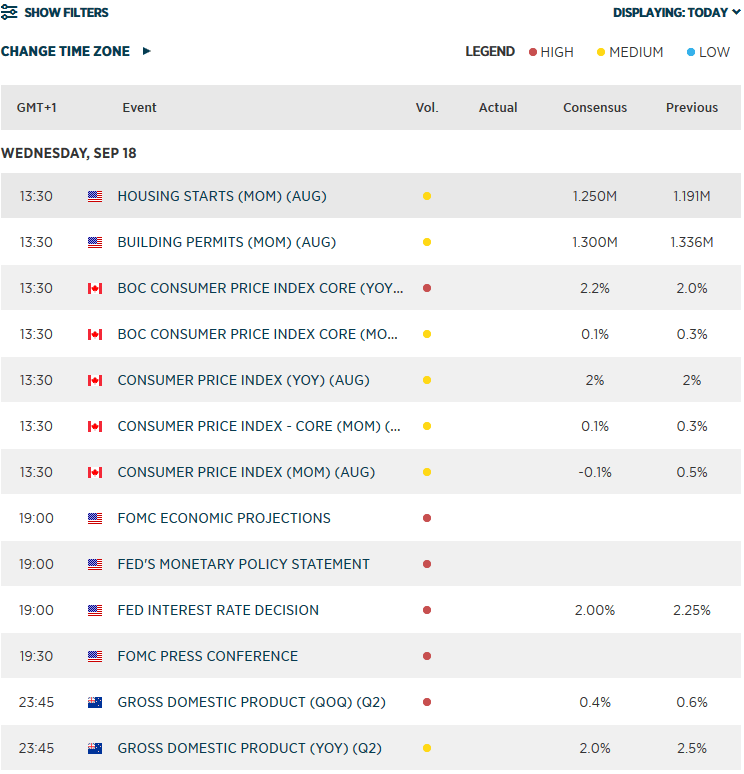

- Tonight, the Federal Reserve is widely expected to cut rates by 25 basis points. The FOMC is also likely to signal that at least one more cut will be arriving later in the year. The US economy has remained fairly resilient and equity indices near record levels, despite trade concerns and weakness elsewhere in the global economy. This begs the question why does the US President Donald Trump desperately want the Fed to lower interest rates to zero?

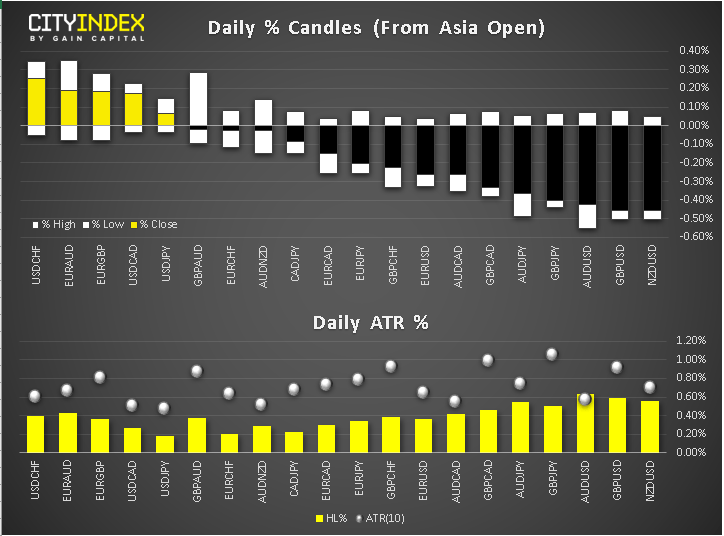

- Saudi Arabia says it has "material evidence" tying Iran to the Kingdom’s oil infrastructure attack. The defence ministry will hold a press conference at 17:30 local time or 15:30 BST to reveal evidence on Iran’s involvement in the Aramco attacks that took place on Saturday. Oil prices weakened further this morning after Tuesday’s drop, but still remain comfortably above the closing price of Friday – so the weekend gap has not been entirely filled just yet.

- UK inflation dipped below the Bank of England’s 2% target, falling to 1.7% year-over-year in August from 2.1% in July, the ONS reported this morning. The drop was more severe than 1.8% economists had expected. Core CPI dipped to 1.5% from 1.9%, likewise more than 1.8% expected. The UK’s Supreme Court will continue to examine the legality of PM Johnson’s decision to suspend parliament over the next few days. Meanwhile Eurozone consumer inflation remained unchanged at 1.0%, according to the final estimates by Eurostat.

- European stock markets edged higher after last night’s positive close on Wall Street, and despite a mixed session for Asia as Japan’s markets fell on news exports contracted for the 9th straight month with an 8.2% y/y slump.

- In corporate news, my colleague Ken Odeluga writes:

- Kingfisher dropped as much as 3% after the home improvement retailer reported a 6% drop in underlying first half profits.

- Deutsche Post shares fell 2%, leading declines by logistics groups after FedEx slashed its profit outlook late on Tuesday, citing a weakening global economy and the trade war.

- Germany's Wirecard rose 3.3%, topping the DAX index. The payments group has formalised an agreement with Japan's SoftBank that includes a convertible bond and expansion opportunities.

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Forex articles

Today 04:00 PM

Yesterday 11:30 AM