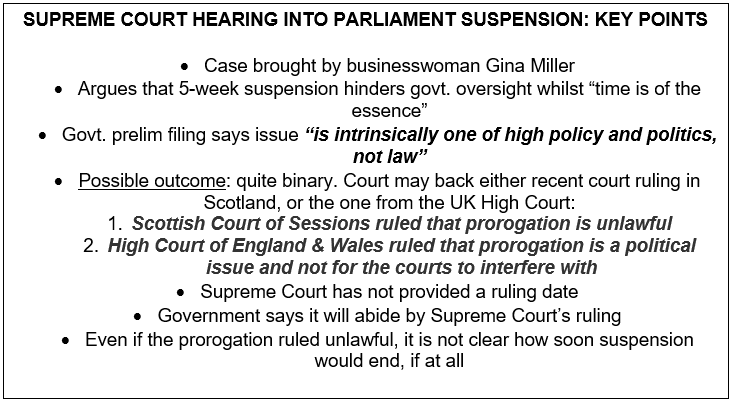

Sterling takes 5 as ‘constitutional crisis’ looms

The Supreme Court hearing into whether Prime Minister Boris Johnson’s suspension of Parliament is lawful, has begun. The case potentially represents the beginning of a ‘constitutional crisis’ that pits the Prime Minister against courts and the Houses of Parliament. Here are some key points.

Market reaction suggests investors are Brexit-ed out for the moment. An enforced hiatus from the beginning of Parliament’s prorogation last week has damped volatility somewhat. The ‘oil supply shock’ may also be temporarily drawing attention away. With Parliament’s anti- no-deal law now established and the Prime Minister’s call for an early election rejected (it can’t happen before 19th November) there’s a sense that the tussle over Brexit would recommence proper when Parliament returns on 14th October at the latest. In the event of a ruling that the suspension was unlawful, it’s far from clear when, of even if Parliament would immediately return.

Meanwhile, PM Johnson says the government is “confident in its court arguments” whilst no-deal planning is continuing “at pace”. The comment comes against the backdrop of a tide of criticism about Downing Street’s strategy from Westminster, Brussels and beyond. The persistent suggestion is that the government isn’t making much of an effort to avoid no-deal, as the clock runs down.

As such, whilst The Bank of England’s statement on Thursday will provide vital updates on policymakers’ inclination to change rates (a new hawkish tilt seems possible) comments will be more for colour than immediate action.

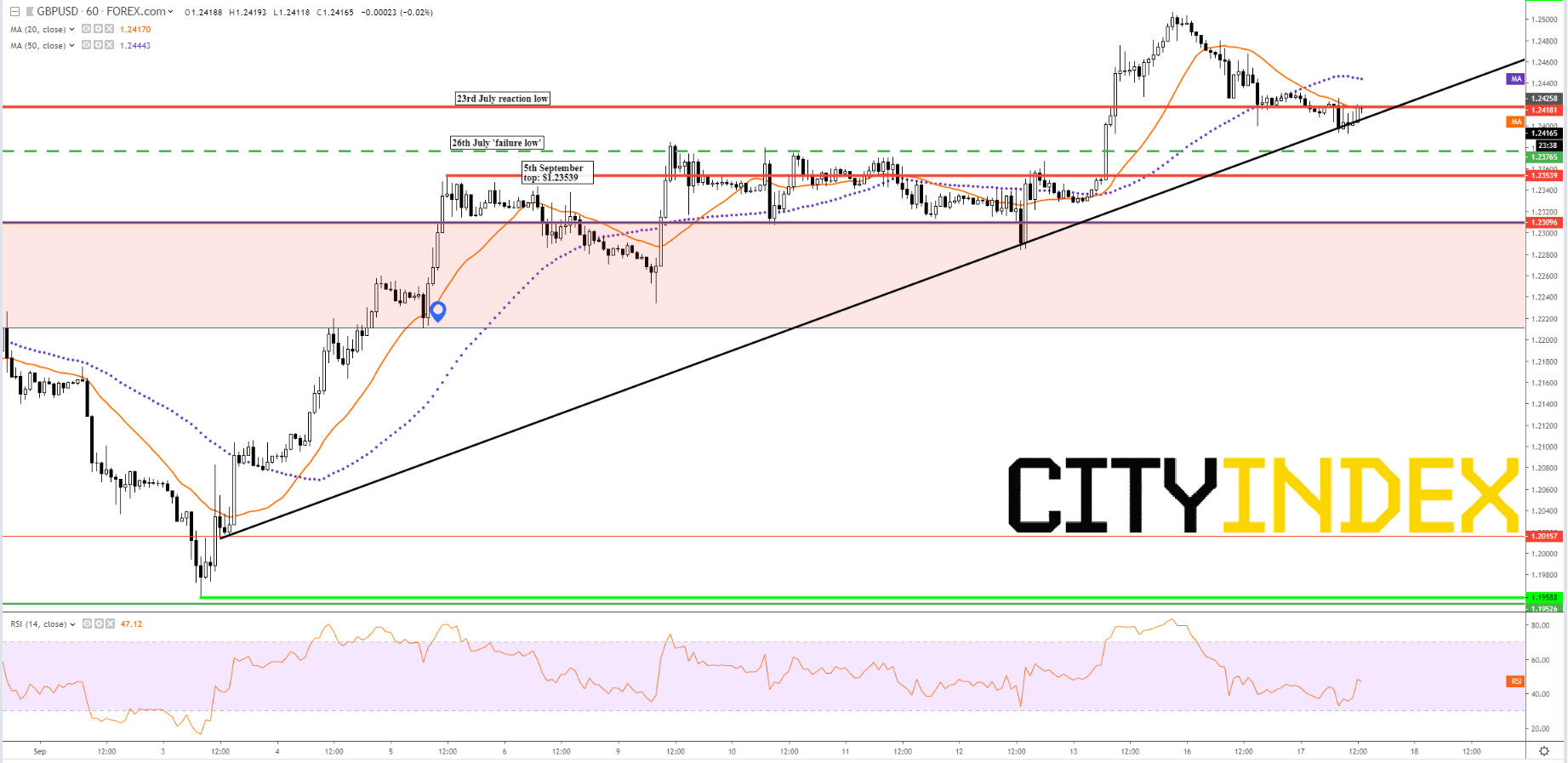

How’s the pound doing?

Quite well, considering. However, sterling has drifted off the seven-week high reached against the dollar last week, partly on profit taking and a wave of ‘risk-off’ sentiment following the attack on Saudi’s key oil plant.

Key technical points

- Deterioration of sentiment could be judged to have deepened if the almost pristine rising trend formed early this month, soon after GBP/USD collapsed to the lowest since October 2016, were to give way

- The rate is flirting with 23rd July’s $1.2418 reaction high. It has been shown to be sensitive again in recent sessions as support; and right now, again, as resistance

- Definitive loss of the level, which bisects the rising line we mentioned near current levels, would also be a moderate negative

- A weaker $1.23765 low (echoing a bounce on 26th July) would be in focus below here, though more downside attention is likely to be on 5th September’s circa $1.23540 top. There, cable consolidated an up leg before breaking to fresh peaks for the month days later. As such, a break below $1.23540 may mark the end of sterling’s relatively bullish bias so far this month

GBP/USD – Daily

Source: City Index

Latest market news

Latest Sterling articles

March 29, 2024 10:00 PM

October 7, 2022 08:58 AM

October 7, 2022 08:58 AM

March 5, 2020 04:13 PM