Lloyds shares slide as PPI eclipses payout rise

Lloyds Banking Group joined the ‘groundhog week’ for UK banks on Friday when it said above-forecast profits were slashed by compensation costs. The news sent Lloyds’ […]

Lloyds Banking Group joined the ‘groundhog week’ for UK banks on Friday when it said above-forecast profits were slashed by compensation costs. The news sent Lloyds’ […]

Lloyds Banking Group joined the ‘groundhog week’ for UK banks on Friday when it said above-forecast profits were slashed by compensation costs.

The news sent Lloyds’ shares down 3% at their worst, despite the now circa-15% state-owned bank hiking its dividend policy.

Lloyds said it would “look to return surplus capital above core capital of about 13%”, but the weight of charges put a negative tint on this and further progress made by the bank during its first half.

So, better-than-expected core income, trashed by bigger-than-expected charges.

A consensus forecast compiled by the bank itself showed analysts were expecting £1.9bn on average.

Chief among the hits to the largest British retail bank’s bottom line in the first half was the biggest charge amongst its peers so far this year for mis-sold loan insurance.

It said it was setting aside an additional £1.4bn.

But Lloyds also highlighted a new set of legal issues related to payment protection insurance (PPI) that may wreak havoc with its own financials in H2 and those of its rivals.

LLoyds said it was not possible to estimate the financial impact of a recent legal development in the PPI saga.

It was referring to a ruling in May against Paragon Personal Finance Ltd, a small financial services firm, in a case brought by one Mrs. Plevin.

A court said Paragon failed to disclose the amount of commission it would receive for selling PPI.

Lloyds concluded it was “not possible to estimate the financial impact of the Plevin decision so no additional provision (was) taken for it, but it is possible the impact could be material”.

A rough tally of the existing data suggests there could be an additional £10bn of total PPI charges left in the pipeline if ‘Plevin’ paves the way for a new set of complaints via the Consumer Credit Act.

Lloyds itself indicated on Friday that there was a moderate risk of a further £1bn in charges in 2H15 and perhaps even £1bn in each half of 2016.

Lloyds also booked a charge to cover an £117m fine by the Financial Conduct Authority relating to aspects of its PPI complaint handling process, and set aside £175m for complaints relating to packaged bank accounts, together with other sums for various other legal issues, making £435m in total for ‘other’ misconduct provisions.

Lloyds’ total regulatory charges so far this year are therefore far above the £850m Barclays announced for the same purpose this week, and the £459m quarterly misconduct and litigation costs RBS revealed on Thursday.

Reassurances by the bank’s CFO on Friday that ‘packaged accounts’ mis-selling “will not be another PPI” were given in good faith, but unfortunately are likely to ring hollow given the bank’s track record.

Lloyds has taken a total of £13.4bn in charges for PPI so far, more than any other bank.

Investor fears that the spectre of PPI could undermine Lloyds’ shiny new dividend policy look difficult to dispel.

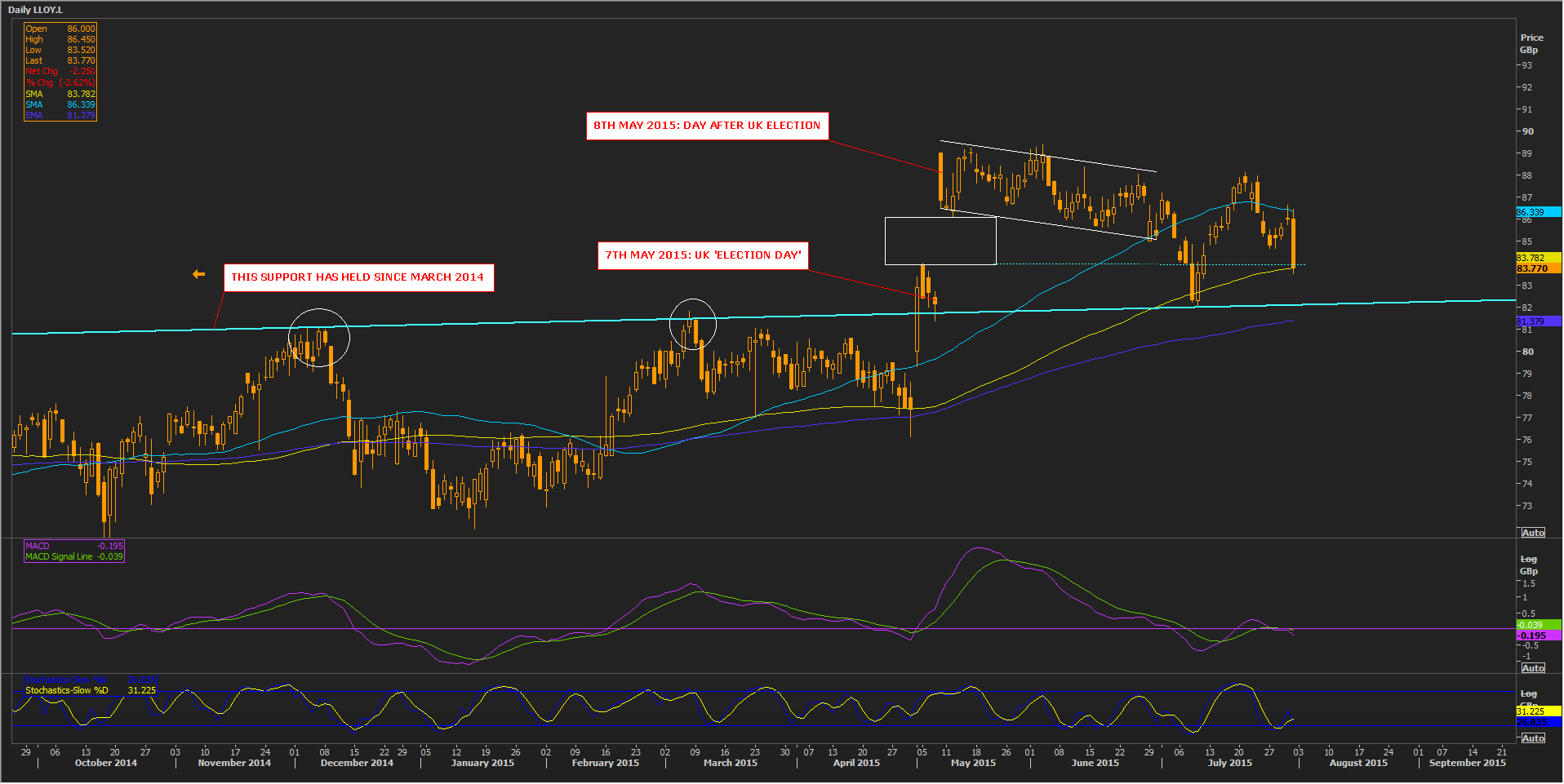

That said, Lloyds’ shares do not reflect as pessimistic a picture for the medium term as the bank’s PPI outlook.

The stock has now completely resolved the gap higher that followed Election Day in May.

A potential bull flag which followed looks to have definitively failed to signify another uptrend.

However, the stock remains above its 100-day moving average and in all probability would also be supported by a line around 82p that extends back to March 2014.

Please click image to enlarge