Last-minute PPI sting won’t be fatal for pay-out plans

As it was for Lloyds Banking Group’s main rivals, the tail of the PPI saga had a sharper sting than expected. Charges related to remediation costs for the two-decade long insurance mis-selling issue amounted to £1.80bn in Q3, against £1.67bn expected by analysts. The harsher than forecast hit partly reflects a last-minute gush of compensation claims that brought Lloyds' buyback plans to an abrupt halt in September.

The group is arguably the best-defended and best-positioned bank focused on the UK for revenues. Yet it is just as hemmed in by economic challenges as peers. Consequently, substantially accelerated growth remains a distant goal. Shareholders have thereby been more focused on capital growth and prospective returns to assess their investment in recent years. So even the hint of a risk to expected higher dividends and share buybacks can be a big deal, particularly with PPI impact also consuming profit targets for the year. (The trading statement didn’t update the bank’s view on its Return on Tangible Equity goal for 2019).

Still, such concerns have been reflected in contained fashion by share price moves in Lloyds stock on Thursday. It retreated by somewhat less than 3% at worst and curbed the loss to about 2% by late morning. Despite Q3 upsets, the buffer of capital Lloyds is obliged to hold as a ratio of total assets improved by a satisfactory extent in Q3. Common Equity Tier 1 Capital stood at 13.5% by quarter end, “in line with the board’s target”. As such, management emits no change to dividend plans and “will give due consideration to the return of any surplus capital at the year end.” Meanwhile, “never say never”, the advice on PPI offered by Lloyds’ previous CEO, remains wise, though post-deadline, claim volumes will continue to decline.

Q3 2019 is yet another quarter Lloyds investors would prefer to forget and that’s reflected in a ten percentage-point share price drop over the last ten days. Still, a firm net interest margin emerged as one of the few high points of the quarter at 2.88% vs. 2.87% expected. Cost control also remained in hand. Lloyds is not compounding past mistakes with new missteps.

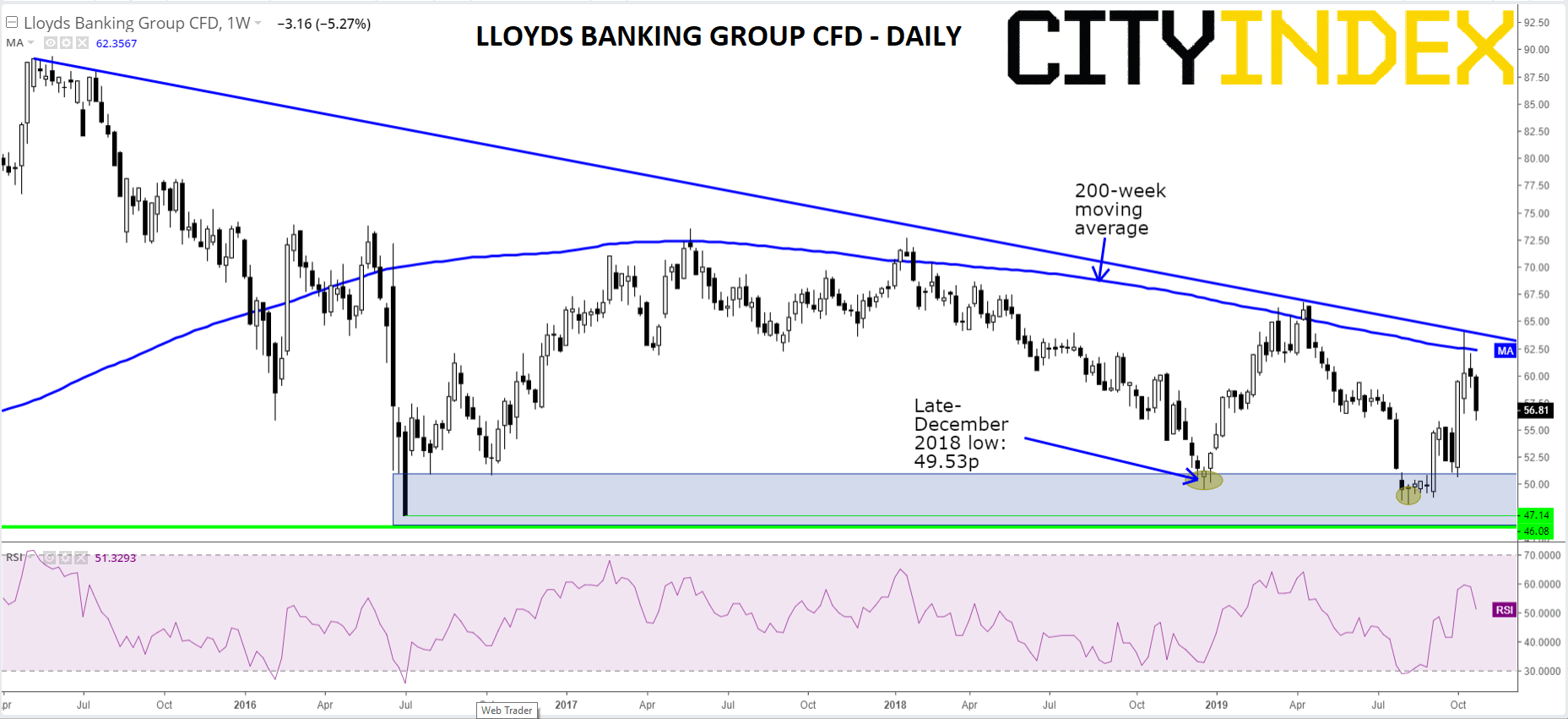

Chart points

Over-arching pressure on the shares that could erode more of LLOY’s remaining 9% rise this year should continue, according to technical analysis. The decline since May 2015 is now well established: see the well-corroborated falling trend line since then that was last tagged in mid-October. The 200-week moving average reinforces trend line resistance given that mid-October also featured another failed attempt to get above the 200-WMA, the latest of many rejections in recent years. So long as overhead structures remain intact, objectives will continue to point towards December 2018’s base at 49.53p, and 2019’s 48.2p low from August. These floors are in within reasonable range of June 2016’s post-referendum lows as deep as 46p.

Lloyds Banking Group Plc. CFD – Weekly

Source: City Index

Latest market news

Today 10:37 AM

Today 08:25 AM

Latest Bank Stocks articles

October 10, 2023 09:31 AM

October 6, 2023 02:28 PM

July 17, 2023 04:03 PM

July 11, 2023 02:28 PM