Lloyds share rebound could be provisional

Lloyds Banking Group shares were up as much as 15% from almost three-year lows earlier this week. A combination of the wider market’s comeback from […]

Lloyds Banking Group shares were up as much as 15% from almost three-year lows earlier this week. A combination of the wider market’s comeback from […]

Lloyds Banking Group shares were up as much as 15% from almost three-year lows earlier this week.

A combination of the wider market’s comeback from a challenging start of the year helped.

So did signs that the UK’s biggest retail lender had been unfairly tarred with the same brush as ‘racier’ European rivals.

Unfortunately though, Lloyds’ reputation for generating bad news offers ample scope for a renewed sell-off, when it reports final 2015 results on Thursday.

A number of issues are bubbling under and could come to the fore.

An additional £1.4bn was set aside in H1 2015, bringing total PPI provisions to more than £13bn.

PPI provisions for the final quarter of 2015 are likely to be £2.5bn-£2.9bn

For H1 2016, as much as £1.1bn is likely.

It’s about HBOS, the bank Lloyds Banking Group took over at the height of the financial crisis in 2008.

About 6,000 investors are suing LBG for £350m after the “financially disastrous” acquisition.

Lloyds has vowed to defend itself against the lawsuit.

That defence and potential unfavourable outcome will come at a cost, which may be revealed on Thursday.

The UK’s Supreme Court ruled earlier this month that holders of Lloyds’ Enhanced Capital Notes (AKA CoCos) have the right to appeal the bank’s decision to buy the bonds back, overturning a Court of Appeal ruling in December.

LBG would save about £1bn if it bought the remaining £3.3bn of a total £8.4bn CoCos it issued as part of its 2009 bailout.

Lloyds said in late January it would launch a tender offer for the £2.6bn bonds that haven’t reached maturity.

It said it would redeem at ‘face value’ the ECNs not subject to the tender, worth around £700m.

After rule changes, the ECNs are no longer deemed regulatory capital, and hence are just expensive borrowing.

The ECN Saga could also fatten provisions.

But the global stock market sell-off gave the Chancellor of the Exchequer, George Osborne, pause for thought. He said the sale would only take place “when the time is right.”

Another plan to continue carefully filtering shares into the market each month was extended in December, keeping a lid on the stock.

Lloyds says the timing of any future offering is for the government to decide, but it’s worth listening out for clues on Thursday.

The final major focus point is dividends.

Under the current circumstances, market yield forecasts as high as 5% for 2016 (vs. current ~1%) look too optimistic.

We expect a final payment of 1.75p for 2015, bringing the total for the year to 2.5p.

Our other main forecasts are below.

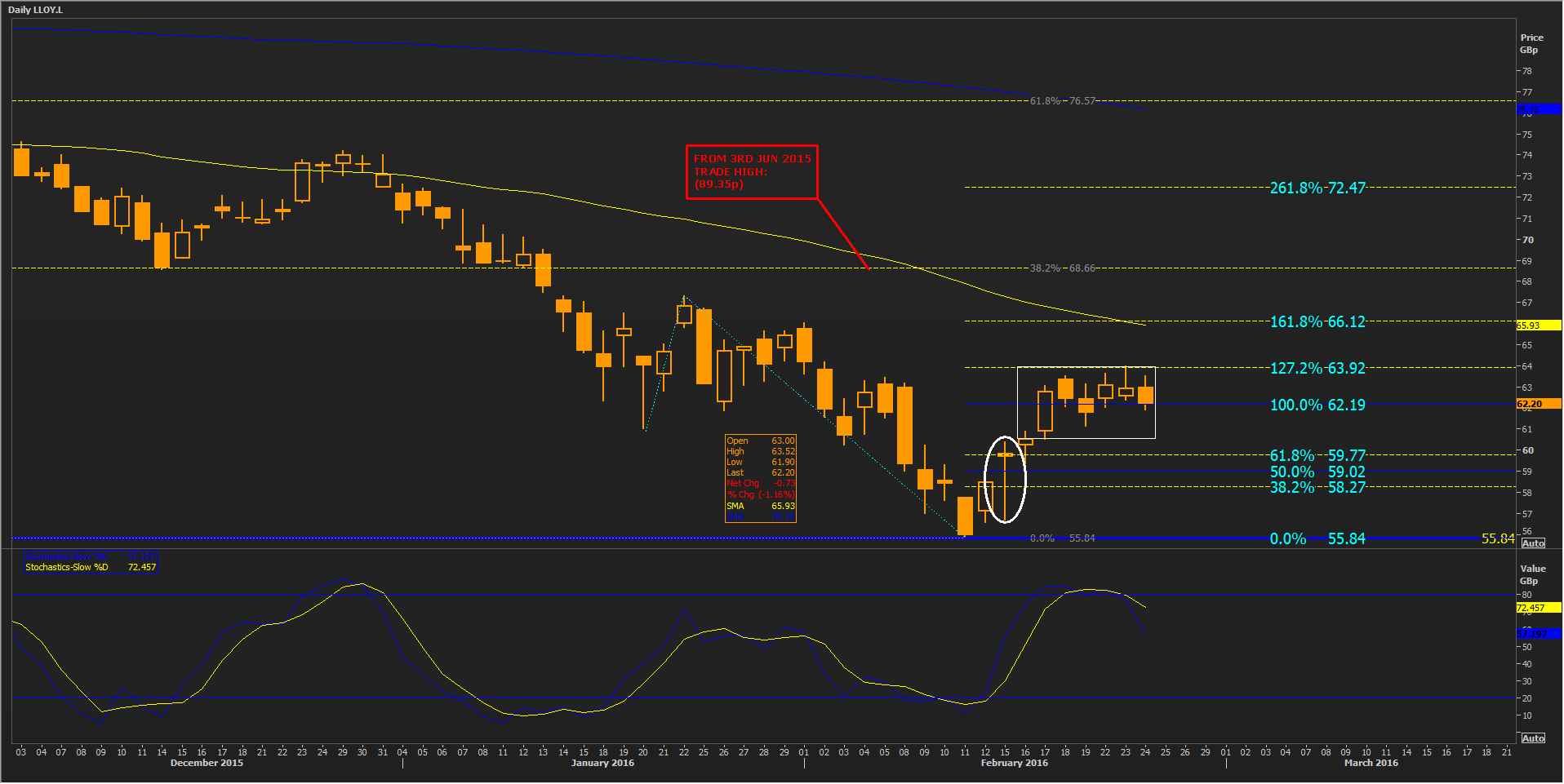

For the shares, the main watch point in the event of a dissatisfied market reaction will be moderate support around 62p, the base for the shares so far this week.

The price also equates to 100%, by extension, of a rise and slide that commenced on 20th January.

Trade below 62p could come under the influence of the ‘long shadow’ doji, seen on the 15th.

Given that sellers took over on that date, the shares may quickly head back to a re-test of three year-lows at 55p.

Please click image to enlarge