The best-performing big UK bank stock needs fresh impetus

On Thursday, Lloyds Banking Group, Britain’s biggest mortgage provider, reports its first set of earnings since Britain’s planned departure from the EU was put off till 31st October. The group and its shares will be sharply in focus as investors continue to gauge the impact on the UK lender with the biggest exposure to Brexit risks.

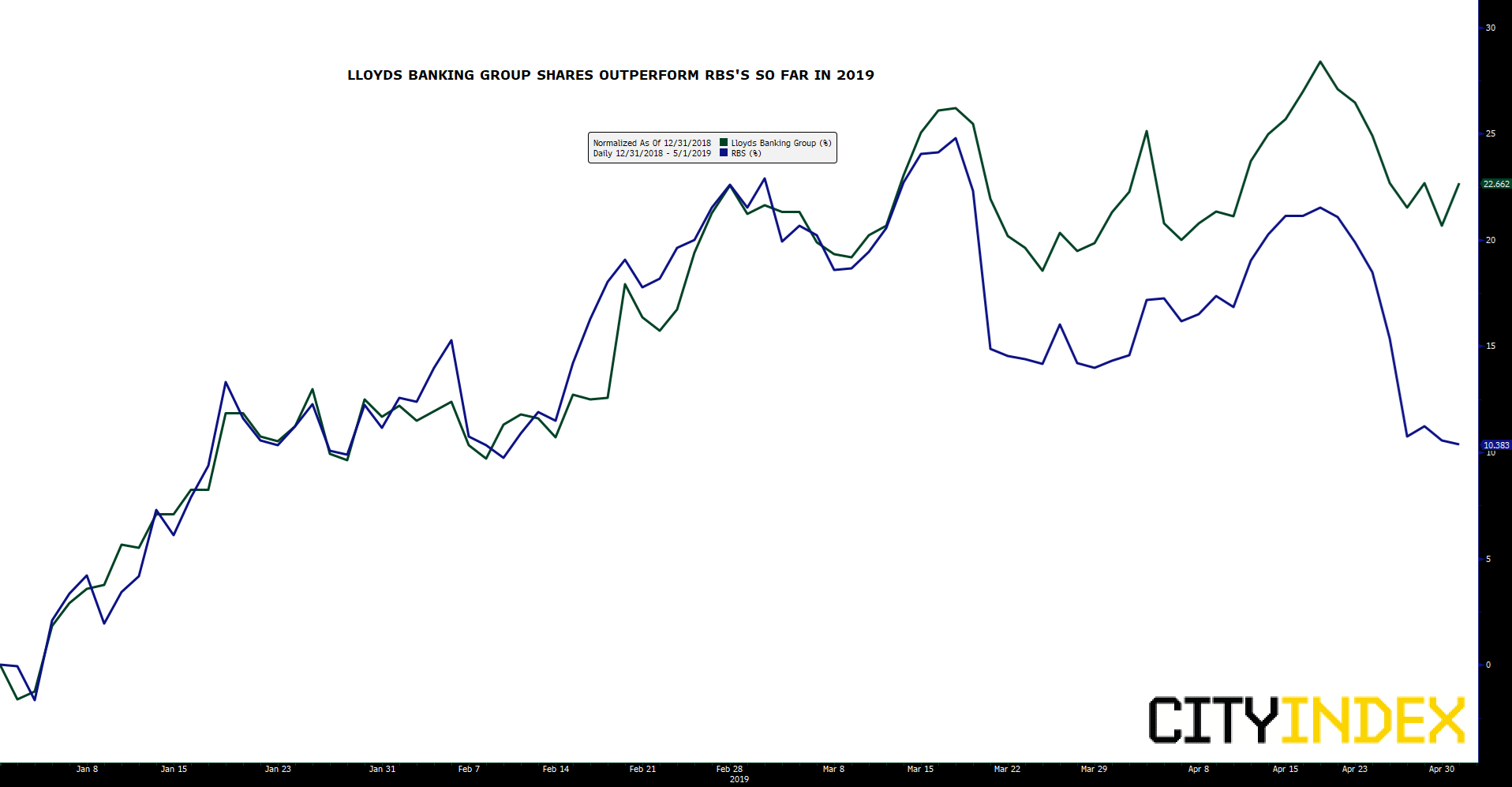

Although the shares have ceded some of their advance as much as 28% higher by mid-April, sentiment on the stock still largely reflects assured investor confidence following the bank's solid performance in 2018. Lloyds was still 22.6% above its price at the beginning of the year by Wednesday’s close. That compares with shares in close rival, RBS, which were up 10.3%, even after resilient headline earnings last week.

Lloyds enjoyed another boost on Wednesday when the UK bank regulator reduced the level of capital deemed necessary to ensure it can survive a financial or economic emergency. The Prudential Regulation Authority trimmed its Systemic Risk Buffer for Lloyds, allowing the group to reduce its core capital target to 12.5% from 13%. This bolsters hopes that the group’s leeway to raise capital returns to shareholders in the form of dividends or buybacks is increasing. Market forecasts project an annual capital return of £4bn-£5bn. Any hints of more, offer the best chance for the stock to extend its lead against close peers in 2019.

If the bank does little to underpin such hopes on Thursday, its stock may have few sources of impetus to extend gains further in the medium term, implying it could begin to drift lower. It may still do so, if the extent of any pay out undershoots what’s now roughly priced in. After all, the odds that revenue growth can gear up are slim, even if Lloyds’s key net interest margin is unlikely to slip below 2.9%. Increasing efficiency should keep pushing the cost-to-income ratio well under 40, but the real prize would be if higher-margin wealth and insurance growth accelerated. That’s a distant prospect.

Normalised price chart: Lloyds Banking Group, RBS – year to date

Source: Bloomberg/City Index

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Lloyds articles

April 21, 2024 04:00 AM

February 22, 2023 02:59 PM

February 20, 2023 09:18 AM

July 27, 2022 08:00 AM