Lloyds Bank stuck in a Brexit trap

Profits are largely unchanged year-on-year, but the early share price sell-off of some 3% on Wednesday tells us Lloyds Bank’s very patient investors aren’t pleased. […]

Profits are largely unchanged year-on-year, but the early share price sell-off of some 3% on Wednesday tells us Lloyds Bank’s very patient investors aren’t pleased. […]

At a few points during the quarter to the end of September, there have certainly been grounds to fear that underlying profit would slide below the £1.97bn level booked in Q3 last year.

However we notice consensus in recent weeks had been inching well above the £1.912bn underlying net income the group has reported.

Hopes have been rising that the absence of a clear structural economic hit and (probably) delayed fallout from the collapse of the pound would mean a relatively unhindered LBG performance in Q3.

In the event, comparable profits look as much as 9.3% light of the typical City forecast, and 3% weaker than the ‘flat’ view.

Furthermore, there’s no additional announcement of self-help (also known as cost measures) having taken place within the bank during the quarter, even if we recognise that management probably thought it prudent to hold fire whilst the dust to settled, and to keep a rein on sentiment.

Lloyds’ CFO Culmer has simply pledged this morning that “there is more to come”.

Perhaps the most positive note is the signal from the group’s CFO that its latest PPI provision of £1bn is the final one the bank expects to take given that it is intended to cover the period up until the recently pushed-back deadline.

In the meantime of course, it is that very payment which has taken a big bite out of profits and, potentially, prevented Lloyds from taking as much advantage as possible from what still looks set to be a delayed hit from the referendum outcome.

Looking deeper into this morning’s figures and then looking further ahead, the crucial Return on Equity figure—that will probably be the decider on profitability and dividends going forward—remains problematic.

Unadjusted (as presented by the bank) it probably is a little over 1%.

If we wash out the effect of the new PPI provision (assuming 12 quarters of amortised installments till 2019) , a one-off corporation tax hit, and even fail to give LBG the benefit of the doubt that a £150m packaged accounts provision won’t recur, then ROE looks more viable around 11%, meaning above real financing costs.

With difficulty, not least because it’s quite the unknown.

For now, shareholders can be expected to simply be thankful for the group’s good fortune—the shares have duly recouped most of their sharper loss on Wednesday morning.

Lloyds numbers can also serve as a benchmark for the other UK-focused giant lenders that will report his week, Barclays and RBS.

Working out relative performance won’t be easy of course, due to the now routine obfuscation of ‘one-off’ items.

But any hint that they’ve taken a bigger hit than LBG won’t play well.

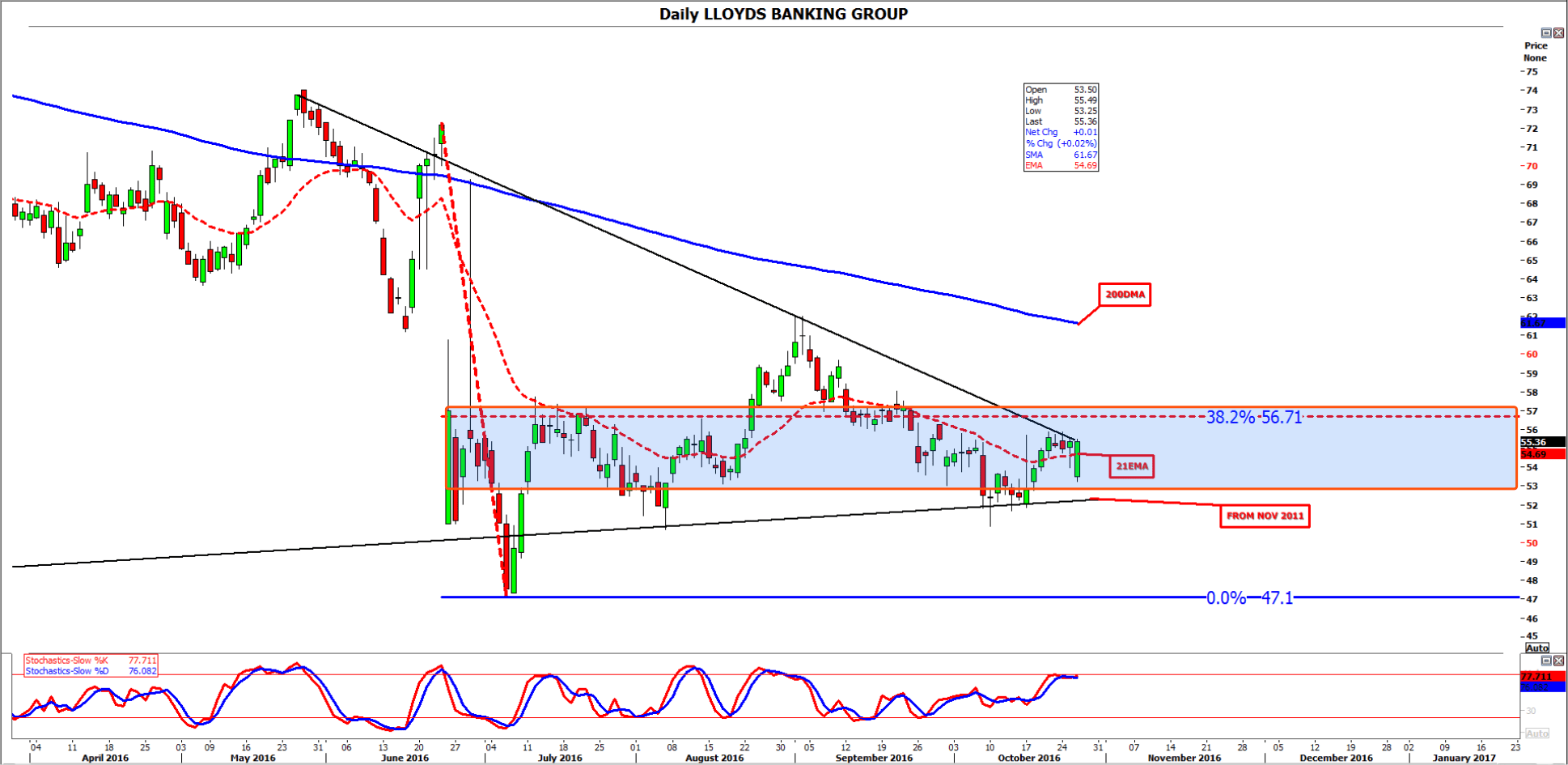

Please click image to enlarge