LIVE BLOG Autumn Statement 2013

Welcome to our live blog on the Chancellor’s Autumn Statement. We will keep this page updated with new information as and when it is announced […]

Welcome to our live blog on the Chancellor’s Autumn Statement. We will keep this page updated with new information as and when it is announced […]

Welcome to our live blog on the Chancellor’s Autumn Statement. We will keep this page updated with new information as and when it is announced by George Osborne.

To get the latest updates, please press F5 button on your keyboard or refresh this page.

SUMMARY

So that’s it. The 2013 Autumn Statement has been delivered. The tone of the statement was very much one of ‘traction.’ The hard times of the last two years is starting to gain traction in terms of the UK economic recovery. The recovery bus is moving. Both OBR forecasts on borrowing and GDP was no surprise and that’s why the markets did not react with any sort of volatility or speed to the statement itself.

We hope you enjoyed our LIVE BLOG and stay tuned to the City Index website for more market and analysis.

Feel free to tweet myself at @Josh_Cityindex or @Cityindex for your comments and feedback. Keep an eye on the ECB rate decision at 12.45pm and best of luck with non farm payrolls tomorrow.

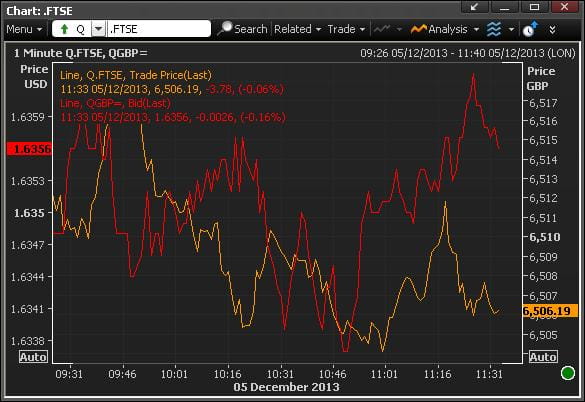

Here’s a final chart tracking the movement of the FTSE 100 and GBP/USD following the Autumn Statement. The vertical line marks the start of the statement. FTSE in orange and GBP/USD in red.

UPDATES:

12.06pm

Ed Balls now up to challenge Osborne’s statement.

12.05pm

Osborne finishes with “Britain is moving again. Lets keep going.”

12.02pm

UK FINANCE MINISTER OSBORNE – WILL CANCEL NEXT YEAR’S PLANNED 2 PENCE/LITRE RISE IN PETROL TAXES AND OTHER FUEL DUTY INCREASES

12.01pm

UK FINANCE MINISTER OSBORNE – WILL REMOVE EMPLOYER NATIONAL INSURANCE CONTRIBUTIONS FOR PEOPLE AGED UNDER 21

12 noon

Bank of England leaves interest rates and QE levels on hold. That’s no surprise and market as expecting more of the same. Next up is the ECB announcement at 12.45pm. No change expected there also but Mario Draghi has surprised the market before so don’t take your lunch break just yet!

12 noon

Hope you are enjoying the blog. This is our first LIVE BLOG. Hopefully more to come. Let us know your thoughts. Tweet us at @Josh_Cityindex and @Cityindex

11.59am

Business rates capped at 2% rise and £1,000 discount given to small high street retailers. Re-occupation relief to help those new to high street to take up stores vacant.

11.57am

UK FINANCE MINISTER OSBORNE – WILL CAP INCREASE IN BUSINESS RATES PROPERTY TAX AT 2 PCT FROM APRIL 2014

UK FINANCE MINISTER OSBORNE – WILL INTRODUCE TAX RELIEF FOR TENANTS MOVING INTO VACANT COMMERCIAL RETAIL PROPERTY

11.55am

UK FINANCE MINISTER OSBORNE – WILL ABOLISH STAMP DUTY TRANSACTION TAX FOR SHARES PURCHASED IN EXCHANGE TRADED FUNDS

11.50am

Latest chart here. The vertical line marks when Osborne started the statement. FTSE in orange and GBP/USD in red.

11.48am

2 more banks on Help to Buy now. That will drive down APR rates on offer and likely increase demand for it. fuelling house price bubble.

BUT – now the #BoE can take action to mitigate against asset bubbles….hmmm house price forward guidance?

11.47am

HELP TO BUY – 2 more banks will join the scheme this month including Virgin.

Want a responsible recovery. Bank of England to take action on asset bubbles if they threaten financial stability.

11.45am

UK FINANCE MINISTER OSBORNE – ANNOUNCES NEW TAX ALLOWANCE TO ENCOURAGE INVESTMENT IN SHALE GAS THAT HALVES TAX RATES ON EARLY PROFITS

11.44am

UK FINANCE MINISTER OSBORNE – WILL RAISE BANK LEVY TO 0.156 PCT FROM JAN 2014

11.43am

UK FINANCE MINISTER OSBORNE – TO INTRODUCE CAPITAL GAINS TAX ON FUTURE GAINS MADE BY NON-RESIDENTS ON SELLING UK RESIDENTIAL PROPERTY FROM APRIL 2015

11.42am

UK FINANCE MINISTER OSBORNE – WILL RAISE 9 BLN STG OVER NEXT 5 YEARS FROM TACKLING TAX AVOIDANCE AND EVASION

11.37am

UK FINANCE MINISTER OSBORNE – AS MILITARY WIND DOWN OPERATIONS IN AFGHANISTAN, WILL REDUCE MILITARY SPECIAL RESERVE BY FURTHER 900 MLN STG

11.36am

UK FINANCE MINISTER OSBORNE – WE WILL CAP OVERALL WELFARE SPENDING

UK FINANCE MINISTER OSBORNE – AUTUMN STATEMENT FISCALLY NEUTRAL OVER FORECAST PERIOD

11.33am

Chart of FTSE 100 and GBP/USD during the Autumn Statement here. Both barely moving. Why? Cause there are no surprises so far.

11.29am

UK FINANCE MINISTER OSBORNE – SET TO BORROW 73 BILLION POUNDS LESS OVER 5-YEAR PERIOD THAN WAS FORECAST IN MARCH

UK FINANCE MINISTER OSBORNE – OBR FORECASTS PUBLIC SECTOR NET DEBT AS PCT OF GDP TO BE 75.5 PCT THIS YEAR

UK FINANCE MINISTER OSBORNE SAYS PUBLIC SECTOR NET DEBT TO FALL AS A SHARE OF GDP IN 2016/17 (MARCH FORECAST 2017/18)

11.26am

UK’S OSBORNE – OBR FORECASTS SHOW 2013/14 BUDGET DEFICIT OF 6.8 PCT OF GDP (MARCH FORECAST 7.5 PCT – PSNB EX ROYAL MAIL EX APF)

UK’S OSBORNE – OBR FORECASTS SHOW 2014/15 BUDGET DEFICIT OF 5.6 PCT OF GDP (MARCH 6.5 PCT – PSNB EX ROYAL MAIL EX APF)

UK’S OSBORNE – OBR FORECASTS SHOW 2015/16 BUDGET DEFICIT OF 4.4 PCT OF GDP (MARCH 5.5 PCT – PSNB EX ROYAL MAIL EX APF)

11.25am

Osborne clearly enjoying this statement more than any of the others.

11.24am

UK FINANCE MINISTER OSBORNE – OBR FORECASTS UNEMPLOYMENT TO FALL TO 7 PCT IN 2015

UK FINANCE MINISTER OSBORNE – OBR SEES UNEMPLOYMENT FALLING TO 5.6 PCT BY 2018

11.23am

Employment OBR forecasts higher. Jobs to rise by 400,000 this year.

11.23am

FTSE 100 and Sterling both barely moving. #Dampsquib?

11.20am

UK’S OSBORNE – OBR FORECASTS SHOW 2013 GDP GROWTH OF 1.4 PCT (MARCH FORECAST 0.6 PCT)

UK’S OSBORNE – OBR FORECASTS SHOW 2014 GDP GROWTH OF 2.4 PCT (MARCH 1.8 PCT)

UK’S OSBORNE – OBR FORECASTS SHOW 2015 GDP GROWTH OF 2.2 PCT (MARCH 2.3 PCT)

11.19am

There was no double dip recession

11.19am

OBR:

Recession was staggering 7.2% – sharpest fall in national income of any developed country in the world

11:18am

UK FINANCE MINISTER OSBORNE – BUSINESS TAXES STILL TOO HIGH, EXPORTS TOO LOW, MUST ADDRESS THIS

11.18am

UK FINANCE MINISTER OSBORNE – BIGGEST RISK TO UK ECONOMY WOULD COME FROM ABANDONING PLAN FOR FISCAL CONSOLIDATION

11.16am

Britains economic plan is working but the job is not done. We need to secure the economy in the long term

11.15am

Autumn Statement. Here we go.

11.12am

Statement due imminently. Let me know what you think of it by posting your comments below or tweeting me at @Josh_Cityindex

11.06am

Take a look at the FTSE 100 below. Its right at its lower trend line. This means we have an important week of trading coming up and there is of course no shortage of volatility. We have the Autumn statement, BoE and ECB to make statements today and of course non farm payrolls tomorrow. Keep an eye on this one.

The FTSE has always risen in December for the last decade an average of 142pts. But if we fall below this lower trend line, that historic behaviour becomes under threat. However, many traders who want to buy into this market are looking at this as an opportunity, particularly if the FTSE bounces from this lower trend line support.

What will you do?

11.00am

Of course Autumn Statements are just as much about the politics as the economics. Traders and the markets will be looking purely at the numbers. The key focus is borrowing figures, which will impact the guidance that credit ratings agencies such as Fitch have on the UK’s ability to service its debt. In addition, keep an eye on the OBR upgrades to the UK’s economic outlook and GDP forecasts for the next 3 years. Given the strong rise in manufacturing output, where PMI services remained at 60.0 in November, GDP continues to provide an upward surprise.

10.58am

Quick markets check.

10.40am

So here were are. Its that time of the year for the Chancellor’s Autumn Statement. Of course, right on queue, most of the interesting details had already been well leaked into the Sunday Press. So here is what we know already: