Kingfisher shares leap on big refurb

News of a sweeping revamp of Kingfisher Plc., that’s trickled out over the last few days, continues to win applause, lifting the stock as much […]

News of a sweeping revamp of Kingfisher Plc., that’s trickled out over the last few days, continues to win applause, lifting the stock as much […]

News of a sweeping revamp of Kingfisher Plc., that’s trickled out over the last few days, continues to win applause, lifting the stock as much as 5% more on Tuesday.

Albeit, tardy, Europe’s biggest DIY retailer embarking on a top-to-bottom refurb is exactly what was needed to offset full-year pre-tax profit sliding 7.5% to £675m.

What’s more remarkable is how long it’s taken the firm to decide on what probably amounts to its most significant reorganisation for a decade.

The issues the B&Q owner is beginning to address have been bubbling under at least since 2013, when Kingfisher bought 135 stores in Western Europe from Germany-based Hornbach, taking its total store count early in 2013 to 1,137 in 17 countries, 81% outside the UK and 15.75% outside Western Europe.

KGF’s acquisitive thirst of the last couple of years left it with a financial profile incongruously on a par with Home Depot.

HD quick ratio: 0.4, KGF: 0.5; HD current ratio: 1.4, KGF: 1.2.

But of course, HD’s equity value is about 12 times the size of KGF’s

Something had to give and finally, and fortunately voluntarily, it has.

It’s worth noting there is already an unexpected benefit of what we can call Kingfisher’s new financial discipline, which may have been in effect for months—net cash has risen to £329m.

That’s a rise of £100m on the year, 38% of that apparently booked since Q3.

Any implied discount to Kingfisher’s 42 times price-to-free cash flow at last count would be welcome, given the, again, questionable premium compared to Home Depot’s 36 times.

But medium-term challenges are considerable—underscored by £34m-worth of currency impact (mostly €) and £22m “country development” charges in the full-year outcome.

Expect further items like these in the year ahead, although no doubt, this week’s news is welcome.

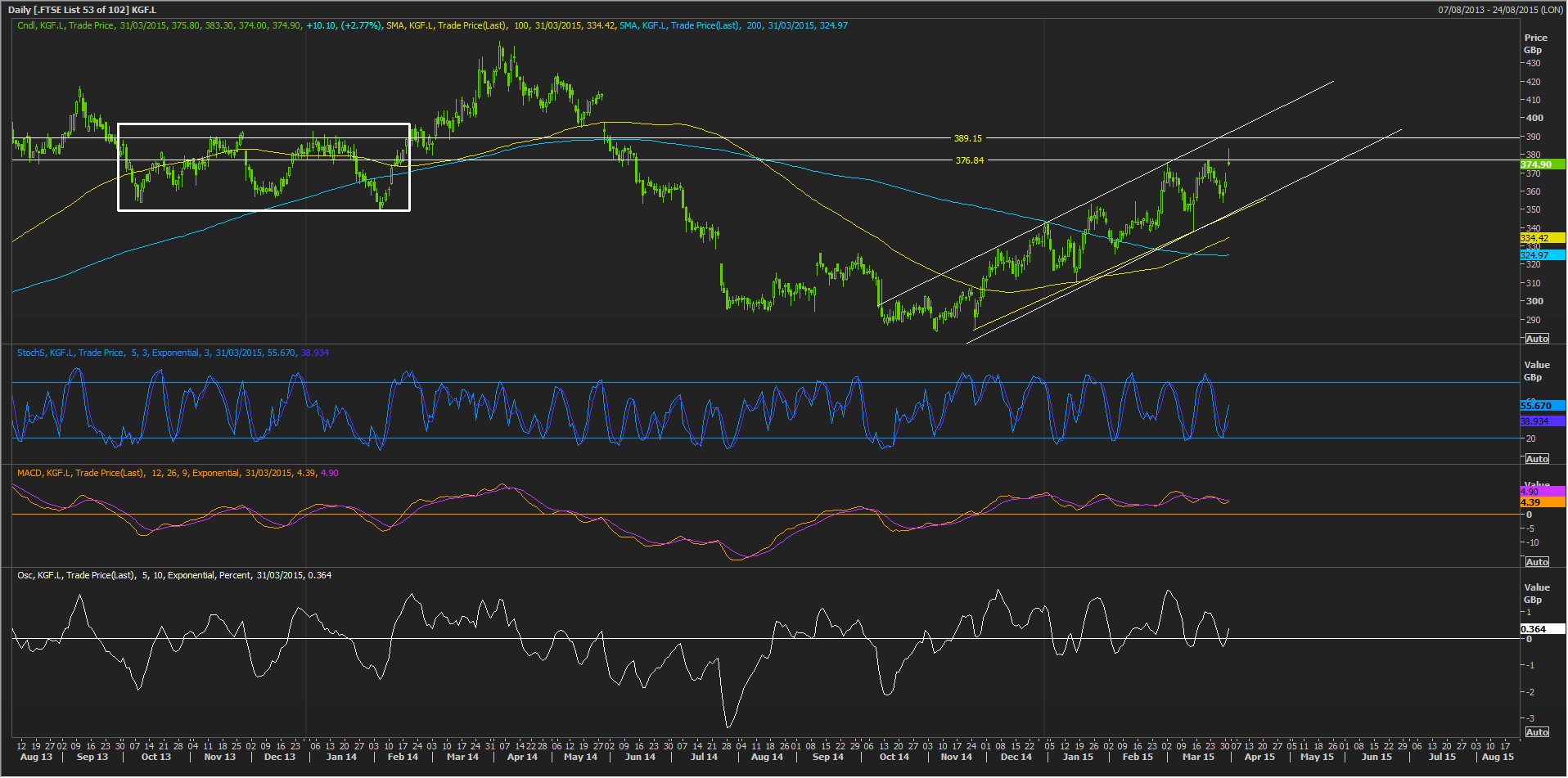

For now, we have fair reason to regard the stock as demonstrably supported at current levels, momentum as good.

On that basis there could be upside for the rest of the week at least, equating to a further 2.5% or slightly more.