Just Eat delivers just enough

Just Eat shares have now recovered all of the loss they suffered after its CEO’s sudden decision to resign last month due for personal reasons.

Just Eat shares have now recovered all of the loss they suffered after its CEO’s sudden decision to resign last month due for personal reasons.

Just Eat shares have now recovered all of the loss they suffered after its CEO’s sudden decision to resign last month due to personal reasons.

Shareholders can get back to savouring its long-standing strengths, and chewing over its well-known weaknesses.

The trigger for sentiment to snap back was of course that 2016 earnings were reassuringly in line with expectations. It’s curious to note though that a slump of the shares at the beginning of the year accelerated on 10th February after CEO David Buttress said he’d leave by the end of March for “urgent family matters”. Long-term holders will also recall Just Eat lost another CEO in seemingly similar circumstances when Klaus Nyengaard stepped down in 2013, after five years in charge, saying he wanted to spend more time in his home country of Denmark. (Chairman John Hughes will step in as interim CEO during the search for a permanent replacement.)

It would be little surprise for investors if the pressures of building Just Eat into the UK’s biggest online takeaway company are in fact difficult to stomach for more than a few years. Just Eat does after all dominate the British Internet takeaway market. It is 10 times larger than its closest competitor. The group (and its top management) have had to be aggressive to grow.

The City’s best intel suggested investors should not read anything more into events surrounding CEO Buttress. But coming so close to earnings, shareholders inevitably thought dark thoughts. In the event, underlying earnings almost doubled to £115m, albeit they ‘only’ matched expectations. It’s worth noting that for a fast-growing group with equally fast-moving shares, on-target earnings can often bring a fast sell-off. After all, the group’s ravenous expansion over the years actually leaves 2016’s 93% profit growth looking modest. Earnings soared 163% year-on-year in 2015.

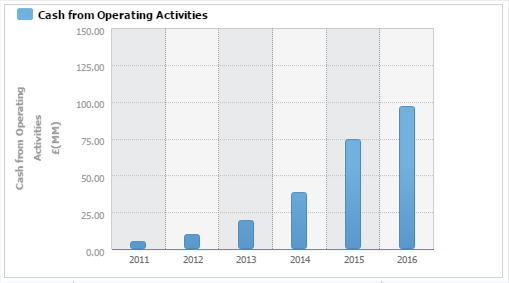

Another sign that investors are being weaned of expectations of high double and triple-digit growth, was their apparently sanguine reaction to the CFO’s comment on Tuesday that he was “comfortable” with consensus for “mid-to-late teens” order growth in the UK. If we’re reading shareholder response accurately, they’re taking a rational view. The group converted more than 90% of underlying earnings before interest depreciation and tax into cash flow in each of the last two years, pointing to the benefits of its growing scale as well as strenuous efforts to remain efficient. And whilst Just Eat’s phase of eye-watering sales growth might be coming to an end, the group continues to generate plenty of the main ingredient required to achieve the top end of underlying earnings expectations this year: cash. The graphic below suggests Just Eat can, for now at least, afford to secure its share of a market that is estimated to grow to around £8bn by the end of the decade.

Just Eat Plc. cash from operating activities 2011-2016; source: Thomson Reuters

To be sure, the battle is going to be a fierce one. Whilst Just Eat can probably be true to its name a few more times by simply acquiring rivals, there are limits imposed by financing, ease of integration, and, after last year’s buy of its biggest rival, Hungry House for £240m, regulatory concerns. Signs of reduced focus and competitive encroachment already abound at the enlarged group, regularly giving the City cold feet. This last happened as recently as January, when the group revealed annual orders rose 31% in its key UK market and 36% as a whole, compared with 50% and 57% respectively the year before.

It’s also notable that the group has transitioned from essentially a digital-only ‘orders reconciliation’ service into a full-on delivery group. Pressure from European rivals like Delivery Hero and Take Eat Easy is showing. Soon, that pressure will be scaled by upstarts like UberEats, Deliveroo and, in time probably Amazon. Just Eat’s claim to target the lower end of the market (£16 per delivery vs. £25-£30 at Deliveroo) is likely to be falsified as all rivals grow and grab.

Still, buyers and holders of the stock have been well-rewarded till now. The shares are up almost 90% since their April 2014 debut, even after slipping as much as 15% since January. A similarly bumpy ride is ahead, though Just Eat’s record of cash and profit growth is getting stronger.