June Month End Dollar Selling May be Dwarfed by Greek Drama

Background: Traders often refer the impact of ‘month end flows’ on different currency pairs during the last few days of the month. In essence, these […]

Background: Traders often refer the impact of ‘month end flows’ on different currency pairs during the last few days of the month. In essence, these […]

Background:

Traders often refer the impact of ‘month end flows’ on different currency pairs during the last few days of the month. In essence, these money ‘flows’ are caused by global fund managers and investors rebalancing their currency exposure based on market movements over the last month. For example, if the value of one country’s equity and bond markets increases, these fund managers typically look to sell or hedge their now-elevated exposure to that country’s currency and rebalance their risk back to an underperforming country’s currency. More severe monthly changes in a country’s asset valuations lead to larger portfolio adjustments between different currencies.

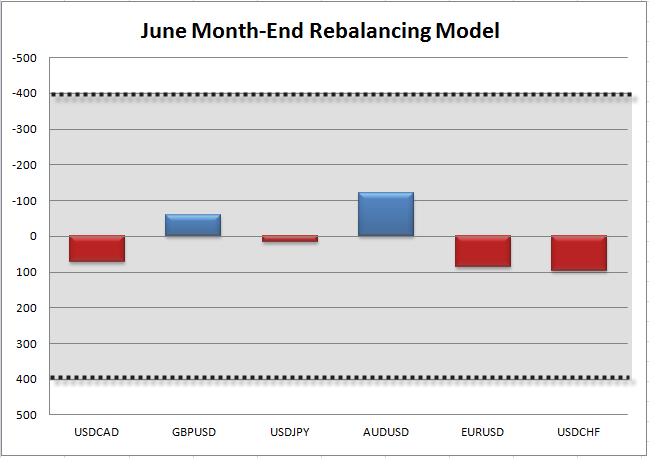

In order to predict these flows and how they impact FX traders, we’ve developed a model that compares monthly changes in the total value of asset markets in various countries. In our model, a relative shift of $400B between countries over the course of a month is seen as the threshold for a meaningful move, whereas monthly changes of less than $400B are often overwhelmed by other fundamental or technical factors. As a final note, the largest impact from month-end flows is typically seen heading into the 11am ET fix (often in the hour from 10 & 11am ET) on the final trading day of the month as portfolio managers scramble to hedge their overall portfolio ahead of the European market close.

With all the talk about Greece’s drop-dead date for reaching some type of debt agreement by June 30, it’s pretty hard to forget that the end of the month is just around the corner. And while traders the world over are far more interested in the latest headlines out of Greece, readers should also be aware of the potential for month-end flows to impact the market tomorrow.

It’s been a volatile month for global stock and bond markets, but for the most part, they’ve moved in sync with one another. US and European stock market indices pulled back by about 2% and 3% respectively on the month, though the UK’s FTSE index lagged its European rivals at -5%. Meanwhile, bonds fell across the board, with German’s 10-year bund yield pacing the gains by tacking on 31bps to 0.80%.

With most major equity and bond markets singing from the same hymn sheet this month, our model suggests minimal month-end rebalancing flow, with a slight bias toward US dollar selling. The biggest imbalance is in AUDUSD, but even that figure falls well below the +/- $400bn threshold for a significant move.

As of now, it looks like any month-end rebalancing flows may be overwhelmed by the ongoing Greek debt drama.

Source: City Index

Source: City Index