JPMorgan Wells Fargo shares dragged by mortgage hangover

The quarterly flood of so-called ‘bulge-bracket’ US bank earnings started on Tuesday afternoon, with Q2 results from JPMorgan, followed shortly afterwards by Wells Fargo. JPM […]

The quarterly flood of so-called ‘bulge-bracket’ US bank earnings started on Tuesday afternoon, with Q2 results from JPMorgan, followed shortly afterwards by Wells Fargo. JPM […]

The quarterly flood of so-called ‘bulge-bracket’ US bank earnings started on Tuesday afternoon, with Q2 results from JPMorgan, followed shortly afterwards by Wells Fargo.

JPM reported a revenue fall of 3.6% to $23.8bn in Q2 from $24.7bn in the same quarter a year earlier. On an ‘underlying’ basis—not including costs which the bank would classify as ‘one-offs’—the revenue result was $1bn lower than gross income in the year before.

JPM said the revenue slippage was the result of weakness in its Mortgage Banking and Corporate and Institutional Banking Markets divisions, as it continued its “business simplification” drive, though associated costs in the mortgage unit were partially offset by growth in Asset Management.

Either way, investors were set to give the shares a slight lift at the open, judging by pre-market price indications, but in the event its stock opened slightly lower, before going on to dither above and below the flat line within the first half hour of the session.

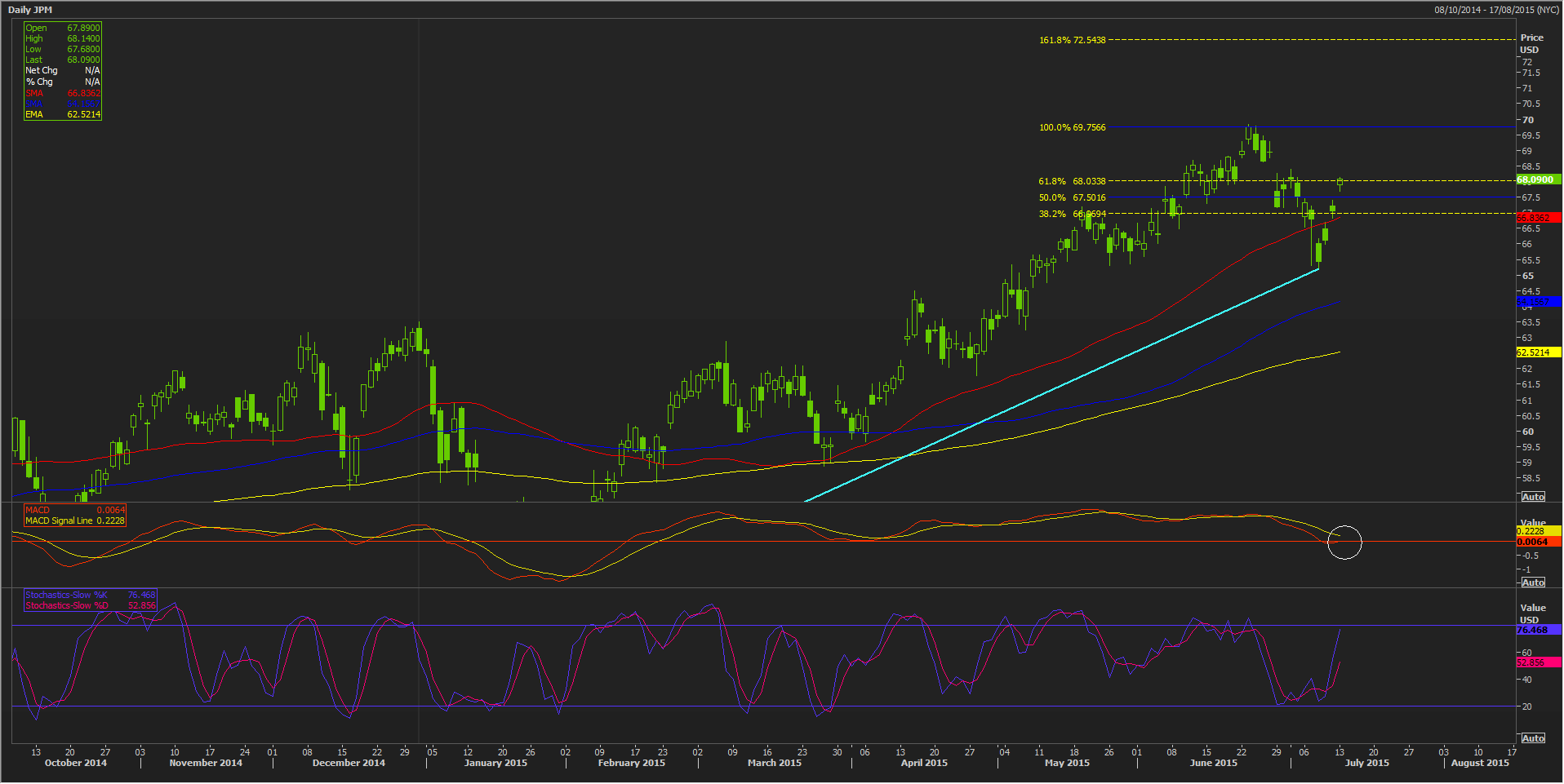

The stock looked visibly well-supported, well above the uptrend that began in February, and also higher than all major moving averages, even though moving average convergence divergence (MACD) and stochastic indicators were more ambivalent.

Whilst in the former (first sub-chart; yellow and red lines) the ‘faster’ moving average (MA) was pointing moderately lower, the MACD itself was pushing above the ‘zero’ balance, suggesting a stronger impetus from buying—that would be confirmed if this red line broke above zero.

The ‘Slow Stochastic’ indicator was close to the upper bound but the faster MA continued to lag whilst inverted upwards, suggesting buying would probably carry the stock through the near-to-medium term.

One proviso was that retracements drawn off JPM’s rise from late-May lows suggested the stock was butting up against a powerful level—whilst Tuesday’s pre-opening orders showed investor enthusiasm was only moderate.

Please click image to enlarge

Mortgage demand turned out to be an important focus for investors in assessing Wells Fargo revenues, given that weak demand had restricted its growth in that business for a few years.

Whilst earnings from this crucial unit for America’s fourth-largest banking group showed signs of recovery, with a $158m rise quarter-on-quarter in mortgage banking non-interest income, unlike for JPM, investors looked set to give WFC the thumbs down at the US market open.

This was at least partly due to an apparent decline in earnings quality as judged by reported Return on Equity which fell almost half a percentage point to 12.71% quarter-on-quarter.

And even with the uptick in mortgages, Wells still reported an overall drop in profit for the second quarter in a row as provisions for bad loans and other expenses rose, taking out $60m in net income compared to the $5.42bn it reported in the second quarter to the end of June last year.

The bank’s non-interest expenses rose 2.3% to $12.47bn, accounting for about 58.5% of revenue, whilst it had intended to bring expenses down to 55%-59% of revenue.

EPS ticked higher by two cents to $1.03 year-on-year, but this was down to the removal of stock from issue; some of this was due to an on-going return of cash to investors which will pull in 240 million shares in 2015.

The stock closed on Monday at 56.74 and pre-market quotes showed the stock could open as much as 74 cents lower.

In fact WFC did open slightly weaker, before trading a few cents higher on the day–investors didn’t seem particularly impressed with its results.

Wells’ stock has lagged that of its peers badly over the last year, with a rise of just 3.5% in the second quarter, compared to shares of other Wall Street banks which have gained 7%-12% in the latter period.

JPM is up 21% over the last year, whilst WFC is up about 11%.

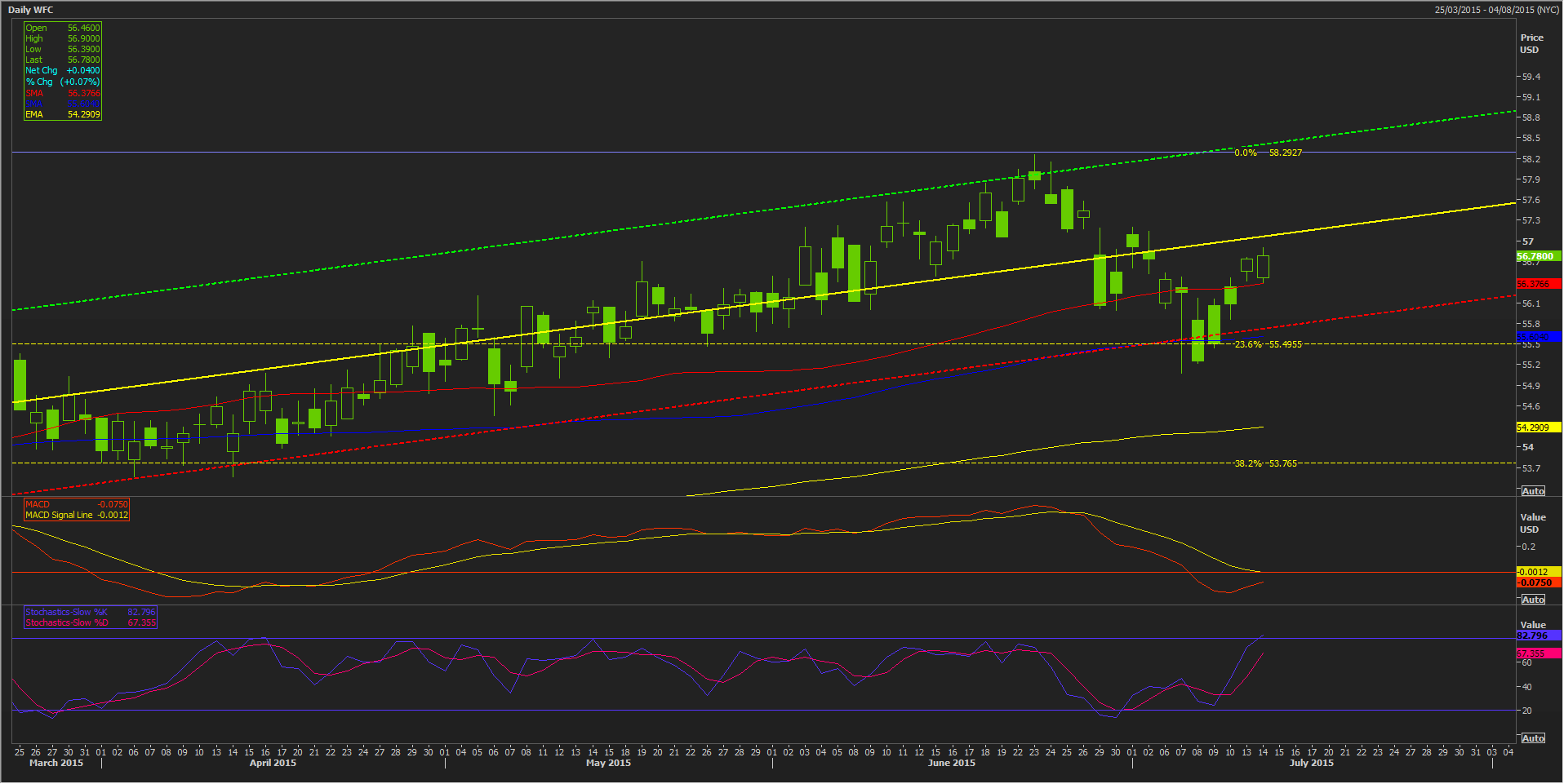

Despite the wary pre-market activity, signs of underlying strength were still apparent in Wells stock.

A relatively weak retracement marker related to the rise from October 2014 low to the current 2015 peak, combined with WFC’s 100-day moving average, provided delayed support last week.

However the midpoint of a regression channel that currently sits close to $57 may be the current limit for the stock on the upside.

Please click image to enlarge

Shares of the largest North American lenders have been in even tighter focus in the last few days amid events in Greece and China.

Their shares rose after Monday’s news that Greece capitulated to tough conditions with creditors, whilst China’s recent stock market tumble of more than 30% over the space of a week also stoked worries that the global impact might give the Fed a reason to lengthen its timeline to a rate rise.

Bank of America earnings will follow on Wednesday and Citigroup’s and Goldman Sachs’ on Thursday.

This article will be updated later on Tuesday