Jobless uptick messes up sterling 8217 s week again

The pound has continued to ail on Wednesday as traders focus on the most up-to-date parts of the day’s UK employment update.

The pound has continued to ail on Wednesday as traders focus on the most up-to-date parts of the day’s UK employment update.

This has clipped sterling’s recovering wings yet again, sending the pound against the dollar away from $1.25 after the rate managed to claw its way as high as $1.2492 earlier.

This vacillating and nervy market reaction reflects the view that whilst the quarterly ILO jobless total fell 37,000 to 1.604 million, an 11-year low, more sensitive gauges of the labour market like the Labour Force Survey showed the pace of new job additions slackened back to rates seen in earlier and more uncertain months of the year.

A faster rate of ‘signing on’ than expected, and the highest since the month before the Brexit vote, also caught the market’s eye.

Coming on top of Tuesday’s price inflation data, where the emphasis was squarely on upward price pressure on producers, the recent tail-off in hiring may be pointing to a return to the anxious slowdown in business activity seen earlier in the year.

At the same time though, underlying pay increases met expectations with a rise of 2.4% year-on-year in September, whilst most of the other pay data filters were also firm, apart from public sector figures.

As ever, one set of data doesn’t make a trend, particularly in a year of such economic volatility as this one. And whilst any real softening of the jobs market could be confirmed next month, we are also entering the period where seasonal effects often begin.

Either way, ample ambiguity will remain in the jobs outlook for some months, as it will in other parts of the economy. During that time, sterling’s mean reversion will almost certainly be extended.

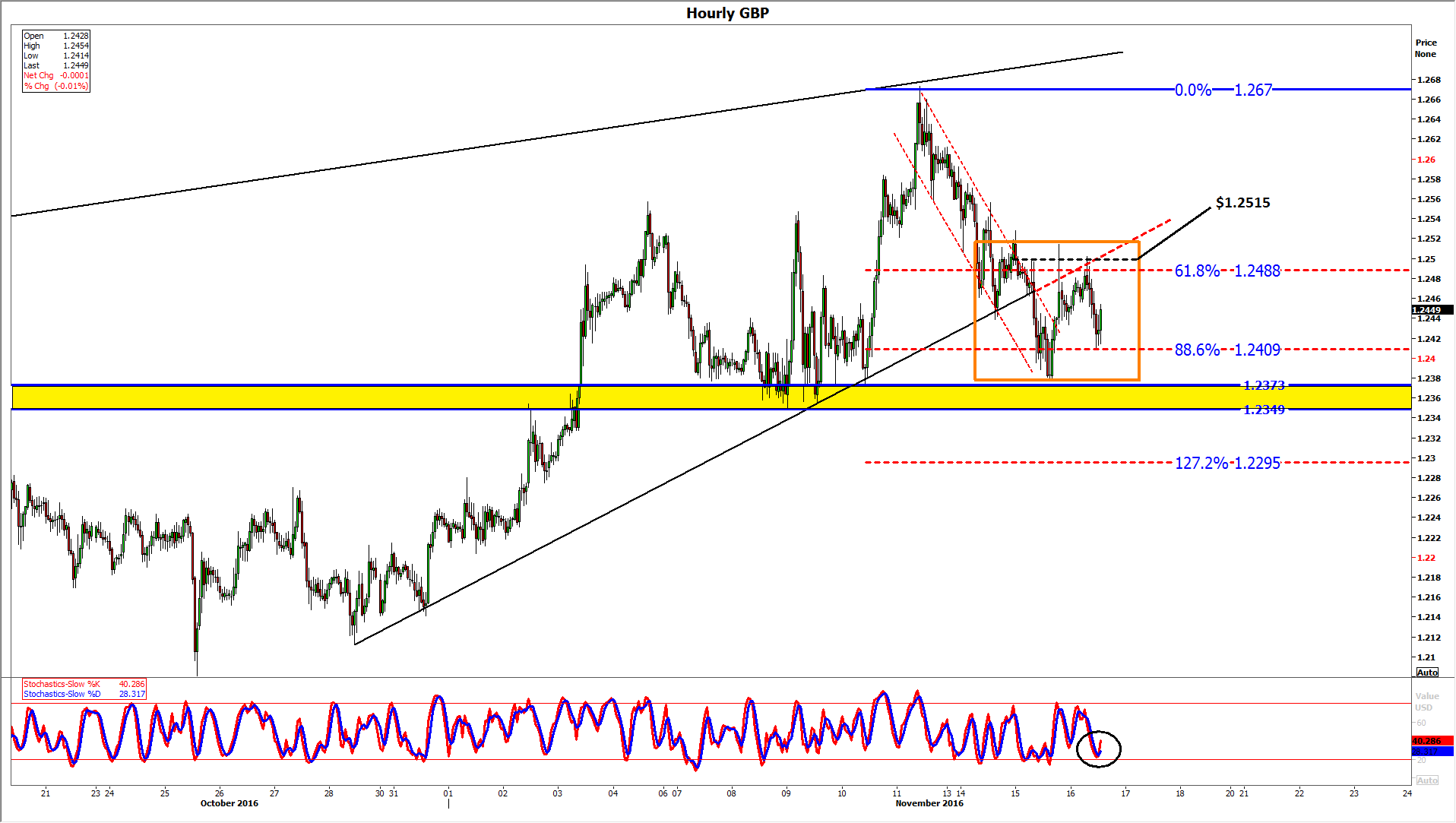

The good news for sterling bulls from recent price action is that GBP/USD has swerved out of a short-term descending channel, breaking the sharp decline off the month’s highs (so far?) around $1.267 which followed the Trump election shock.

The bad news is that the downleg also broke under the rate’s recent ascent from October’s lows (c. $1.2081) and pretty much obviated the ’rounded bottom’ pattern visible between early September and November highs.

Certainly, we would not expect medium-term bulls to begin showing interest before the rate breaks above the troublesome and volatile region seen this week between $1.2498 and $1.2380.

We suspect there may be an ‘order block’ surrounding price action of a candle nestling at 00.00 hours on Tuesday morning, when the rate closed at $1.2515. In keeping with the order block concept, the candle was the last higher period-period close before the down move commenced, hence a potential nook holding slow-release institutional orders.

Currently support appears to be forming at 88.6% (a Fibonacci interval) of the 10th-11th November surge to those $1.267 highs, though extension down to $1.2373 can’t be ruled out with any confidence right now.

A bid from the 88.6% notch ($1.2409) was in effect as I wrote this (taking advantage of the momentum swing—see Slow Stochastic Oscillator turning higher from lower boundary though it was not oversold).

The range between $1.2488 (61.8% of this week’s slide) and $1.2515 looks like a reasonable target, for those on board.

Please click image to enlarge