Job Flow vs 2007 amp USDJPY Perfect Storm

There are obvious usual positives from today’s release of the US February jobs report: 7.7% unemployment being the lowest since Dec 2008; non-farm payrolls beating […]

There are obvious usual positives from today’s release of the US February jobs report: 7.7% unemployment being the lowest since Dec 2008; non-farm payrolls beating […]

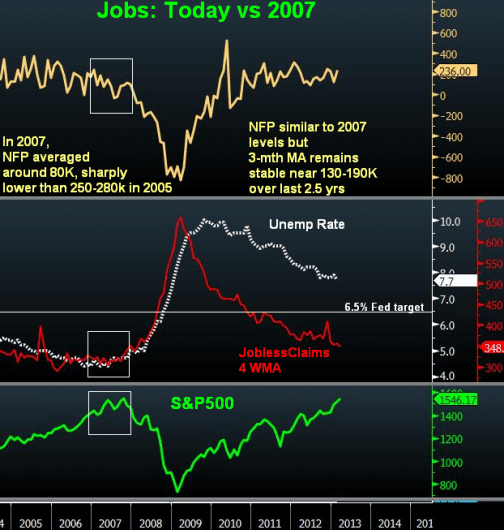

There are obvious usual positives from today’s release of the US February jobs report: 7.7% unemployment being the lowest since Dec 2008; non-farm payrolls beating expectations by 80K to 236K, showing the 2nd monthly reading about 200K over the last months. But what about comparing job markets to 2007?

Comparing Jobs to 2007

Since equity indices are at or close their 2007 highs, let’s compare the current employment metrics to 2007.

The charts below indicate the following:

1. Non-farm payrolls stand around the same levels of +200-300K seen in summer 2007, but the two glaring differences are that the current 3-month average has remained stable near the 130K-190K range over the last 2 years, while the 3-month average in 2007 stood near 80K, well below the 250K-280K range prevailing between 2005 and 2007. This illustrates that the ascent in job creation over the last 2 years is clearly superior to that when equities had peaked in 2007, suggesting the rising trend could feed into higher personal expenditure and corporate margins.

2. The unemployment rate of 6.5% compares to 4.5%-4.9% in 2007, while jobless claims (4-week MA) stand at 348K versus 305K-320K. Note how the declining cycle leading to the 2007 lows in jobless indicators had lasted 4 years (following the cycle peak in 2003). While jobless claims remain close to their 2006 lows, the unemployment rate has greater scope for decline. This is best illustrated via the underemployment rate, which stands at 14.3%, compared to 8.0%-8.5% in 2007, but well below the 2010 high of 17.3%. A trend which merits scrutiny is the extent to which US jobless claims will continue their ongoing decline (as they near their 2007 lows), until dragging unemployment further for longer than 4 years.

3. Sector jobs breakdown are more solid in 2007. Retail jobs have not had a net-monthly loss since June, creating a net increase of 200K in the last 8 months. This compares to 2007 when retail jobs had weaker jobs creation during the year as well as frequent net monthly losses. In manufacturing, the 3-month moving average currently stands at 14K, compared to a range of -15K to -30K in 2007. Not only the 2007 plateauing in manufacturing was spread at far lower levels, but it lasted for about 2 years.

The aforementioned comparisons illustrate a healthier flow (rate of change) in US labor markets compared to 2007 despite weaker stock (absolute figures) such as higher unemployment and jobless claims. And with the DJIA as the only index of the 7 major global indices at record highs, he scope for further gains become more convincing.

Perfect Storm in USDJPY

USDJPY hit a fresh 4-year high at 96.56 trading as the perfect storm, propped by : i) full-fledged anti-deflation Japanese policy; ii) improving US growth dynamics; and iii) broadening global risk appetite further weighing on the yen. USDJPY soared to new 4-year highs throughout the last 24 hours on better than expected US services ISM and fresh declines in US jobless claims, before further declining on comments from Japanese Fin Min Taro Aso who said he did not discuss the JPY with his US counterpart Lew and that yen weakness was a result of Japan’s campaign to fight deflation. Fears of an overbought trend were tempered by the fact that the pair had already shown consolidation in lat Jan- mid Feb, followed by a sharp decline in Feb 25. But more of the same continued. Reflationary monetary policy receives a weekly affirmation by the Prime Minsiter, Minustry of Finance and the newly appointed governor of the Bank of Japan (as well as his 2 deputies),. The perfect storm is here to stay until 97.50 acts as a temporary barrier. 102.00 USDJPY remains viable well before Upper House elections in July.