February 16, 2020 11:15 PM

A quiet start to the week in the Asian time zone with traders seeming content to sit on their hands ahead of Presidents Day holiday in the U.S. and Family Day holiday in Canada tonight. Content also to mostly look through GDP data in Japan that showed the Japanese economy shrank by an annualised 6.3% in the fourth quarter of 2019.

Due to the impact of a sales tax hike in October and a devastating typhoon, the expectation was for a contraction, however, todays fall was much steeper than expected. When taking into account the threat to activity data from coronavirus in the current quarter, mainly via tourism and exports, the Japanese economy is in danger or recording two consecutive quarters of negative growth. Thereby meeting the technical definition of a recession for the first time since 2015.

In days gone by, today's GDP would have provoked a sharp response across Japanese financial markets. Apart from modest falls in the Topix and Nikkei stock indices, USD/JPY and JGB’s remained becalmed comforted by an expectation todays GDP fall, increases the chance of more stimulus.

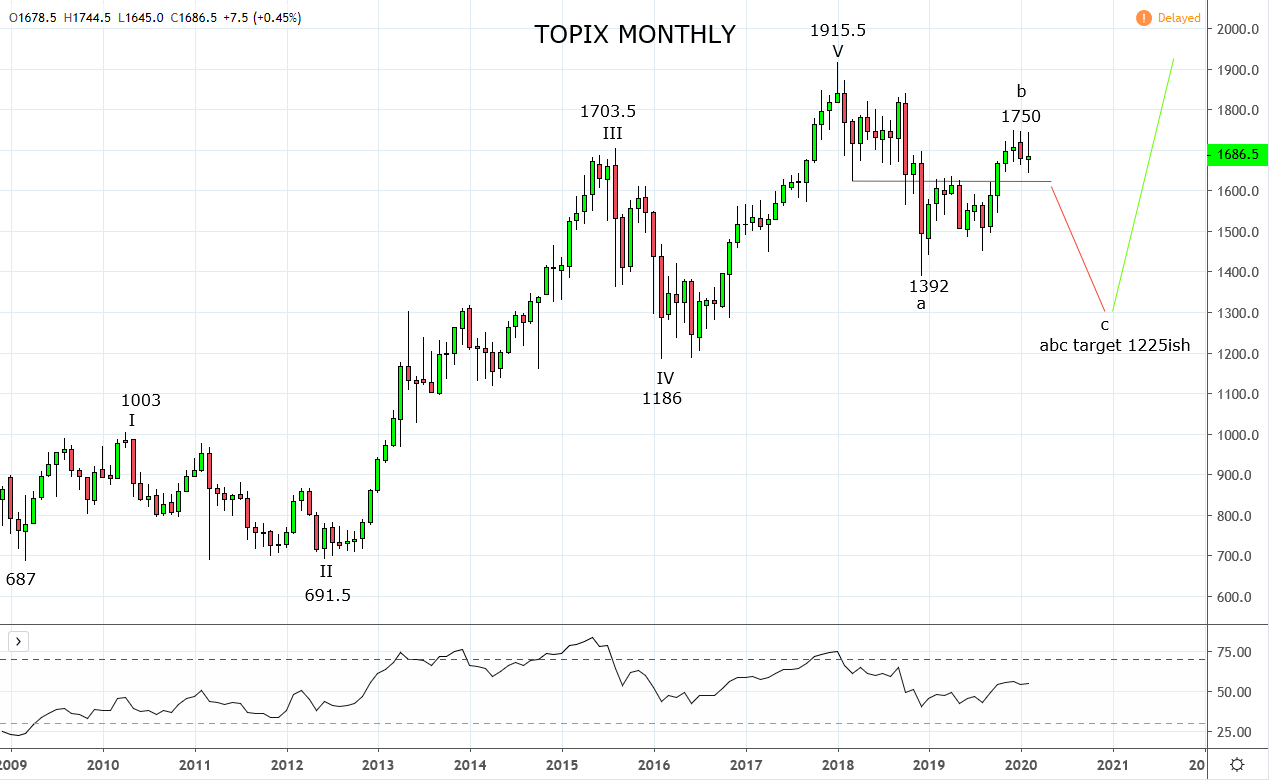

There is certainly a degree of truth in this. However, there is a genuine concern among market participants that another round of easing/stimulus from the Japanese government, will do more harm than good. The monthly chart of the Topix below goes some way to validating this concern.

The rally from the Global Financial Crisis low of 687 to the 2018, 1915.5 high unfolded in a textbook Elliott Wave five waves, after which the Topix commenced a correction. The most common type of correction is a three-wave zig-zagging correction. The current correction appears incomplete and missing a final leg lower.

Providing the Topix remains below the recent triple high 1750, the risks are for a move towards the wave equality target at 1225ish to complete Wave c of its correction. I would suggest using a break/close below support at 1620 to suggest the aforementioned big picture move is underway.

Source Tradingview. The figures stated areas of the 17th of February 2020. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Japan articles

April 11, 2024 11:15 PM

February 27, 2024 12:54 AM

February 21, 2024 06:12 AM

February 10, 2024 09:00 AM