Japan shares eye BOJ after worst quarter for 5 years

Japanese stocks are likely to be scrutinised for further signs of weakness in the near term, after closing out their worst quarter for five years. […]

Japanese stocks are likely to be scrutinised for further signs of weakness in the near term, after closing out their worst quarter for five years. […]

Japanese stocks are likely to be scrutinised for further signs of weakness in the near term, after closing out their worst quarter for five years.

Japan’s benchmark Nikkei 225 stock index rose 1.9% on Thursday, adding to a 3% rise a day before, aided by Chinese manufacturing data that showed signs of bottoming out.

Economic readings from Japan itself also helped revive sentiment, after a manufacturing gauge declined only marginally, whilst highlighting a rise in orders.

However, the Nikkei 225 was still far from recouping a 14% slide in the fiscal quarter ending 30th September, its deepest quarterly drop since 2010.

A confluence of well-known bearish factors contributed to global sell-offs in the last two months, including tumbling commodity prices, China’s slowdown, and high-profile corporate turmoil.

It looks like Japan may have faced a higher order of risk aversion as the world’s economic wobble coincided with a reckoning for its own economy.

The Bank of Japan, which has pumped Y180 trillion into the economy since embarking on a huge unconventional stimulus programme, is reportedly having a re-think.

The BoJ’s quantitative and so-called ‘qualitative’ easing (QQE) began in 2013.

It burns through government bonds equivalent to 1% of Japan’s GDP each month.

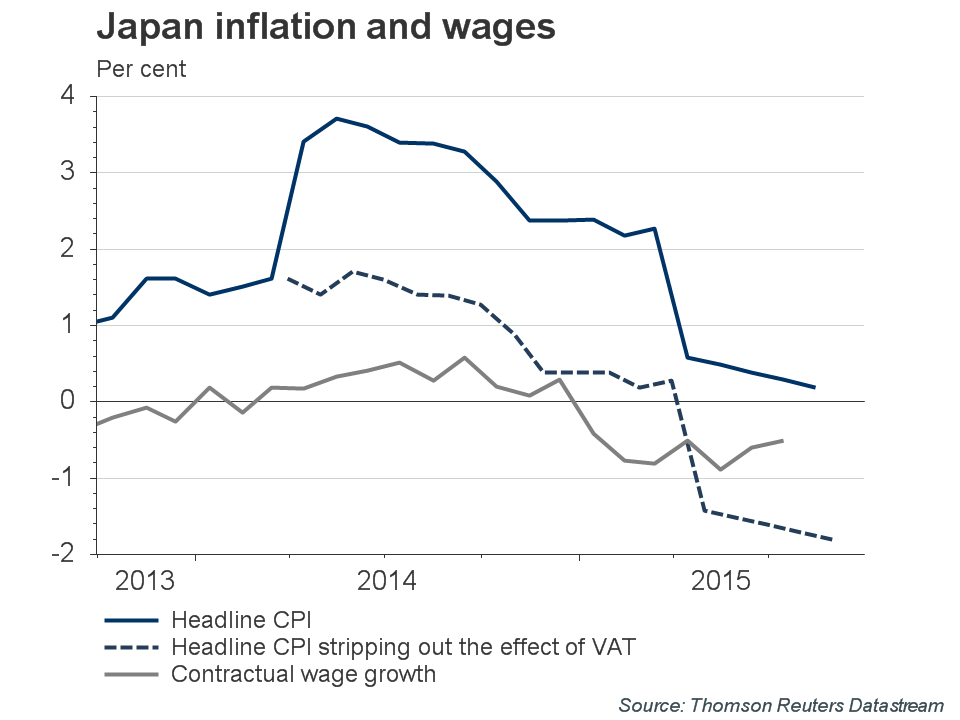

However after Japanese inflation peaked near 4% almost 18 months ago, it has fallen ever since.

The BoJ’s Y80 trillion ($665 billion) per year economic intensive care has inflated exporters’ profits by weakening the yen.

But its wider impact has been limited, with firms apparently wary of increasing wages and investment.

Last month, unconfirmed news reports suggested the central bank might not extend the programme, given its failure to sustainably boost inflation above a 2% target.

The BoJ already holds about a quarter of Japanese government bonds (JGB) in the market.

That would rise to nearly 40% by the end of 2016 at its current pace of buying, bringing risk that sellers may run out.

Still, the BoJ’s official line remains that it can keep buying government bonds for several more years.

It has other options too, including cancelling a 0.1% interest rate on banks’ reserves, perhaps in combination with buys of riskier assets.

Such speculation and doubts can only fuel stock market volatility, especially with the next BoJ announcement due on 7th October.

Surveys and interest rate futures suggest markets only attribute a 1-in-3 chance of stepped up BoJ easing.

That comes amid signs of the first net short position in the key USD/JPY cross, since QQE began.

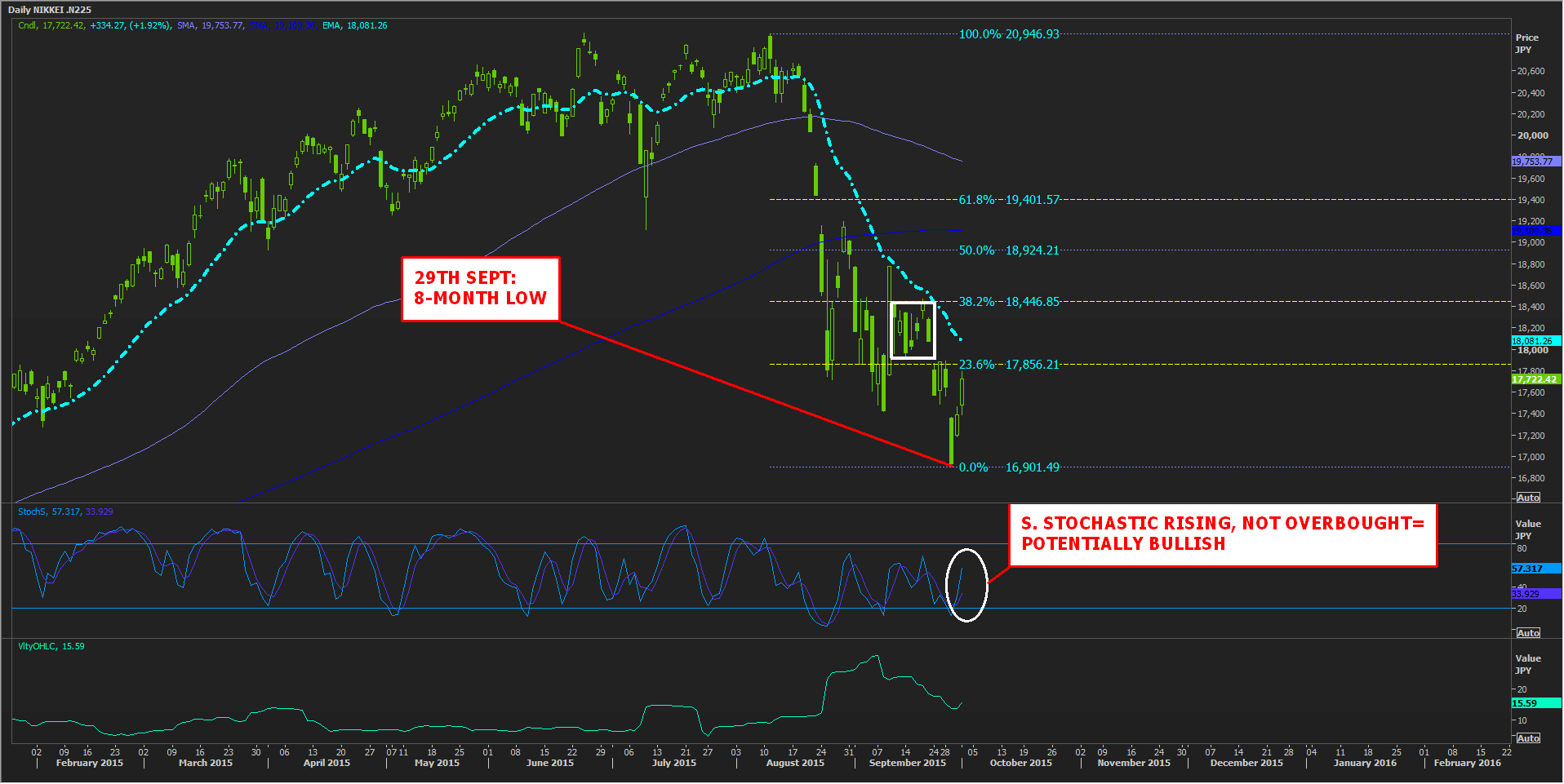

As for Japan’s main Nikkei stock index, a key short-term test is whether it can get above its 21-day exponential moving average (EMA), currently at 18081, after touching 8-month lows this week.

Please click to enlarge

The closely-eyed 21-day EMA is favoured for short-term charts as it has less lag.

It straddles anticipated resistance between 17965 and 18468.

In the meantime, momentum studies (like the Slow Stochastic Indicator, pictured) show improving sentiment has room to run further, though that’s not guaranteed.

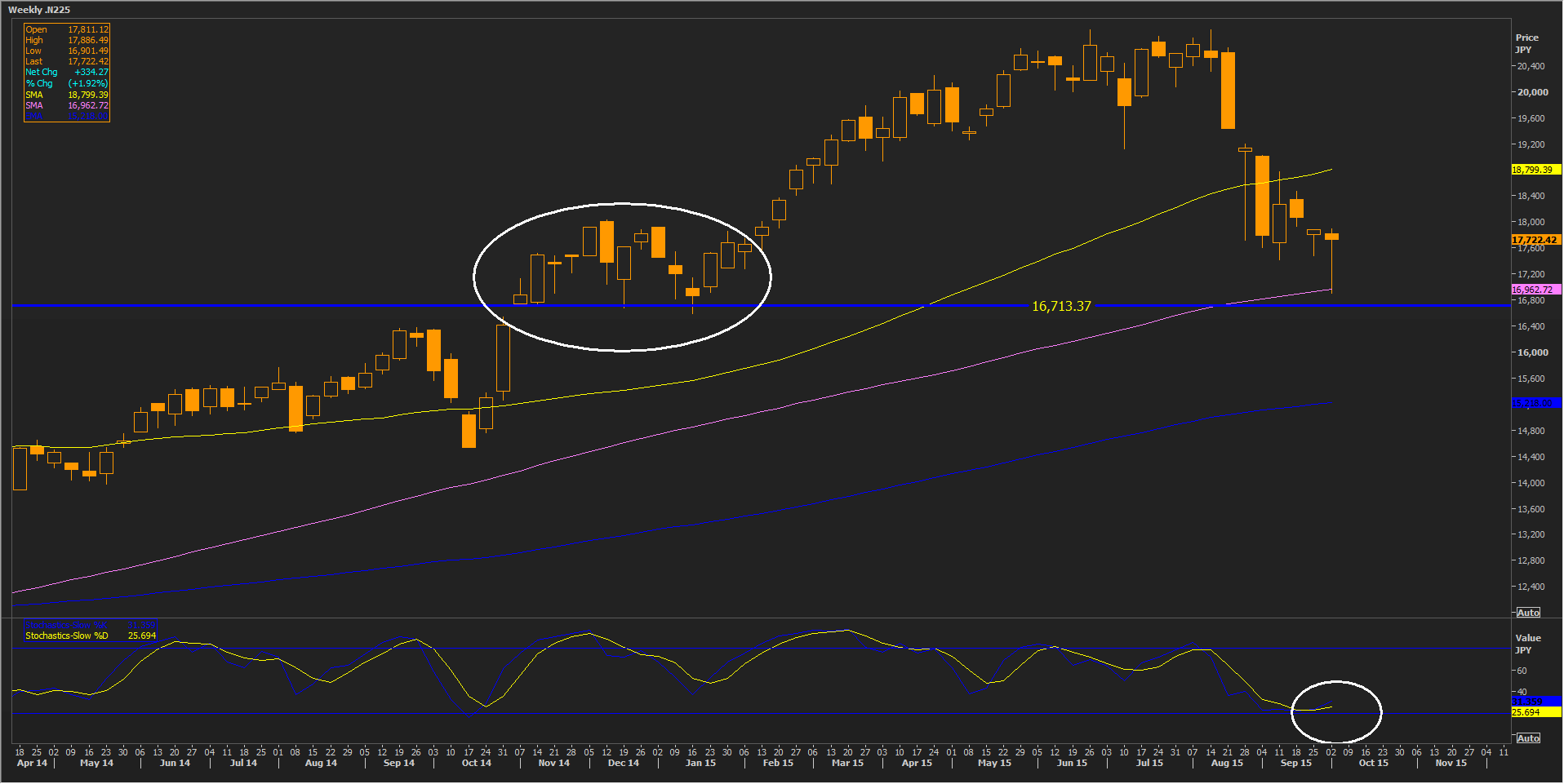

In a weekly view, the N225 is testing its 100-week MA, above 16710-16800 support from November 2014 to January 2015.

Please click image to enlarge