ITV shares await liberation

A steady-as-she-goes interim update from ITV was deemed satisfactory by investors, helping the shares rise off a 0.7% early-morning loss to a gain of 2%. […]

A steady-as-she-goes interim update from ITV was deemed satisfactory by investors, helping the shares rise off a 0.7% early-morning loss to a gain of 2%. […]

A steady-as-she-goes interim update from ITV was deemed satisfactory by investors, helping the shares rise off a 0.7% early-morning loss to a gain of 2%.

No arguing with the solidity of ITV’s cash streams, during the third quarter:

And key television metrics are also trending in the right direction:

o seen +1% in November

o +1%-3% in December

o 1%-2% for Q4

o FY seen +5%

If achieved, the complete-year revenue rise would be well ahead of the average for the UK TV market.

What more could a broadcast investor wish for?

Well, we think they could wish for quite a bit more.

After all, ITV Plc.’s prospective dividend yield of 3.1% fairly pales in comparison with its main listed broadcasting peer, Sky with the latter on 4.12% against ITV’s 2.10%.

We think there is a degree of dividend anticipation among investors regarding the ITV yield.

The compound annual growth rate for dividends could be 13%, looking at consensus forecasts for this year and the next four (although forecast growth for 2014 is as much 21%).

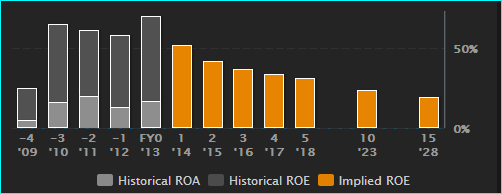

Return on equity (ROE) is currently at just under 39% at ITV whilst Sky is returning 83%.

ITV ROE should flatten from its crises-to-recovery gradient and trend lower.

Source: Thomson Reuters

We also query the price-to-earnings ratios that remain around 14-15 times within a fiscal 2013-2015 time frame.

It looks like some bid interest remains in the stock price, even though there have been none of the elliptical references to US cable giant Liberty Media of the summer for months (and no mention today).

The only operational figures which scream of surging growth are the digital ones, and these do not appear to be a major priority, yet, for CEO Adam Crozier, who made it clear he would focus this year on continuing to right-the-ship, whilst laying the ground work for growth.

Audience shares for the all channels seem close to five-year lows, despite their firmness.

Meanwhile, Sky’s consolidation into a larger European broadcaster (completed today) fortifies its cash flows, placing it on a better footing to tackle an increasingly consolidated broadcasting landscape by means of combined marketing spend and amalgamated purchasing power.

The best hope for continued profit growth comes from the prospect of another step in liberalisation: that ITV could begin charging for the shows it now gives to BSkyB and Virgin for free under its British public obligation.

Ofcom launched its latest review into public service broadcasting in May. It’s expected to run well into the autumn. A public consultation will follow, ending in the spring.

In the meantime, the stock will continue to act ambivalently—unless the return of real bid interest is confirmed.

Worth bearing in mind that highly-indebted Liberty became less acquisitive than usual this summer after debt agency Moody’s chided the Virgin Media owner for a set of relationships with media companies with “no material upside”.