Italy decides will it be Armageddon for European markets

Context Potential outcomes and how financial markets could react Trading Opportunities 1, Context This Sunday, 4th December, Italy will vote in a yes/ no […]

Context Potential outcomes and how financial markets could react Trading Opportunities 1, Context This Sunday, 4th December, Italy will vote in a yes/ no […]

1, Context

This Sunday, 4th December, Italy will vote in a yes/ no referendum on proposed constitutional changes proposed by Prime Minister Matteo Renzi. The polls close at 2200 GMT, with the exit polls expected to be released soon after. The first state results should be released by 2300 GMT, and the official result is expected to be called around 0500-0600 GMT on Monday 5th December.

Italy has banned any polls since November 18th, when it appeared that the No campaign was in the lead. However, it is worth noting that there was a high percentage of undecided voters, approx. 30%, which could skew the results. Our source on the ground in Rome urges caution in assuming that the No camp will win on Sunday, saying that 5% of Italy’s voters are foreign residents, who haven’t been included in the polls and may be more likely to vote Yes in the referendum. They also noted that there could be some “silent” Renzi voters, who won’t admit that they will vote Yes on Sunday, due to a general feeling that he has been a disappointing PM for Italy.

So, with only a few days to go before the vote, the markets have little certainty over which side will prove victorious on Sunday. The opacity of this vote has triggered some angst in financial markets, there has been some panic in equity markets, particularly in European banking stocks, as we lead up to the referendum, and we have seen a spike in the Italian – German bond yield spread, although Italian bond yields have backed off from recent highs, and have not yet surged to levels seen during the sovereign debt crisis, when Italian yields jumped to 7% back in 2012.

2, Potential outcomes and how financial markets could react

So, are the markets under-pricing the risk from this referendum, and does it matter for markets? Considering the political shocks that have been delivered in 2016 already, we think the markets would be wise to keep a close eye on Sunday’s referendum outcome. Two things matter for markets, in our view:

1, The No camp wins and this causes the collapse of the current government. If a government cannot be formed then this could trigger an election, which may give the anti-establishment Five Star Movement Party some momentum to secure a larger majority in the Italian parliament. This may trigger a wave of market volatility due to the Five Star Movement’s anti-EU stance in the past.

2, The banking sector: Italian banks are in terrible shape, and had been subject to a bailout plan agreed by Renzi’s government. If he loses the referendum and resigns, then the big question for traders will be if the bailout plan still stands. If not, then eight of Italy’s lenders could be at risk of collapse. Due to the interconnectedness of the global banking system, and the weakness of some other European lenders notably Deutsche Bank, a collapse in Italy’s banking system could lead to intense pressure on global financial stocks in the aftermath of a No vote.

A win for the Yes camp, could trigger a sigh of relief for the markets, particularly for Italian bond yields, which we would expect to retreat back to the 1% mark, where they were back in August, they are currently just under 2%. We would also expect a large rebound in Europe’s banking shares, particularly Unicredit and Banco Monte dei Paschi di Siena SpA. These banks, in particular, could benefit from a win for the Yes camp as it could facilitate a rapid share pricing for these banks early in 2017.

Is a win for the No camp really that bad?

Even if the No camp wins on Sunday, the market could initially misinterpret the result just as we saw with Trump’s victory in the US, for three reasons:

1, Just because the Italian people vote No doesn’t mean that they don’t want change, in fact it could signal that they want a new more reform-minded government than Renzi, especially if a No vote triggers a general election.

2, Even if the Five Star Movement wins power under a hypothetical election post the referendum, this does not mean that Italy will leave the EU. Italy’s constitution does not allow referendums on international treaties, which could put some investors’ minds at rest.

3, The Italian finance minister warned that a win for the No camp would not necessarily mean that Italy’s banks would be at risk, as the bailout plan could still go ahead. When it comes to Italian banks, no matter who wins on Sunday, they have a period of painful readjustment ahead.

We would expect further soothing words from Italian and EU officials if there is a win for the No camp next week, which could dampen any spike in volatility on the back of this referendum.

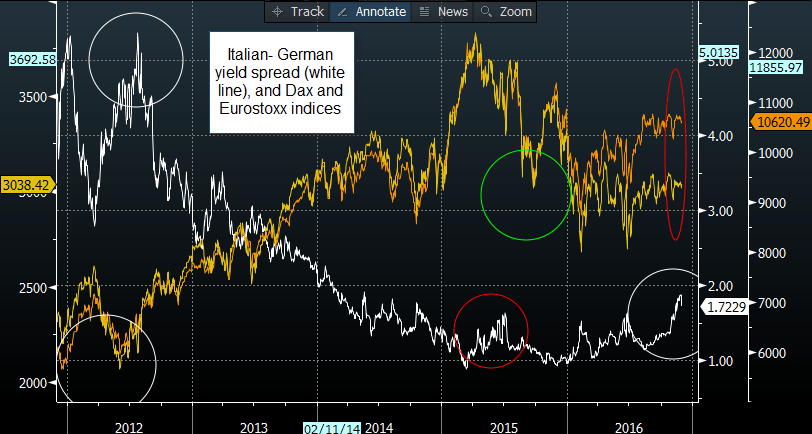

What the Italian – German yield spread could tell us about equities

In terms of market action, the chart below is a good indication of how markets could react to any referendum-inspired spike in Italian bond yields. The chart below shows the Italian – German 10-year sovereign yield spread, the Dax and the Eurostoxx index. Since 2012, the Dax and the Eurostoxx index have suffered sharp falls when this yield spread has spiked. This happened again when the yield spread started to wobble in 2015. In recent weeks, as the yield spread has risen to its highest level since 2014, European stock markets have started to wobble although they have not fallen off a cliff

Although historical price action does not predict what may happen in the future, one could assume that the same may happen after a win for the No camp on Sunday/ Monday, with a spike in the Italian – German yield spread triggering a decline in Europe’s two major stock indices. Below we go into more detail about specific trading opportunities.

Figure 1:

Source: City Index and Bloomberg

3, Potential Trading Opportunities (by Ken Odeluga)

An extraordinary year in global politics has meted out some hard lessons to investors. One flippant one, albeit with more than a grain of truth might be ‘take the polls with a pinch of salt’, and perhaps more seriously: ‘prepare for the sell-off and for the bounce’.

Ironically, in 2016’s third potential anti-establishment political ‘shock’, Italy’s referendum on constitutional reform, the first lesson points to a different outcome than at the Brexit vote and U.S. election. It is the most obvious of several nuances in the plebiscite on proposals by the country’s Prime Minister Matteo Renzi.

Broadly speaking, it therefore makes sense for market participants to take a somewhat different view of the risks and potential rewards linked to Referendum Costituzionale too. To be sure, Renzi’s days as PM will still probably be few, once Sunday’s poll is tallied, by Monday afternoon, latest. Note he has recently reiterated earlier pledges to resign if his plan is rejected.

Back to the pollsters: big opinion polling groups in Italy have almost unanimously abandoned the extreme caution they were expressing just days ago about the referendum result, underlining how surveys came unstuck over Trump’s victory and in the June ‘Brexit’ referendum. Now, most say the size and consistency of the lead for ‘No’ is not comparable with either the U.S. election or Brexit, and it would take an unforeseen event, or another remarkable surprise, for Renzi to win.

But this raises another head-scratcher. With pessimism over Renzi’s chances now so widespread, will a ‘no’ outcome be a surprise for the market? The country’s benchmark stock index is already among the worst performing developed markets this year, with a near 23% fall that even exceeds the 14.4% slump of Europe’s banking sector, weighed most heavily by Italian banks. More widely, Europe’s broad STOXX index is within 20 points of the year’s lows and the euro actually mere cents from the same versus the dollar.

All this suggests that market nerves are well baked into prices already, regardless of the outcome. This particular article doesn’t have the scope to discuss scenarios in detail, but, a ‘No’, will probably lead to the formation of a new government. The colour of the new administration will resemble Renzi’s if his coalition partners support a new pick for PM by Italy’s President.

For now, with one of Italy’s rather common short-term governments looking like the probable outcome if Renzi is forced to resign, we would expect a single-digit sell-off of large European markets on the day to be followed, by the end of next week, by a stabilisation in European stock prices.

We would expect Germany’s DAX to once again reflect hypersensitivity to European political risk with a fall of no more than 5% on Monday 5th December following a ‘No’ vote. Recovery should track progress of tidying up Italy’s latest government collapse, if seen. Other European stock markets will also be volatile, particularly France’s CAC-40, as the establishment there will be the next to face a political reckoning in spring 2017. We would expect an already OPEC-weakened FTSE 100 to also be pressured.

However, the FTSE should also be tilted higher more quickly, due to the likely extended weakness of the euro against the dollar and its ties to mining and oil denominated in a stronger than usual dollar.

In terms of the euro, we think that EURJPY is at risk of a sharp sell off in the event of a win for the No camp. This pair has tested the 200-day moving average support at 118.58 in the lead up to this referendum. A negative shock could trigger an initial decline back to 114.94 – the 100-day sma. We believe that the major euro crosses could also be at risk. If a win for the No camp triggers further accommodative action from the ECB, then we may see a return to parity for EUR/USD. In contrast, we would expect a modest rally for the major euro pairs if the Yes camp is victorious on Sunday.