Is this the end for easy money

This week has been illuminating for a number of reasons. We know that the UK PM Theresa May will trigger Article 50 by March, which […]

This week has been illuminating for a number of reasons. We know that the UK PM Theresa May will trigger Article 50 by March, which […]

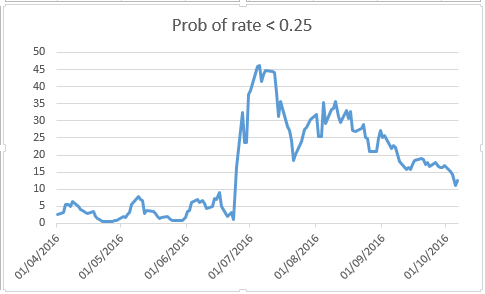

This week has been illuminating for a number of reasons. We know that the UK PM Theresa May will trigger Article 50 by March, which has unleashed another wave of pound selling as Hard Brexit paranoia stalks the markets. Perhaps more important for the long term trends in the financial markets has been a slight, but significant, shift in global monetary policy, which could see less monetary easing from the major central banks’ than we thought. Fed rates could be a done deal if NFP plays ball A rate hike from the Fed in December has been on the cards for some time. After Wednesday’s stunning non-manufacturing ISM, which saw gains across the board, the market goes into Friday’s NFP report with great expectations. The probability of a rate hike from the Fed at its December meeting (as measured by the Fed Funds Futures rate), has risen to 62% from 54% a week ago. Two months ago the expectations for a rate hike were below 50%. Of course, this could all go pear-shaped if the NFP report disappoints expectations on Friday, but for now we are living in a world where the market is prepped for higher interest rates at the world’s most influential central bank. Could the BOE put the brakes on QE? On the other end of the spectrum is the UK. The Bank of England cut interest rates and expanded its QE programme in the aftermath of the Brexit vote, but since then the economic data has proved to be more resilient than the Bank expected. Numerous BOE officials have stated in recent weeks that there may not be a need to cut rates further or expand the QE programme. While this has failed to stem the pound’s decline, it has been reflected in the UK interest rate swaps market, where expectations for a cut at next month’s meeting have fallen to a mere 12%, a month ago the probability of a cut stood at more than 20%. The ECB joins the band wagon The other central bank news this week included comments that the ECB is nearing consensus on tapering its QE programme early. While nothing has been confirmed at this stage, today’s release of minutes from the last ECB meeting could shed light on whether a consensus to end QE is starting to build. This has also been reflected in the European interest rate swaps market, the probability of a rate cut in the Eurozone at its meeting this month has fallen to a mere 7% from 12% a week ago. The probability of a rate cut at the December meeting is down to 20%, from 44% a month ago. Could falling levels of liquidity hit global stock markets? In recent months the markets have been comfortable with the notion that the US will hike rates first, and the BOE, ECB and even the BOJ will keep monetary policy loose. Thus, even if the Fed tightens rates, markets will continue to benefit from the liquidity coming from other central banks. Developments this week throws into doubt the prospect of unending central bank liquidity. This could be bad news for risky assets including stocks, in particular those like the FTSE 100, which is approaching a record high. Rising oil prices buoy stocks, but for how long? For now the rising oil price has helped to boost stock markets, but if the oil rally is cut short by the increase in shale oil production In the US, then global stock markets could come under pressure. Defensive sectors such as utilities and consumer stocks may outperform in this scenario. FX oblivious to shifts in central bank sentiment, for now On the FX side, currencies like the pound haven’t been impacted by the decline in expectations of a rate cut from the BOE, and this morning GBPUSD dipped below 1.27. While we don’t think the pound will rally sharply on the back of goings on in the interest rate swap market, it could slow down the pace of the pound’s decline, and if central banks do put the brakes on their liquidity programmes then we could see FX market volatility more generally weaken in the latter part of this year. So, while an end to central bank largesse could cause a major readjustment in stock markets, its impact on the FX market could be more muted. For now though, any major weakness in the GBP/USD could be limited, although we may see down to 1.25 if we get a strong NFP number on Friday. Figure 1: expectations of a rate cut below 0.25% from the BOE for November are now back at June levels.

Source: Bloomberg and Gain Capital

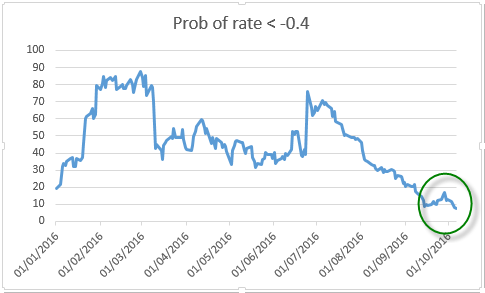

Figure 2: ECB rate cut expectations have also fallen sharply in recent days

Source: Bloomberg and Gain Capital