Is the UK labour market suffering from Brexit fever

The pound may have cleared the 1.25 hurdle on the back of the UK labour market report for February and March, but aside from the […]

The pound may have cleared the 1.25 hurdle on the back of the UK labour market report for February and March, but aside from the […]

The pound may have cleared the 1.25 hurdle on the back of the UK labour market report for February and March, but aside from the stronger wage growth the labour market data had some worrying pockets of weakness, which may suggest that the triggering of Article 50 is starting to have some economic effect.

Jobless claims: largest increase since 2011

The chief concerns are the rise in jobless claims, which surged by 25.5k in March – the month that the UK government triggered Article 50. This was the largest monthly increase in claims since 2011. Although one month’s data does not make a trend, it does suggest that we could have reached peak employment in the UK, and as we progress through 2-years of Brexit negotiations, we may see labour market weakness ahead.

Although the unemployment rate remained steady at 4.7%, the lowest level since 1975, If we see further increases in jobless claims then we could see the unemployment start to creep higher over the summer. Although employment levels are at record high in the UK, we are also seeing jobs growth start to slow. 39,000 jobs were created in the UK in the three months to February, although job creation can be quite erratic, we would expect job growth to continue to slow this year as Brexit uncertainty weighs heavily on business sentiment and investment.

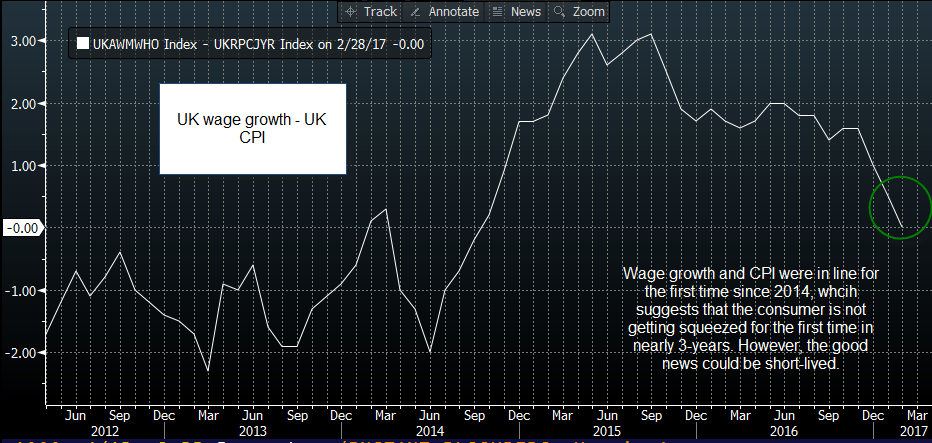

Why the UK consumer may still expect a squeeze

The chart below shows the spread between UK wage growth and UK CPI, which fell to 0% in February. This means that for the first time since 2014 there hasn’t been a squeeze on the consumer (as you can see in the chart below). But, the good news might end there. If our hypothesis is correct, and the rise in jobless claims could be a signal for weaker labour market data ahead, then we would expect wage growth to slow in the coming months, which could be pound negative. Although GBP/USD jumped on the back of today’s labour market data, the gains may not be sustainable.

The impact on sterling

Overall, we think that this month’s labour market data isn’t enough to significantly boost the pound. The Feb/ March UK jobs report is showing some signs that Brexit is starting to hit the labour market. If this continues then we believe it will be pound negative, but we need a few more months’ of rising jobless claims to prove that our hypothesis is correct. In the interim the pound is being driven by broader market forces, namely rising levels of risk aversion. GBP/JPY spiked on the labour market data but is now backing off highs, and this pair remains 1% lower on the week, suggesting that the pound could be vulnerable if markets go into full-blown panic mode over Russia/ US and North Korea fears.

Chart 1:

Source: City Index and Bloomberg