Is a stock market sell off inevitable

US stock markets reached another record high on Valentine’s Day, but where will they go next? As analysts and economists fret about potential sell-signals, the […]

US stock markets reached another record high on Valentine’s Day, but where will they go next? As analysts and economists fret about potential sell-signals, the […]

US stock markets reached another record high on Valentine’s Day, but where will they go next? As analysts and economists fret about potential sell-signals, the markets are grinding higher, and risk appetite is strong across the board.

The S&P 500 has rallied more than 250% since the financial crisis, and another 12% since President Trump won the US election in November. The Dow Jones is well above 20,000, and the Vix is close to record lows. Even emerging market currencies are starting to join the party, the South African rand is up more than 5.5% versus the US dollar since the start of this year.

So, are financial markets ripe for a sell-off? This report will analyse some of the most common sell-signals out there, and urge you to use them with caution. It will also conclude that perhaps the most reliable sell-signal of all could be what you least expect.

But are financial markets in a bubble?

To answer this question you need to define what a bubble actually is. This week’s Buttonwood report in the Economist quotes one definition from William Goetzmann of Yale School of Management who defines a bubble as a doubling in a market’s value, followed by a 50% decline. The trouble with this definition, Goetzmann found, that over five years markets are much more likely to double again rather than fall by half. Thus, even the term bubble is troublesome.

Beware using P/E ratios as a sell signal

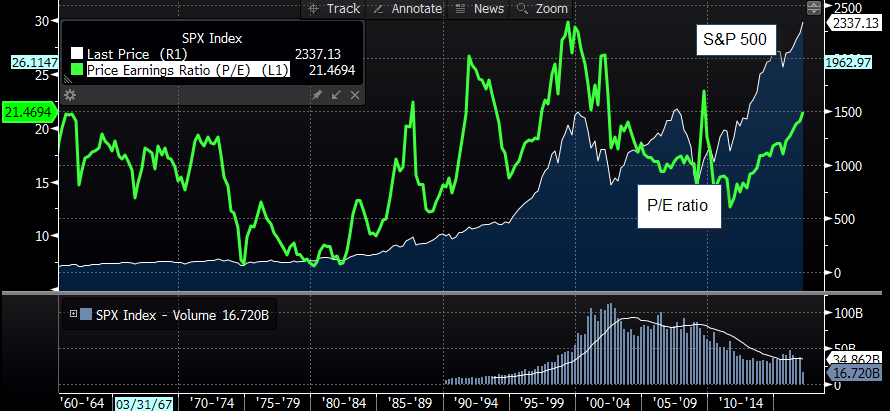

Another way to define if a market is about to sell-off is valuation, if stocks are considered too expensive they should fall in price, right? The chart below shows the price to earnings ratio for the S&P 500, going back to 1960. Over the long-term the P/E ratio has not been a reliable guide for when markets will see off, apart from the dot.com bubble when P/E ratios reached their highest ever levels. Thus, a rising P/E ratio, it is currently at 21, does not necessarily mean that a market will change direction any time soon.

Figure 1:

Source: City Index

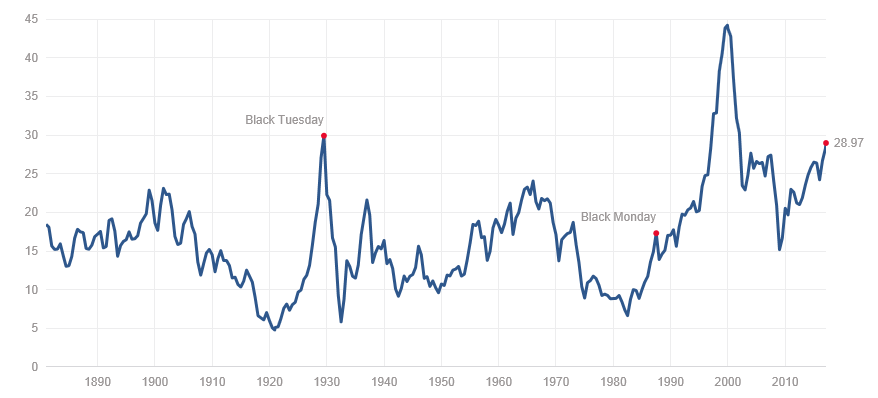

Some traders prefer to use the Cyclically Adjusted P/E ratio (CAPE), which was formulated by economist Robert Shiller. This uses average earnings, which some believe is a more accurate gauge of market valuation. The S&P 500’s current CAPE is 28 (see chart below), before the 1929 crash this peaked at 30, but its highest ever level occurred right before the dot.com bubble burst when it reached 45, so there could be more room for a further increase in the CAPE ratio before any sell off may, or may not, happen.

Figure 2:

Source: www.multpl.com

There is a wider debate going on about the relevance of P/E ratios in today’s environment, especially with an ever growing number of large multi-nationals that are big enough to buy back stock or go on an M&A spree to try and eke out growth. Some argue that P/E ratios may have reached a permanently high plateau, and thus are no use at predicting a potential market sell –off.

You can’t rely on volume data either…

Another measure of stock market health is tracking market volume. The perceived wisdom is that stock market rallies on low volume suggest that investors do not have confidence in the said rally. While larger than normal volume can be a sign that traders are confident about the market rally. However, volume has been steadily declining since the financial crisis, as you can see below. So, if you had adhered to this theory, then you would have missed the 250% increase in the S&P 500 since the 2009 low. Thus, volume indicators do not appear to be a reliable red flag for market vulnerability either.

Figure 3:

Source: Bloomberg and City Index

To conclude, it is very difficult to pick the top in a market. As this analysis shows, sharp sell offs in markets are fairly rare events, and markets tend to bounce back. The red flags that have traditionally been used to determine when a market is ripe for a sell-off tend to be wrong more often than they are right.

Could President Trump provide the most reliable sell signal?

In this environment, perhaps the biggest threat of a market sell-off comes from Donald Trump, who has made big promises on fiscal policy and financial regulation, which have fuelled the rally in equity markets since November. If he has over-promised, but under-delivers, then we could see investors lose faith and markets start to tumble.